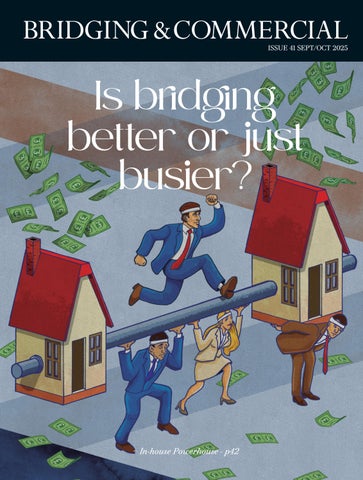

Is bridging better or just busier?

+ In-house Powerhouse - p42

+ In-house Powerhouse - p42

Editor-in-chief

Beth Fisher

Magazine manager

Dhuha Al-Zaidi

Creative direction

Beth Fisher

Dhuha Al-Zaidi

Sub editor

Christy Lawrance

Contributors

Kiernan Barnden, Chelsea Stewart, Chris Omanyondo, Alastair Hoyne, Martyn Smith, Mark Posniak, Alan Kimber, Jack Coombs, Vic Jannels, Danny Robinson, Jonathan Samuels, Joseph Aston, Shazad Ahmed, Phil Derbyshire, Zuhair Mirza, Adam Stiles, Phil Gray, Adam Tyler, Michael Strange, Colin Anderson, Lorraine Hart, John Symons, Lewis Casserley, Richard Tugwell, Jo Breeden, Stuart Benge, Tanya Elmaz, John Phillipou, Duncan Abraham, Danny Waters, Andrea Glasgow, Sam Bryce, Alice Moore, Kunal Mehta, Roz Cawood, Gary Thompson, Justin Trowse

Photography

Connie Burke, Alexander Chai, Carmen Alaimo llustration by Valf

Sales and marketing

Beth Fisher beth@medianett.co.uk

Ellen Townsend ellen@medianett.co.uk

Special thanks

Christy Lawrance, CLComms

Matt Wells SQ1 Team

Printing

The Magazine Printing Company

Design and image editing Jana Rade, impact studios

Bridging & Commercial Magazine is published by Medianett Publishing Ltd

Managing director

Beth Fisher beth@medianett.co.uk 0203 818 0160

Follow us: LinkedIn @Medianett Publishing | Instagram @medianettpublishing

To read about our commitment to the environment and sustainable print publishing, please visit https://bridgingandcommercial.co.uk/page_magazine.

The car finance industry just blew a £8.2bn hole through the argument that weak standards don’t carry consequences. The FCA says more than 14 million car finance agreements may have involved discretionary commission arrangements that weren’t properly disclosed. Now, a compensation bill in the billions is looming—and the real damage may be to trust.

It’s a moment the entire lending sector should pay attention to. Because fast-and-loose standards didn’t just impact borrowers, they left a crater across the industry. Six years ago, we ran a cover story that ruffled a few feathers—asking whether the bridging industry’s low barrier to entry was undermining standards. Back then, some said the bar was too low. Others weren’t even sure there was a bar. This issue, we revisit that question with fresh eyes, a much bigger market, and arguably even more at stake [p50].

Some believe today’s borrowers are more informed, brokers more selective, and lenders more professional. But has the bar only been lifted because the competition forced everyone to put on a better show? While we don’t expect universal agreement, it’s what makes the conversation worth having.

Elsewhere in this issue, we hear from some of the sector’s most influential names on how they’re navigating change and growth while increasing standards.

Maslow Capital’s Mark Posniak shares the thinking behind their lifecycle lending approach, and how using one team is delivering speed and consistency across complex multi-jurisdictional deals and straight-up bridging alike [p30]. Over at Precise, Alan Kimber unpacks how their newly expanded bridging team is meeting shifting borrower needs and what brokers can expect in the second half of the year [p37].

Aspen’s Jack Coombs reveals the firm’s £1bn ambition and how strategic investment in people and infrastructure is getting the lender there [p42]. Together’s Tanya Elmaz speaks frankly about knowledge gaps in the market, the importance of profitable products, and what brokers can expect from leadership changes at the top [p68].

There’s an exclusive with West One’s Danny Waters and Duncan Abraham, who are bringing a bridging mindset into the commercial mortgage space [p76], and Paragon Bank’s John Phillipou walks us through a landmark £100m scheme funding rooftop solar installations across 4,000 SME roofs—with no upfront cost to the businesses [p86].

In his column, BDLA’s Vic Jannels makes a compelling case for proactive fraud detection, launching a new early warning system and urging lenders to flag suspicions sooner, rather than trying to undo the damage later [p66]. Elsewhere, SDKA’s Kunal Mehta provides a timely reminder that brokers must ensure borrowers understand what they are signing up for in order to avoid painful exit wounds [p94].

Ultimately, this issue explores how brokers—now more than ever—are the real gatekeepers of quality. Because if standards have improved, it might be thanks to sharper expectations from them and their clients.

All in all, it’s an issue that wrestles with some uncomfortable questions and doesn’t pretend there are easy answers. But perhaps that’s the point. If bridging is going to evolve, and mature, then we need to keep asking the harder stuff, even when the market’s doing well.

Until next time.

Beth Fisher

3.50% Plus Bank of England base rate from Up to 75% LTV - Residential Up to 70% LTV - Commercial

Loan sizes: £100,000 up to £5,000,000

ESG discounts available to exit fee p.a.

2.00% Arrangement fee, 2.00% Exit fee

4.50% Plus Bank of England base rate from

p.a.

Loan sizes: £100,000 up to £5,000,000 Terms up to 24 months

“We’re

What has the CPSP taught us?

Learning lessons from decades in bridging

Life-cycle lending / OSB’s big bridging push

New positions, upgraded strategy

Six years on, did we raise the bar?

Tackling fraud one tool at a time

Tanya Elmaz / Duncan Abraham and Danny Waters /

John Phillipou

Brokers and loan pathways / Why we need PBSAs /

Breaking down exits

Meet MS Lending Group’s longest serving employee

StreamBank celebrates two years of raising standards /

Missed opportunities for funders

Here’s what you missed, but diarise these instead

Justin Trowse switches sides

When the stakes are high, we’ve got you covered.

We can fund loans up to£7.5m*, so when your clients think big...

So do we!

Fast decisions, truly transparent terms - delivered with a human touch. Discuss your requirements with us, and we'll provide a quick answer:

0117 937 4333 *Need more than £7.5m? Talk to us... Start your application here.

The Certified Practitioner in Specialist Property Finance (CPSP) course was set up by the Financial Intermediary and Broker Association (FIBA), the Bridging and Development Lenders Association (BDLA) and the London Institute of Banking and Finance (LIBF) in 2023 to educate brokers and raise standards in the specialist finance industry. While not mandatory, more than 1,000 property professionals have registered for the course and hundreds have qualified to date. We ask experts how undertaking the course has enhanced their knowledge and customer service, and how valuable it has proved to be

Kieran Barnden Bridging and commercial team leader at Brilliant Solutions

I wanted to expand my knowledge in the specialist mortgage market and ensure I could provide the highest level of advice to my clients. The CPSP process was thorough but very rewarding, and it gave me the chance to step back, consolidate my experience and sharpen my technical understanding further.

Chelsea Stewart Associate broker at Property Finance Group

At 24, I knew I wanted to establish credibility early in my career and demonstrate commitment to the specialist finance industry. Coming from a lending background, I felt it was important to build a solid technical foundation before stepping into brokering. The CPSP gave me structured learning and context that tied together the product knowledge I had from lending with a broader understanding of the market. The process was rigorous but clear, and I enjoyed being able to immediately apply what I was learning to real-world scenarios.

