www.iceniprojects.com

iceni-projects

iceniprojects

www.iceniprojects.com

iceni-projects

iceniprojects

Iceni is delighted to present its 5th year of annual research into the industrial, logistics and data centre (ILD) sector.

This year we have looked at the critical role of ILD in the economic and national policy landscape, taking stock of the important contribution being made by the sector, where opportunities lie and how the public and private sector can act to best harness these.

Key messages and findings from this work are:

f I&L is a driver of the UK economy - jobs have grown by 330,000 over the last decade. In almost all regions, I&L employment growth has outperformed the economy average, with transport and storage growth more than double the broader economy average. Average I&L GVA per job is £64,900.

f The UK Transport & Storage sector jobs growth is forecast as over 330,000 over the next 20 years. However this could exceed 465,000, if

the outlook more closely follows past trends and draws on a favourable policy environment.

f Government and industry need to ensure that the workforce has the right skills in place to take advantage of the sector opportunity

Housing Growth as an Important Platform for Sector Growth

f Housing and population growth are key drivers of demand for industrial and logistics space, both last-mile logistics as well as local employment and business activity. The Government’s Standard Method housing need sees housing requirements across England increased by almost 150,000 per annum or 66%, from around 223,000 to nearly 371,000. Effects are by far the highest in London and the South East. New homes in the next 5 years alone are expected to require an additional 7-9 million sq ft of last mile logistics floorspace, and we look at where this is most prominent.

f The Government’s New Towns agenda could generate demand for 2.5 million sq.m (27 million sqft) of commercial floorspace, of which around 82% is expected to be industrial and warehousing space.

f I&L is a central piece of delivering the UK’s Modern Industrial Strategy. Government needs to recognise the criticality of planning for the sector in delivering growth ambitions. It is a platform for many of the sectors, including defence, manufacturing, life science and energy.

f The Planning and Infrastructure Bill will enable the government to introduce a system of strategic planning through Spatial Development Strategies which can establish the need for and locations for development of strategic industrial and logistics facilities.

f The English Devolution White Paper sets the government’s ambition for strategic authorities and Local Growth Plans. It is essential that Local Growth Plans and Spatial Development Strategies recognise the critical importance of industrial and logistics as an economic driver both in its own right and as a part of the UK’s Industrial Strategy.

f UK Government considers data centres to “underpin almost all economic activity and innovation”. The UK has around 450 data centres adding GVA of £4.7 billion per annum. It is estimated that around 100 new data centres could be built in next 5 years.

f The UK’s Compute Roadmap also focusses on facilitating new investment through AI Growth Zones (AIGZs). Three AIGZ have so far been confirmed – Blyth in Northumberland, Cobalt Park in North Tyneside, and Culham, Oxfordshire. The former Teeside Steelworks, Middleborough is expected to be another designation.

f The National Energy Systems Operator is also developing a Strategic Spatial Energy Plan (expected 2026) to plan energy networks and anticipate demand which will seek to identify optimal locations for 1 to 2 GW of data centre capacity.

For more information, please contact:

Matthew Kinghan, Director, Economics T: 07753 222 920 E: mkinghan@iceniprojects.com

Stuart Mills, Associate Director, Strategic Planning

T: 07771 394 497 E: smills@iceniprojects.com

This year we have looked the role of the critical role ILD in the economic and national policy landscape, taking stock of the important contribution being made by the sector, where opportunities lie and how the public and private sector can act to best harness these.

Despite macroeconomic headwinds, the sector remains resilient, integral to the economy as a whole and positioned to capture the benefits of dynamic economic and planning policy landscape.

This research looks at:

f The important contribution that industrial and logistics (I&L) makes to UK PLC

f The future contribution of the sector in economic terms

f How population growth and housing policy is influencing demand for new I&L locations and requirements

f The role of I&L in delivering the UK Industrial Strategy

f The positive outlook for Data Centres in UK Government policy

f How Strategic planning and devolution are a major platform for delivering strategic I&L space

f I&L jobs have grown by 330,000 over the last decade. In almost all regions, I&L employment growth has outperformed the economy average, but most notably in the East of England, East Midlands, West Midlands, South West and North East.

f Average I&L GVA per job is £64,900. GVA growth has been particularly high in some sub sectors, such as food & drink, pharmaceuticals and transport equipment.

f I&L (both manufacturing and logistics) outputs support multiple UK industries, including supply chains for retail, public services, professional services, construction and hospitality.

f Vacancy of I&L space has remained very low for much of the last 10 years, although has seen some increase from 2024 as deliveries overtake sluggish demand.

Primary I&L sectors support almost 4.5 million jobs across the UK and generate gross value add (i.e. a contribution to GDP) of over £290 billion. There are around a further 4.5 million further jobs in secondary sectors such as wholesale, utilities and construction (recognising not all are directly in I&L space), which generate over £317 billion in GVA.

3.1 Industrial and logistics performance snapshot

Source: Experian 2025

In 2025, the UK faces macroeconomic challenges with sluggish productivity growth, increased business costs from higher National Insurance contributions and US tariffs. However, the UK industrial and logistics (I&L) sector has been a stellar performer in recent years and despite some headwinds the underlying fundamentals for growth are strong. The reality is that I&L is the life blood of multiple sectors, ensuring supply chain and goods movements and housing a wide variety of businesses.

We have used Experian data to analyse the economic contribution of the sector. For the purpose of measuring economic performance, we have split this into key sectors of:

f Primary sectors mostly located in industrial and logistics facilities: manufacturing and transport and storage, and

f Secondary sectors, parts of which locate in industrial and logistics facilities: Wholesale, Utilities and Waste, and Construction

Over the past ten years, primary sector I&L employment and economic output has grown substantially. As explored further below, there has been some divergence between sectors, with employment shrinking in manufacturing but growing strongly in transport and storage. Secondary industrial and logistics sectors have also seen growth.

Industrial and logistics uses have a critical position in the supply chains of local economies across the nation.

Central Government statistics(1) show that around 35% of the economic output of the manufacturing and transport and storage sectors form supply chain inputs to other sectors, compared to 31% which is exported. These supply-chain inputs are essential for a variety of other industries including professional as well as service sectors.

The chart here proportionately shows how the outputs of manufacturing and transport and storage are used and flow into the rest of the economy. Boxes and grey lines are scaled to represent values of goods and services in 2022 £s.

Employment in transport and storage has grown very strongly over the last ten years as e-commerce has boomed and near-shoring has occurred post-COVID.

(GVA / full-timeequivalent job) 2024

Employment change over 10 years (2014-2024)

Source: Iceni Projects, ONS data

This growth of 24% has easily outpaced the broader economy, where employment grew by 10%.

By contrast, manufacturing and secondary industrial and logistics sectors have seen less employment growth, with contractions from pre-COVID peaks.