Chris Omanyondo Mortgage adviser at Visionary Finance

Before entering the mortgage space, I had completed my CeMAP but was eager to demonstrate to both myself and prospective employers that I could tackle more complex areas of finance. The course rewarded me with knowledge and a solid understanding of areas of lending that relatively few hold and also paved the way to my current role as a specialist adviser. The course was seamless with clear, relevant explanations on each topic.

Alastair Hoyne CEO at Finanze Capital

Despite being known in the specialist property finance space for having launched my own custom products and designed new property strategies with the finance that supported them, when the CPSP was launched I realised I had to affirm my knowledge and expertise with this exam. I already had the CeMAP [certificate in mortgage advice and practice], but this was an extra qualification that would add further credibility to my personal brand strength. Likewise, for clients who hadn’t used me previously, this was an additional set of letters to add to my name to provide the confidence that they would know I was an expert in this field. The process was very straightforward for me and, given my experience in the field, I was able to quickly scan the textbook and pass the exam after a single read in May 2024.

Alastair Hoyne CEO at Finanze Capital

My own approach to the role has not changed. But I make the CPSP a requirement for all my team, no matter the function, as I believe it provides a thorough grounding in specialist property finance, which is our core focus. More knowledge is never a bad thing. The CPSP as a foundation paves the way for the enhanced training we provide internally, given our nature as a product-structuring house. After all, our standard model works on the basis that, if we don’t already have the capability to service our client, we build a custom product/strategy for their needs.

Kieran Barnden Bridging and commercial team leader at Brilliant Solutions

It has given me added confidence when navigating complex cases and has enhanced the way I communicate solutions. Clients can see the benefit of the additional expertise while colleagues value the structured approach the qualification encourages.

Chelsea Stewart Associate broker at Property Finance Group

It’s given me extra confidence in client conversations, particularly when explaining complex structures or walking them through niche products. The qualification gave me a deeper appreciation of compliance and risk considerations, which has strengthened how I collaborate with lenders and colleagues internally.

Chris Omanyondo Mortgage adviser at Visionary Finance

The foundational knowledge it provided me with when entering specialist finance was invaluable, as I was unfazed by the fog of technical jargon when discussing cases with new clients and when learning from more experienced colleagues. This boosted my productivity in both performing and learning my role.

Alastair Hoyne CEO at Finanze Capital

Definitely. As mentioned, it provides a thorough grounding to the specialist property finance sector and is far more in depth than the training provided for our sector versus the CeMAP, which only covers the BTL, bridging and development sectors lightly. Commercial property finance isn’t simply a case of going to an aggregator platform and selecting a loan—you need a deep understanding of your clients’ needs to be able to recommend the appropriate products and select the right lenders. To be able to do that, you need to know what you are doing. The CPSP starts you off competently on that transition from the more vanilla regulated mortgage arena to specialist short-term finance.

Chelsea Stewart Associate broker at Property Finance Group

Definitely. Beyond the knowledge, I think the biggest value is the credibility it gives you with both lenders and clients. It demonstrates professionalism and shows that you’ve invested in doing the job properly. For new brokers in particular, it fast-tracks your learning curve and gives you a framework that you can then build on through real scenarios. It’s not a shortcut but a solid stepping stone to developing into a trusted broker.

Kieran Barnden Bridging and commercial team leader at Brilliant Solutions

Absolutely. It is a real differentiator in the market. Brokers gain not just technical knowledge but also a framework for handling specialist cases more effectively and, ultimately, improving client outcomes and building stronger professional credibility.

RECOMMEND

Chris Omanyondo Mortgage adviser at Visionary Finance

I would certainly recommend the CPSP to other brokers to expand their capabilities and understanding of complex, multi-faceted lending. Investment solutions often flow into one another, so having a broad understanding is crucial. As an example, a client could release equity on their residence as a deposit for an auction purchase with a bridging loan, with their exit strategy being refinance onto a BTL mortgage; such a case would require knowledge of topics covered in the course alongside the CeMAP.

Cambridge & Counties Bank is proving that sustainability and specialist lending can go hand in hand, in a market where speed, pragmatism, and partnership define success. As one of the UK’s few B Corp-certified business banks, we’re proud to be using finance as a force for good – not just for our customers, but for our colleagues, communities, and the environment.

A relationship-led approach that brokers trust

Our lending ethos is built around real relationships. Brokers tell us they value our flexibility, responsiveness, and willingness to look beyond the numbers, and our customer stories speak volumes.

Take the semi-commercial mortgage we completed with Mighty Oak Business Finance. The deal involved planning conditions, a newly formed tenant company, and the risk of significant penalty fees from the client’s existing investors. Thanks to our pragmatic underwriting and storybook lending approach, we got the deal over the line, delivering a better outcome for the broker and their client.

Or the loan we provided to The Growforward Project to purchase the former Chelfham School site in North Devon. This complex community-led initiative will transform a derelict site into a wellbeing retreat, café, and heritage centre. It’s a perfect example of how our lending supports regeneration and social impact.

Broker engagement: Built around you

We know that brokers are the heartbeat of the bridging and commercial finance market. That’s why we’ve invested in expanding our regional footprint, opening new o ces in Manchester and Reading to provide faster, more localised support. Our regional directors are empowered to make decisions quickly, and our underwriting teams work closely with brokers to deliver tailored solutions.

We also o er direct access to decision-makers, ensuring that brokers can speak to someone who understands the deal, not just the data. This relationship-led model is what sets us apart and continues to drive repeat business and referrals.

As the financial landscape evolves toward greener practices, we’re proud to support brokers and borrowers on their journey to more sustainable outcomes. In 2024, we saw a steady rise in loans secured against properties with an EPC rating of E or above — a positive trend that reflects our commitment to improving the energy e ciency of our loan portfolio and reducing the environmental impact of the assets we lend against.

Our collaboration with Twinn Risk Analytics is another step forward. By leveraging advanced flood risk modelling, we’re equipping brokers and borrowers with deeper insights to make smarter, climate-conscious decisions in an increasingly unpredictable environment.

“ Thanks to the Bank’s pragmatism, understanding and ‘story book’ lending approach, we finally got it over the line. I cannot recommend Simon and Cambridge & Counties Bank enough.”

Brian Snape

Mighty Oak Business Finance

B Corp Certification:

More than a badge

In April 2023, we became a certified B Corp, joining a global movement of businesses committed to high standards of social and environmental performance. Our B Impact Score of 92.8 places us well above the sector average, and we’re already preparing for recertification under tougher standards in 2026.

This certification isn’t just about internal culture – it’s about how we lend. We’re proud to be the first UK lender to register simultaneously for the Lending Standards Board’s Business Standards and Asset Finance Standards, demonstrating our commitment to fair, transparent, and responsible lending.

At Cambridge & Counties Bank, we’re committed to reducing our environmental footprint and improving how we measure impact. In 2024, our total emissions were 107.79 tonnes of CO₂e, equating to 0.83 tonnes per £1m revenue. We o set 140 tonnes through UK-based nature projects, including work at the Lowther Estate, giving us greater visibility and connection to the impact we’re supporting.

We also maintained our Investors in the Environment accreditation for the 10th consecutive year, a testament to our long-standing commitment to sustainability.

To further strengthen our approach, we joined the Partnership for Carbon Accounting Financials (PCAF), enabling us to improve how we measure Scope 3 financed emissions — a key step in our journey toward Net Zero.

Every deal we support is backed by a robust governance framework. In 2024, we strengthened ESG oversight, increased the proportion of loans with EPC Grade E or better, and reduced exposure to flood risk. Our Enterprise Risk Management Framework ensures we assess both physical and transition risks, helping brokers and borrowers navigate environmental and regulatory challenges with confi dence.

We’ve seen a meaningful rise in colleague-led community engagement. In 2024, we recorded 276 hours of volunteering and donated £75,000 to charity, supporting initiatives like Stepladder Plus and LEBC. While we’re proud of this progress, we know our colleagues are doing more than we’re

currently capturing, and we’re working to improve how we measure and support their impact.

Internally, we continue to foster an inclusive culture, with 44% of senior management and 50% of board members being women, and our Female Founders initiative helping women-led SMEs grow through mentoring and networking.

Let’s build a better future together

At Cambridge & Counties Bank, we believe that specialist lending can be both commercially e ective and socially responsible. At the heart of it all is our continued support for SMEs — the backbone of the UK economy. Flexible, human-centred banking for SMEs can make a real di erence. Whether you’re a broker looking for a pragmatic partner or a borrower seeking sustainable finance, we’re here to help.

Martyn Smith, CEO at Black & White Bridging, was presented with Bridging & Commercial’s Lifetime Achievement Award this summer for his contribution to the industry over the past 45 years. Here, Martyn discusses trust, how not to annoy brokers, the limits of IT, and the importance of being open and clear

Words by MARTYN SMITH CEO at Black & White Bridging

Be honest and transparent

The integrity of the bridging finance market has been tested over the years and, in some cases that integrity has been found to be wanting. To be successful in bridging, it’s crucial to shake off the stigma of the 1980s and 1990s and place honesty and transparency at the core of your working practices, which I tried to do way back from the years 2000–08. This is crucial not only to individual success but also to the reputation of the industry. We’ve all worked hard to rehabilitate bridging finance as an industry, and we need to continue to work together to maintain the position we have now carved out for ourselves.

The first step is to get your own house in order. You need to assemble a strong team, a team on which you know you can rely. How can you build honesty and transparency into your brand if you can’t trust the person sitting next to you? The only way to keep brokers coming back consistently is with relationships and first-class service, so they know that, whoever they speak to in your team, they will get the same standard of care. I learned the value of having supportive partners early on in my career. It’s been crucial to our success at Black & White Bridging.

From there, aligning with regulatory expectations and best practice in the work you do should be the bare minimum. It’s important to communicate clearly and honestly about your products, your lending criteria and your relationships with funding partners. Hold nothing back. This will help build mutual understanding and respect, not only with the businesses you are dealing with at the back end for funding, but with those who are dealing with you at the front end. Build a reputation as a company that brokers and borrowers can truly rely on and trust. This isn’t just for the sake of appearances. Ambiguity and inconsistency are counterproductive. If brokers are struggling to decipher your lending criteria, you’re missing out on opportunities. Acting with smoke and mirrors isn’t just suspicious and annoying—it’s unacceptable. Brokers want to be able to share options with their clients quickly and easily and have all the details at their disposal to answer any questions without delay. They’re under pressure to deliver and their clients, teetering on the edge of a significant credit agreement, will be looking for chinks in the armour for anything that doesn’t make sense. Clarity is crucial.

To be successful in the lending market you need to consider the needs of the borrower and the broker in tandem. Deliver on the borrower’s needs while recognising the questions that will be being asked of the broker. Good brokers understand and genuinely care about their clients. They take time to build trusted relationships that will keep clients coming back. Arm brokers with the information and resources they need to keep nurturing those relationships. Then they won’t just recommend your products because they are the best fit—although of course that is crucial—they’ll relish working with you because you recognise their role in the process. Take steps to make their job simpler—don’t pass on ambiguities that could risk their relationship with their client.

Bridging finance has come so far. More people are considering a bridging loan as a viable option. They are not put off by the rates (which are clearly going to be higher than a regular mortgage loan and no one pretends otherwise), recognising instead the flexibility and opportunity a short-term loan can provide. As bridging continues to become more mainstream, it is important lenders learn to adapt. More demand

will necessitate more lenders. To cut through will require innovation, flexible terms, new solutions for unusual circumstances and thinking outside the box.

Not only does creativity deliver competitive advantage, but it builds resilience. Having more flexible options at your disposal will put you in a better position should the lending or property market change. It also puts you in a solid position to attract custom from those with more unusual circumstances. Developing a reputation as a brand that can always deliver a truly transparent solution will make you the obvious choice for brokers.

Deliver quickly

Of course, a core characteristic of a successful bridging lender is speed. Bridging deals can be done quickly; that’s a given, especially with auction or residential bridges. And speed is another differentiator that can make a lender stand out as competition increases. With pressure on the whole property transaction process to streamline and cut completion times through digitalisation and data sharing, speed of delivery is becoming a necessity for lenders regardless of product type.

You need both tech and touch

Integrating automated and digital solutions will soon be the only way a lender can compete. Digital underwriting tools, AVMs and AI-driven risk assessments will all help to streamline the process and expedite decision-making and delivery. The key—and this will be the crux of what success looks like in the future—is to not lose sight of people in the process. Striking the right balance between automated efficiency and providing a truly human experience is a challenge we will all continue to face going forwards. It’s going to be about tech and touch.

Don’t hide behind AI

At Black & White, we’re always about people first. A machine can’t build a relationship with your brokers or sympathise with a borrower’s situation. If anything, recognising as a customer that you have been communicating with AI and not a real person does the opposite of instilling trust and respect in a brand. AI might not be smoke and mirrors but it’s still something to hide behind. Adopting time-saving administrative systems is one thing but success relies on people. Open and honest communication, balancing the needs of all parties, creativity and the ability to adapt—all of which relies on a trusted team of colleagues.

Our name says it all

There is a reason Damien Druce [COO] and I rebranded Bath & West to Black & White in 2021; it wasn’t by accident. It’s our mantra, in bringing all the good from our past, insisting on true transparency and ridding ourselves of ambiguity. It’s the only way forward for bridging lenders and the key to success.

“Developing a reputation as a brand that can always deliver a truly transparent solution will make you the obvious choice for brokers”

With better Day One funding, you can get your development off to a flying start.

We know you need to get your project up and running fast, that’s why we o er better Day One funding. From initial terms to credit approval and through to delivery, you’ll always know where you stand.

Whether your project is residential, care or student accommodation we can provide stretched senior loans ranging from £3m to £40m.

Work with a team that’s as committed to your development as you are. Take the Atelier Day One challenge – call us today on 020 7846 0000.

Words by MARK POSNIAK

Managing director, short-term finance (UK and Europe) at Maslow Capital

Life-cycle lending, which covers an investment scheme end to end from acquisition through building works to exit, can tackle time-consuming pain points, provide a planned route map, and means brokers deal with just one team

“We will double down on structuring at speed, from straightforward bridges to multijurisdictional deals, and keep measuring ourselves on what matters to brokers: daysto-decision and days-todrawdown”

Over the past two decades, it’s fair to say that the bridging finance sector has evolved beyond recognition. I know because it was exactly 20 years ago that my bridging journey began.

When I started, it was a small, largely privately funded niche. After the credit crunch, a wave of alternative lenders and fintechs professionalised the market, sharpened pricing and broadened product choice.

Since then, bridging has often been the oil that keeps transactions moving when timing or complexity makes term debt impractical.

Maslow Capital was one such lender, born in the aftermath of the global financial crisis and launching in 2009 when the UK economy was in recession and high-street banks were still nervous about lending.

But those days, while dark, were an opportunity for progressive lenders who were prepared to lend when the banks were not—and who backed borrowers’ risk. Maslow was one such lender.

For all the market’s evolution, frictions persist—and Bridging & Commercial’s experienced readers will know them well. What matters now is how lenders respond.

We’ve done this by investing heavily in moving to a full-lifecycle model, offering bridging, development and bespoke structures designed to tackle the pain points that cost brokers the most time.

Brokers can now experience dealing with a single team and pre-mapped transitions across the whole lifespan of their clients’ investment. In practice, that means fewer resets, clearer accountability, compressed timelines and an exit evidenced from day one.

Maslow is an end-to-end lender that has the capabilities to transition brokers and their clients past five milestones:

• acquire

• enhance

• build

• stabilise

• exit.

A single relationship team with a consistent credit memory avoids resets between lenders and materially compresses timelines—critical in bridging and development where speed is key.

For brokers, a life-cycle model means one credit memory and a single decision chain, so one information pack can travel through the journey with pre-mapped transitions all the way from heads of terms.

This reduces applications and paperwork, tightens timelines and improves predictability, while cross-border files benefit from coordi -

nated valuations, notarial steps and transitions planned from day one.

For clients, fewer resets mean lower frictional costs, faster drawdown and smoother, more efficient outcomes. As risks fall—planning granted, works certified, lettings stabilised—pricing and structure can be adjusted without switching lender.

It also supports faster equity recycling at developer exit and keeps the endgame in view.

A sponsor secures a disused riverside office at auction. A £500,000 bridge completes quickly to take control of the asset. While planning runs, a £250,000 refurbishment facility funds strip-out, surveys and a show flat, lifting value without committing to heavy works.

With planning granted, a £12m stretch-senior development facility delivers a mid-scale residential scheme with ground-floor retail. At practical completion, an £8.5m stabilisation facility supports lease-up and marketing, with interest rolling up against a conservative valuation.

Twelve months later, a £9.5m developer-exit loan refinances the stabilisation balance, releases £7000,000 equity and buys time to secure long-term funding. Our lending solutions team then structures targeted land-remediation finance to unlock a phase-two opportunity on the adjoining plot.

The result: by sequencing third-party reports and pre-agreeing refinance covenants at the start, the journey shaved off days and basis points at each transition.

For property investors, certainty and peace of mind are paramount.

As 2025 draws to a close, our focus for 2026 is clear: faster, transparent decisions; pricing aligned to evidenced risk; and bespoke structures delivered at pace.

We’ll continue our partnership approach, seeking broker and borrower input because those closest to the market sharpen our judgement. We will double down on structuring at speed, from straightforward bridges to multi-jurisdictional deals, and keep measuring ourselves on what matters to brokers: days-to-decision and days-to-drawdown.

Since our launch in 2009, we have evolved into a finance ecosystem with fewer moving parts, faster decisions and the ability to scale with one team as transactions grow in size or complexity.

In 2026 and beyond, that ecosystem will continue to grow, and we are keen to make even more brokers and investors an integral part of it.

You’ve been leading the dedicated bridging team. With bridging up 73%, what do you see as the biggest factors driving that?

We’ve certainly seen an increase in the number of bridging enquiries and overall awareness is growing in terms of how bridging can help overcome certain challenges. This uplift in popularity is also reflected in an increasing number of brokers now tackling bridging cases themselves.

At the start of this year, we launched the dedicated bridging division, which meant we were able to hit the ground running as we had anticipated the increased demand. The bridging team offers specialist bridging expertise to brokers with clients looking at short-term finance options as part of their property investment planning as well as guiding brokers who may be new to bridging and need additional support.

We have a team of field and office-based managers who have extensive bridging knowledge, and working alongside them is a dedicated team of around 40 in-house bridging underwriters. These experts put us in the position to be able to support any bridging case, large or small, regulated or unregulated—we have the ability to cover it all.

In Q2, we also announced the formation of a specialist property solutions team dedicated to supporting brokers and their clients with larger and more intricate cases worth over £5m, including portfolio expansion, property development and complex ownership structures. This team includes experienced underwriters and real estate professionals who can also assist with bridging solutions across both buy-to-let and commercial deals.

More recently, Becky Kidby joined OSB Group (our parent company) as bridging and commercial senior proposition manager and will play a pivotal role in ensuring our bridging range evolves with broker and customer needs. Sarah Millard has taken the reins in bridging underwriting and is already presenting a fresh focus, vigour and determination across the team, with an emphasis on converting applications into completions.

It’s a really exciting time—to see our plans coming to fruition and evidencing all the hard work that goes on is incredibly special. I feel immensely proud and lucky to be leading such a talented team of people.

LF uThis year, Precise set up a dedicated bridging division alongside a team focused on large, complex cases. Alan Kimber, its head of bridging, talks about improving processes and knowledge, and how growing demand for diverse deal types is shaping broker expertise

Have you noticed any emerging borrower needs?

There has been a lot of change in the specialist market space and, as such, investors are diversifying their portfolios to maximise their investments and also to minimise their risk exposure. This has led to changes in broker expertise too as brokers want to be able to support their clients for all their property financing needs so they need to be able to advise accordingly. There are plenty of opportunities to improve product and market knowledge in our industry, which is fantastic to see. We’re certainly seeing that brokers are eager to upskill so that they can help shape the vast range of deals their customers may require, whether that’s bridging, BTL, residential or even commercial—it’s always good to have a wide breadth.

The market shift has been clear, but it’s not just changes in regulation and policy that have led to diversification, but also ongoing challenges around property stock. Professionals in the space are looking at taking on projects to help increase their portfolios as well as margins. Due to this shift, many are looking towards bridging to support works before exiting onto a long-term mortgage solution.

We also must consider the perception of bridging as an option too. Historically, it has been viewed as an expensive way of funding. However, in recent years, the cost of borrowing via bridging has become more affordable and more in reach than ever before. This is making it a more viable option and one that an increasing number of borrowers are looking to explore and use.

Earlier this year, you said the bridging team was going to expand. How does this support the strategy?

Between January and May, we welcomed Davey Gurm, John Bremner and Jodie Worswick as specialist finance account managers and Amit Kumar as an office-based BDM within our dedicated bridging team.

Davey was already part of the OSB Group, moving over from his role in the commercial team, as was John, who was a bridging underwriter with us before making the move into an account manager position. Both have brought their extensive knowledge and experience to their new roles and the wider team.

Davey is focused on bridging opportunities across the London area and John’s background in underwriting has helped us to view cases in a different, more adaptable manner. Jodie joined us as a fresh face to the business and her network and knowledge across the North West of England has been invaluable. Amit has hit the ground running in supporting the whole field-based team and all the brokers too. He really has become the linchpin that holds everything together, which he does with such a professional, calm and confident manner.

Precise has won Bridging Lender of the Year several times. What do you think sets your bridging proposition apart from the competition?

It’s incredibly humbling to have been awarded this accolade a number of times now and, each time, myself and the whole team have felt the same sense of pride. It’s an important accolade and shows the support we give to our broker partners is recognised and valued.

At Precise, I feel we have an amazing mixture of expertise, experience and service as well as a wide product range that we can support on. We’re meeting a clear broker need by having a dedicated bridging team as we help customers access expertise when they need it and strengthen their knowledge. We understand the market and are constantly monitoring changes and trends as well as working closely with brokers to understand their challenges and concerns.

In addition, Precise has the advantage of covering regulated as well as unregulated bridging, meaning we’ve built a strong reputation as a one-stop shop for bridging expertise. However, we would never want to rest on our laurels as the market is always moving—sometimes at quite a pace. It’s important for us to remain agile in our approach so we can flex to meet changing needs.

What kind of feedback are you getting from brokers, and how do you act on it to keep improving?

Feedback from brokers is absolutely crucial to us and we use it to shape our service around the requirements that best supports them. We keep an open dialogue and, off the back of various conversations, we have introduced some really tangible developments such as a combined and condensed agreement in principle process, improved criteria around AVMs (which has helped to speed up caseloads), increased access to bridging experts as well as a developer exit proposition.

“There are plenty of opportunities to improve product and market knowledge in our industry, which is fantastic to see”

All these improvements have been brought in this year, so it proves that we not only welcome feedback but we act on it too, constantly building improvements to the broker and customer journey, making Precise quick and easy to do bridging business with.

Precise’s app, which helps keep brokers updated when away from their desks, has grown in popularity since we launched it just over a year ago. We’ve seen a higher percentage of brokers using the app for bridging case updates, which really shows its worth with the most time critical cases.

How do you work with brokers who may not have used bridging before?

We’re seeing more brokers focusing on expanding their businesses and widening their client offering to include bridging as it really can be a great financial solution in many circumstances. So, of course, brokers need support and what better place to ask than a well-established bridging lender who has excelled in this space for over 10 years?

Whether brokers are doing their very first deal or need more specialist advice, this is where our full UK coverage sales team comes in and where they can really add value.

How do you see OSB Group's bridging lending strategy evolving in the next year?

With changes made throughout the year so far, the team are now perfectly placed to take on all bridging needs. We will always see bridging as a solution for chain breaks but it’s becoming a lot bigger than that.

Our H1 results update showed that, collectively, we achieved a 73% increase in bridging business, and bridging originations hit £331.2m. We consider that to be an incredible achievement and show of commitment to the market. We were also able to share that, as a group, we now have over 19,000 active broker partners, demonstrating the strength of our service and products in the market.

We have advancements up our sleeves that will be coming over the second half of the year to further streamline the bridging process without compromising on expertise and service—so please watch this space.

One application. Two solutions. Zero uncertainty.

Seamlessly move your clients from bridging to term finance with Allica’s new bridge-to-term products: Stabiliser and Improver.

Ground-up development rates from 0.78%pm

Loans from £1m to £15m funded

Internal QS from roof level

Interview

by

DHUHA AL-ZAIDI

As part of its target to lend £1bn, Aspen is launching a groundup bridge-to-let product, the first of its kind. Jack Coombs, newly appointed chief operating officer at S&U (Aspen’s parent company), talks about in-house professional services and lending their own money, and why bridge-to-let is popular and scaling up

Congratulations on your promotion to group COO! How does stepping into this role align with Aspen’s broader vision of becoming a standout lender in the specialist finance space?

Many thanks, while my promotion to chief operating officer at S&U widens my remit to broader Group operations and responsibilities there, my focus is also heavily on Aspen. This promotion is a vote of confidence from Group, and particularly Anthony Coombs, our chairman and Graham Coombs, our deputy chairman, not just in myself but also in the important contribution to Group that Aspen is making, both current and future, and our ambitions within the sector. Aspen now makes up approximately a third of Group profit and we are confident both it, and the wider group, will continue to grow.

You’re forecasting 20% lending growth this financial year, with another 20% targeted for 2026. What gives you the confidence to sustain that pace in a competitive market?

Our funding approach, which is underpinned by our parent company S&U’s strong equity position, gives Aspen tremendous flexibility. This offers us a chance to be creative and to continually launch totally new products to the market.

The financial standing of S&U also ensures that Aspen enjoys a competitive cost of funds

This combination, if we can continue to rise to the opportunity, will enable us to compete as we are fortunate in not having typical funding constraints and, crucially, not having to refer any cases for secondary approval. We always say to brokers, ‘the good news is we lend our own money, the bad news is we lend our own money’, but, jokes aside, this is on balance a big plus.

What’s the wider significance of this leadership shift — in terms of driving growth, innovation, and long-term stability?

I will always be someone who enjoys the relationships in the industry and getting neck deep in deals and that is not really going to change. The additional responsibilities to my role include contributing to operational efficiency and innovation as well as funding across the group and complimenting the existing responsibilities of others. Overall, we are committed to improving and growing the business in a sustainable and responsible way. I am very excited about the future prospect for Aspen and look forward to helping drive that alongside Ed Ahrens, our Aspen CEO and the rest of the senior Aspen team.With £750m lending milestone to date, what strategies will you be implementing to achieve your £1bn lending ambition?

Reaching £750m is a proud milestone—but it’s also a springboard. To achieve £1bn, our focus is on scaling both innovatively and responsibly. We’ll continue to refine our lending processes, strengthen our broker partnerships and further expand and enhance our products. Equally, we’re investing in our people and infrastructure, ensuring we can handle volume without compromising speed or service. We’re confident we’ll reach the £1bn mark early next year.

Your bridge-to-let product has doubled in both deal volume and lending. What’s behind that?

Our bridge-to-let has been increasingly popular over the last 12 months because it offers a rare combination of flexibility and certainty.

It is suitable for foreign nationals who are served notice to complete on new-build developments so need a bridge to complete quickly using our no valuation service and who also want the three-year certainty we can offer them.

It is also ideal for heavy works projects where a developer can take an 80% LTV heavy refurbishment offer with 100% of works funding and then, once the works are done, seamlessly transfer across to the Aspen BTL and have the flexibility to either sell or retain units.

We have found this product has an average loan size of £1.25m; this is driven by the fact that the loan amount is up to £15m net, which allows significant works funding, and no stress testing is applied.

What can brokers expect from your ground-up bridge-to-let product, and is it already available?

The ground-up bridge-to-let product is a totally new offering to the market—as far as we know, no other lender provides it—which gives brokers and their developers a guaranteed, pre-underwritten buy-to-let offer that will match the end balance of their development loan. It is a competitive development loan of up to two years followed a seamless transition, without external revaluation or new legals, onto term finance.

The follow-up buy-to-let loan is tailored to the developer’s aims. If they want to sell, it is a one-year product with reduced early repayment charges that offers an all-in-cost equivalent to a 0.6% per month development exit.

If they would like to hold the units, then a two-year product is available, serviced at 6.74% per annum, to developers who can then build rent roll and attract stable tenants and, eventually, refinance onto a longer-term product. This offering is the perfect safety net for developers who, all too often, are compelled into costly extensions, development exit bridges and suboptimal term products.

This product has just been launched to the market; it has already attracted new brokers and developers to Aspen, and we have several progressing deals in the pipeline where developers have opted for this product.

With the recent BDM hires in the Midlands and North growing Aspen's headcount to 31, what do you hope to achieve in those regions?

We have always lent across England and Wales without geographical restrictions. However, previously, we did not have specifically dedicated sales personnel to offer brokers in the Midlands and North. Since appointing dedicated BDM’s here we are now seeing a real uptick in our transactions with several leading firms in these regions. Often, we find the deals we are looking at are not limited to the region the broker is from and the move has generally boosted our lending across the country.

You’ve added dual legal representation with no valuation and expanded your solicitor panel. How will this impact speed, service and broker confidence in Aspen?

Some brokers and borrowers want the certainty and control that dual representation offers. Having combined it with a heavy use of title insurances and Docusign, there is ample opportunity to speed up the legal process. This approach is giving our customers a faster, cost-effective service and we have already completed our first dual representation case in under a week.

We are offering dual representation on all purchases and refinances as well as light refurbishment cases. We will be continually looking to continually improve our legal and other processes as our ambition for growth demands.

WE BELIEVE THIS IN-HOUSE APPROACH WILL OFFER BROKERS AND THEIR DEVELOPER CLIENTS A QUICKER, CHEAPER AND MORE COMMERCIAL SOLUTION THAN BANKS, WHICH ARE RELYING UPON THIRD-PARTY QUANTITY SURVEYORS”

We understand Aspen is hiring an inhouse quantity surveyor in your monitoring team. What is the intent behind this?

We have operated an in-house monitoring team, made up of people with a proven track record in development who can both read a cash flow and plumb, a sink for years. This makes our heavy refurbishment product swift, accessible and cost-effective for developers. The same person appraises then comes back and releases funds, and it happens in 48 hours for a few hundred pounds and funds go directly into the developer’s bank account. It brings borrowers back both to us and the initial broker time and again.

We are looking to bring that same service to our ground-up development offering. We are therefore appointing a RICS-qualified quantity surveyor with a proven track record of appraising ground-up schemes and in project managing them to both appraise and assist with our borrowers’ development projects. We believe this in-house approach will offer brokers and their developer clients a quicker, cheaper and more commercial solution than banks, which rely on third-party quantity surveyors.

This approach means we have less recourse to professional indemnity insurance but, ultimately, that is a decision we are able to take as we principally lend our own funds and we believe that offering a better service together with competitive pricing will reduce our risk by attracting better developers. It may be a tautology but ‘good business is good business’.

As competition in the market increases, what is Aspen doing to get ahead and innovate to ultimately raise the bar?

We are taking several of the support systems around the lending process in-house and, having done this for valuation with our no valuation offering, monitoring and now quantity surveying, we will continue exploring how to offer brokers and borrowers relevant products via a faster and less expensive process. We will continue also to seek to expand the term length and scope of our buy-to-let offerings.

Our reputation has grown from decades of industry expertise, and as an established FTSE 250 business, you’re in safe hands.

We’ve now streamlined how we work, without compromising the specialist knowledge we’re known for. That means we can work with you to find the right deal, at the right price, with the right terms – faster than ever.

Six years after we questioned the state of industry standards, bridging is booming—but has the influx of new lenders and lookalike ‘cheapest and quickest’ products truly raised the bar for quality and professionalism? Brokers and lenders reveal whether progress is real, or just smoke and mirrors

Words

Six years ago, we reported on the flood of new entrants into the bridging market, where setting up a lending firm often took little more than deep pockets, industry connections, and a promise to stand out. Industry voices at the time—both lenders and brokers—sounded the alarm, warning that the low barrier to entry risked diluting quality and driving down standards.

Since then, the demand for bridging has grown significantly. In Q1 this year, the Bridging and Development Lenders Association (BDLA) recorded that bridging applications surged to £18.34bn, compared to £5.96bn in 2019, reflecting increasing borrower appetite and resilience to macroeconomic circumstances—Brexit, Covid, international conflict, and rising interest rates to name a few. Where bridging was once perceived as a niche product, it has gradually worked itself up to the mainstream pedestal, offering quick gains in a market hungry for speed.

As specialist finance grows in both traction and desirability, we raise the question: has the industry genuinely raised the bar to entry in six years?

In our 2019 ‘The Standards Issue’, we heard from several lenders and brokers that barriers to entry were considerably low. Finance providers argued the market was getting saturated, and competition between them was creeping up. Others encouraged this influx of players and said it helped to raise professionalism and competition, providing a greater range of products and services for borrowers to choose from.

In an effort to truly gauge how far the market has progressed, Bridging & Commercial contacted some of its former interviewees to gauge their opinions and find out whether a higher bar has indeed been set.

“I still believe it is easy for new entrants to come into the short-term lending market. But the level of competition in the sector now, driven by the number of lenders in the field, does mean that, to be successful, lenders need to be exceptional to attract clients,” says Phil Derbyshire, managing director at Goldentree Financial Services.

He explains that clients and brokers won't just gravitate to the cheapest set of loan terms offered to them but will instead demand top service from knowledgeable BDMs and relationship managers. Here, he says it is important that a lender will “add value to a longterm relationship that isn't just transactional, but one where the lender understands the client’s aspirations for their business and supports them in that journey”.

For Richard Tugwell, financial market consultant, existing lenders provide tacit guidance for new entrants. “Established lenders and the success that they have had in growing their businesses post-Covid-19 have provided a template for new lenders. Their actions for growth around faster decision–making and speed to completion has shown newer lenders the way in which they can compete,” he suggests.

“The level of competition in the sector now, driven by the number of lenders in the field, does mean that, to be successful, lenders need to be exceptional to attract clients”

Yet some lenders were quick to point out that a lack of proper checks and due diligence could trigger a race to the bottom, encouraging new entrants more interested in turning a quick profit than in upholding high standards of doing business. It was warned that this could result in charging hidden fees and pulling out of complex deals at the last minute.

One senior finance broker claimed the only requirement to entering the market was “a funding line, a LinkedIn account, and a BDM”. One lender was more blunt: “It’s not so much a case of raising the bar, [it’s] finding it—because there isn’t one.”

This sentiment is shared by Colin Anderson, executive director at LDN Finance. “I believe there is now a benchmark, albeit not a formal one. The unregulated sector is largely shaped by a few dominant players whose lending criteria are setting de facto standards for new entrants. This revolves around LTV expectations, speed of completion, valuation, flexibility, and pricing,” he notes. To Colin, the leading lenders that were around six years ago remain “a key component in defining the shape of the unregulated sector”.

However, for Michael Strange, managing director and founder of Funding 365, the barrier to entry for new lenders are still “exceptionally low”. He argues that the marketplace is already crowded with competitive products, notably across the LTV spectrum. “It is a difficult market for a new entrant to garner traction, given they are unlikely to have any funding advantage or product USP versus the existing lenders,” he adds.

So, if product offerings offer little individuality, questions arise about how lenders differentiate themselves.

“Deal volume is considerably lower than when the article was published and lenders are far more selective about what they are willing to lend on,” observes Danny Robinson, director at Grey Matters Specialist Lending. He claims that this in turn appears to have created a standard market mentality whereby almost all lenders operate in the same way—in terms of both risk and practices. This is “to the point where one could argue the specialist market has

“Many lenders have become very risk-averse and vanilla to the point where you question whether they’re truly in the business of specialist lending at all”

become far too vanilla at a time when complexity of borrower circumstance actually requires a specialist lender to be exactly that—specialist”, he contends.

Shazad Ahmed, director at Elan Property Finance, agrees: “There are now more brokers operating in the specialist space, which means clients are spread more thinly. I do agree that many lenders have become very risk averse and vanilla to the point where you question whether they’re truly in the business of specialist lending at all.”

Michael suggests that institutional funding—which 73% of lenders said had increased in 2024 in Bridging & Commercial’s exclusive ‘UK Annual Bridging Market Survey’ with EY-Parthenon—has enabled “sophisticated process and systems” that have raised the value and quality of products being offered. However, for Danny it is quite the contrary.

“Continued institutional investment from larger financial organisations into the specialist finance arena has impacted the DNA of what specialist lending is and should be—the specialist sector seems to have lost its identity somewhat,” believes Danny.

However, Jo Breeden, managing director at Crystal Specialist Finance, asserts that the widening of the bridging market has generally delivered better outcomes. “Borrowers have benefited from sharper rates and improved transparency/speed, while lenders have received much stronger applicant profiles with new customers who would never have entertained a bridging facility six years-plus ago,” he says. “Brokers and customers undoubtedly have more choice now than ever before.”

However, volume itself does not equate to progress. “Genuine product innovation remains limited, and too many new entrants are arriving without a clear value proposition or unique selling point. The result is an oversupply of similar-looking products and propositions, which risks confusing brokers and diluting the professionalism of the sector,” Jo argues.

Jo explains that, with many near-duplicate products, brokers struggle to distinguish between them, which slows their decision-making and makes advice harder to deliver clearly. In turn, if brokers appear to be “shopping” from a wall of indistinguishable options, it can undermine their advisory expertise and the value they bring to clients—the profession risks being seen as transactional instead of consultative.

This concept of shopping around is also noted by Danny, who claims that lenders “fish in the same pond”, and “only differ in rates or fees, as opposed to criteria enhancements or risk appetite”.

In an industry where brokers are having to adapt their skill set while learning and applying their extensive knowledge on several areas of specialist finance, being able to identify the trustworthy lenders is paramount.

“Brokers need support in identifying which lenders are truly reliable partners and which are simply replicating what’s already out there,” says Jo. Michael adds: “As the industry gets larger, it is clear from online reviews which lenders (and brokers) operate with integrity and which ones do not. This is the best protection that borrowers can have.”

Rising competition is sharpening borrower choice, but it’s also making life tougher for lenders entering the market and raising concerns over slipping due diligence. ‘EY’s 2025 UK Annual Bridging Market Survey’ highlighted that, over the past 12 months, 70% of lender respondents viewed competition as one of the top trends in the UK bridging finance market. It was also recorded as one of the top three challenges finance firms faced this year.

According to the BDLA, bridging loan completions stood at £3.99bn in 2019. Now, it’s at a record £13.1bn—arguably an indication of rising

new bridging lenders and growing borrower appetite. However, without a clear USP, lenders risk being left behind.

“If a lender doesn't have a USP and they're a new entrant, then they're going to really struggle in this market,” says Jonathan Samuels, CEO at Octane Capital. “There are already a lot of different lenders, and a lot of needs are being serviced already. Why would a broker trust a new lender without a USP for one of their important clients?”

As Lorraine Hart, head of credit operations at Roma Finance, notes, in a crowded lending environment, a USP isn’t just about standing out but rather being able to “help guide brokers and borrowers to find the best fit for them”.

“More lenders in the market is never necessarily a bad thing because it provides choice,” says Gavin Diamond, CEO at Inspired Lending. However, he explains that from a broker’s perspective, due diligence is crucial: “They always have to question the lender that they're putting the borrower with in terms of whether that is the right lender for the circumstances of the borrower. What happens if things go wrong?”

Michael emphasised the importance of valuable relationships between intermediaries and lenders. “There’s always space for new vendors to come in if they can forge good relationships, offer good service, and execute transactions—even if the product is no different from a product that existing vendors are offering,” he argues.

However, he cautions that entrants need to set themselves apart in an industry with many reputable firms: “If you haven't got a USP, you're going to be a niche player. In this market, there are too many lenders that have good products, relationships, and services. You’re not going to break that unless you have a very compelling product, meaning loan offering as well as service offering.”

This lack of originality, according to Derbyshire, will only become more prevalent as more lenders seek to set up in the market. “I don't understand how the bridging market sustains so many lenders. I'm very sceptical about new entrants,” adds Phil Gray, managing director at Watts Commercial. He explains that his experience of conducting business with lenders has confirmed this: “If you said to them, ‘Explain to me why you're better than a particular lender’, they can't because they're not and that's the problem. The market's flooded with lenders that just do the same thing.”

Joseph Aston, sales and commercial director at Aria Finance, notes caution: “The challenge is that, when lenders flood the market, offering the same thing, you find it's a race to the bottom.” He observes that new entrants typically focus on deploying capital quickly and argues that the best lenders are those that don’t move quick but prioritise understanding the borrower’s asset management process better. “More so than brokers, the borrowing community needs looking after,” he says.

“My fear is that corners can get cut on process and due diligence. How do we keep in touch with our borrowers? How do we help them exit efficiently, and how do we avoid being super aggressive on fines, charges, or possible repossessions? The low barrier to entry has an impact on borrowers that takes out that debt once they're in the loan, not necessarily in the initial delivery of it,” he asserts.

When questioned on what he means by lenders cutting corners, Joseph says that the rush to get money “out of the door” appears as product innovation, yet there is less due diligence. “Newer lenders may build products that have less due diligence—and that for me is dangerous,” he claims.

I spoke to several brokers to understand how they perceive competition and whether the influx of new bridging lenders is a positive development for choice or a drawback in terms of quality control. The verdict was unequivocal—brokers welcome competition but are less convinced whether lenders are truly fulfilling complex consumer needs.

“As the industry gets larger, it is clear from online reviews which lenders (and brokers) operate with integrity and which ones do not. This is the best protection that borrowers can have”

“Lenders’ risk appetite is so conservative now—and I get why—but it makes it hard,” says Danny. He explains that, nowadays, lenders view the industry-standard 65% LTV as a

“Continued institutional investment from larger financial organisations into the specialist finance arena has impacted the DNA of what specialist lending is and should be—the specialist sector seems to have lost its identity somewhat”

nuanced case and argues that down valuations can make a borrower’s case complicated. “If you get a down valuation now, it adds complexity to your case because you're like, ‘Where am I going to go now?’ You can't then go to another lender that offers a high LTV, because none of them do. It’s even simple things like changing valuations that will make a case complex now, which would have been a vanilla thing six years ago,” he comments.

For Adam Stiles, managing director at Helix Structured Finance, his view is the same: “The only way that a new lender can grab market share is by either having a revolutionary product or making riskier lending decisions,” he suggests.

Jo advises lenders to take the time to speak to brokers and understand why cases fall through gaps and don’t complete. “Importantly, they should be taking action to expand their criteria or improve their processes. We have intelligence which indicates cases that have fallen through the cracks, and I think that the more we can share those examples, the more lenders have decisions to make in terms of the kind of risk they want to they want to accept,” he says.

To stand out from the competition, Jo suggests lenders should raise LTV ratios.

For many lenders, the not-so-secret formula is simple: good products and exceptional service. “You can kind of dig into what you need to do to provide those two things, and there's a lot. But, at the end of the day, those are the only two things that really matter,” says Michael. This includes good funding sources and capital flexibility, as well as a solid team and technology. “Any entrant has to do those two things well to become in any way mainstream.”

For Phil, good service always has a place in the industry, and he pinpoints this as lenders being “honest, straightforward, and upfront” in how they deal with matters. This approach to communication is vital and, for Lorraine, it extends to product awareness: “When new products come out, it’s about making sure they're clear and understandable and that it's easy to see what you're offering. You’ve got to constantly try to innovate and come up with new products and solutions, especially if you see a gap in the market,” she explains.

For Gavin, it comes down to delivery and avoiding a one-size-fits-all approach. “A lot of lenders have what I would call a suite of products, and you have a situation where someone's trying to shoehorn a particular deal into a particular product. Then you get other lenders who say, ‘We don't have a suite of products because, at the end of the day, we are a solutions-based lender’. So, they invite a broker or a borrower to come to them with a particular funding requirement, and they understand what it is that they're looking for and then work with them to try to find the right solution,” he shares.

Gavin also highlights that this level of service differentiates lenders to brokers, who rely on a lender’s reputation and track record to deliver in certain circumstances.

“The lenders that we have the most loyal relationship with tend to be brilliant when it comes to overcoming barriers,” observes Jo. Namely, these are lenders willing to stretch their criteria to meet borrowers’ needs and overcome “escalation”.

After all, it’s all about trust. “Unless a new lender is very sharp on pricing, you probably would use another lender that you would trust, unless they started gaining rave reviews, because maybe I wouldn't want my clients to be the guinea pigs there,” says John Symons, mortgage broker at Curzon Financial.

At MSP Capital, we know that every successful development begins with a bold idea. But ambition alone isn’t enough. It needs the right backing to become reality. That’s why we’ve lowered our rates and enhanced the value we offer, giving you the financial strength and flexibility to bring your vision to life.

For Joseph, lenders that find their niche and stick to it tend to be worthwhile. He recognises the repetitive lender catchphrase of claiming to be the quickest or cheapest and recommends instead that firms look to innovate their systems and processes. For example, he suggests products that reward repeat borrowers: “I’ve seen some good innovation for BMV for new popular asset classes like bridge-to-let, or bridge-to-refurb-to-let. It's harder for new lenders to innovate properly because they generally have less control of their funding lines, which again leads to them having challenges in hitting the market,” he says.

Understanding that the market lacks certain niche elements, Lewis Casserley, principal and co-founder of Albatross Lending Group, has exclusively shared with Bridging & Commercial that the lender is looking to launch complex products with the aim of filling gaps in the market.

“When 95% of the industry is powered by the same capital, breaking that mould becomes the only real USP,” explains Lewis. He admits that the firm had lost its identity over the past two years and, despite being a stable lender, recognises that its business model became less competitive where other lenders pushed boundaries—including over-leveraging, cutting legal corners, and leaning on AVMs to name a few.

Though he cannot share much, Lewis hints that the lender is set to shake up the industry soon. “For us, the investment and pain of the past 24 months is about to pay off. We’ve repositioned Albatross to play in spaces that are genuinely underserved with funding lines that allow us to lend where others simply cannot. That, in our view, is the only way to build something resilient in a market that’s otherwise stuck in a cycle of commoditisation,” he says.

From what we’ve discovered, innovation from some existing and new entrants remains limited. Despite the rise in bridging lending, it appears that borrower needs are still being underserved to an extent, posing risks for both the client and broker, and highlighting the need for a lender that that can meet borrowers’ often unusual requirements.

According to Joseph, client needs are always evolving; “the challenge for borrowers is making sure a product is a fit for them. On the flip side, lenders should match this new wave of needs,” he says.

For example, Jo explains he has seen some deals fall through because of lenders’ criteria—specifically flexibility with LTVs. Adding to Danny’s point about down valuations, he asks: “If the valuation is slightly short, then the challenge we have is: can we get a stretch on the LTV to get to the loan that's required?”

Equally as important is the exit plan. “It’s not just about lending the money then leaving them to it—it should be about providing a high level of service and making sure that you are with them every step of the way,” says Lorraine.

Due diligence has never been more important, and it is up to brokers—whose roles are continuously adapting—to choose the right lender to protect their borrowers. “If you take the well-used phrase about treating customers fairly and having a customer at the heart of everything you do, we place the client with the lender who will provide the client with the best solution,” says Gray. This includes a “tried and tested track record of being able to deliver” in a strict timeframe.

“One thing that really drives me insane is there are certain firms that just use the same lenders over and over again and, from a broker perspective, that’s not necessarily the cheapest deal,” shares John. “We'll always go through the process cost wise, who really should be the best lender that's being recommended here, and work through everyone just to find out who's going to be best financial value overall.”

“In this market, there are too many lenders that have good products, relationships, and services. You’re not going to break that unless you have a very compelling product, meaning loan offering as well as service offering”

Stiles points to the lack of regulation coupled with low levels of experience among some lenders. Consequently,

“I don’t understand how the bridging market sustains so many lenders. I’m very sceptical about new entrants”

picking the wrong lender can have repercussions— and be mentally draining. “I've had a situation where the client got into a bit of a death spiral. The lender wanted to repossess the property, and the client wanted to refinance but, every time they asked for a redemption statement, the lender would take three to five days to provide one, by which time the redemption statement was out of date. It just kept going back and forth,” shares Stiles.

He explains that eventually he worked with the borrower to refinance with the said lender at a higher cost, but the lender failed to respond to his enquiries throughout the process. “There’s no real regulation for this thing,” he says. “There is a danger of lenders coming into the market that are untried and untested, that have no track record. It’s like you are rolling the dice on what the outcome might be or how that lender's going to behave.”

The BDLA is behind the drive to maintain stability and professionalism in the industry and, ultimately, protect borrowers from dealing with shady businesses.

Lenders such as Roma Finance believe that the growing influence of such associations have contributed to improvements in standards. “[The BDLA] requires its members to adhere to strict codes of conduct, ensuring transparency, fair treatment of borrowers, clear disclosures, and robust complaint-handling processes. This has led to a stronger culture of self-regulation and an increasing emphasis on professional standards across the sector,” says Lorraine.

Vic Jannels, CEO at the BDLA, highlighted key steps taken to raise industry standards and build a customer-focused market. A top priority, he says, is tackling fraud, most notably through a new intelligence-sharing platform launched in partnership with fraud prevention specialist Synectics Solutions (see page 66).

This system helps lenders to identify and address suspicious activity at an early stage. “We've been amazingly encouraged by the take-up so far,” expresses Vic. “What we were trying to do was to get to an issue much earlier in the process—in other words, to give our members the ability, if they felt concerned that they were being approached with a fraud, that they were able to establish if other people were being faced with the same issue.” He shares that, since the tool was launched in early August, he has been in contact with around five new lenders who were keen to avoid fraud.

For Zuhair Mirza, CEO at Avamore Capital, the BDLA has played a central role in encouraging collaboration between lenders and brokers to “openly discuss challenges, exchange ideas, and explore practical solutions”. He adds: “Just as importantly, they create a platform for progressing industry standards—whether that’s through sharing best practices or facilitating debate on how the industry should evolve. By strengthening these forums, we create more opportunities for shared learning and constructive progress across the sector.”

As part of a broader push to boost education and professionalism in the sector, the Certified Practitioner in Specialist Property Finance (CPSP) qualification was launched in 2023. The initiative—developed through a collaboration between the BDLA, the London Institute of Banking & Finance (LIBF), and the Financial Intermediary and Broker Association (FIBA)—aims to raise industry standards and enhance the market’s reputation. The e-learning programme covers key areas including bridging, BTL, and development finance. According to former FIBA executive chairman Adam Tyler, registrations have now reached around 1,600.

“Brokers need support in identifying which lenders are truly reliable partners and which are simply replicating what’s already out there”

“ The UK needs a huge dose of deregulation. At this point, it feels like every area of our lives is regulated, and I don’t see this regulation making life better for businesses or the average citizen—quite the opposite in fact”

Whether that means being pushed through educational courses or through an onboarding system, I think the onus is as much on brokers as it is on lenders to find the good from the bad in bridging lending.”

Jonathan agrees: “” He argues that if a new lender appears to be unprofessional, then brokers simply won’t recommend their clients to use them, preventing problems by acting as an unofficial barrier. “When it comes to regulation, there’s no middle ground—you either have it or you don’t. Ultimately, we are self-regulated by the nature of brokers choosing the lenders that they respect and have good experiences with,” he affirms.

“I think regulation can be difficult, and sometimes it just becomes too cumbersome and too burdensome, and you end up with the opposite outcome from what people wanted in the first place,” says Phil. “I do think regulation has a place, but you've got to be careful with it and make sure it does the thing it sets out to achieve.”

For Lorraine, you can have the best of both worlds: “To a degree and, certainly for us, it's about behaving like a regulated lender, while remaining unregulated in terms of fair treatment of borrowers, being clear about you're offering, and behaving in a compliant way,” she explains.

“Most bridging borrowers are investors, not consumers, so regulations would be tricky,” argues Shazad. He suggests that instead, lenders enhance the transparency of their operations. “Whether that’s lenders openly publishing turnaround times and fee structures, or brokers feeding back into shared directories, it’s those small accountability steps that raise standards without breaking the market,” he adds.

Consequently, it is down to brokers to gauge which lender is best placed for their client. And, for many, it’s down to track record and longevity.

“Who is loudest doesn't necessarily mean best,” asserts Joseph. “Brokers must get educated, meet a lot of these lenders, understand how they're funded and where that funding comes from, and what their what their back-end process looks like—before you fall for the ‘we move quickest, I can do this in 24 hours’ type of sales spiel,” he emphasises.

Mortgage adviser Stuart Benge, head of property finance at Millbrook Business Finance, uses the acronym PAPER to help him decide. This breaks questions down into the categories of people, asset, purpose, exit and reputation.

“Longevity plays a significant role. A proven track record gives confidence that a lender can deliver and, while new entrants are considered, it’s only once there is evidence they can perform reliably that we will recommend them,” says Stuart.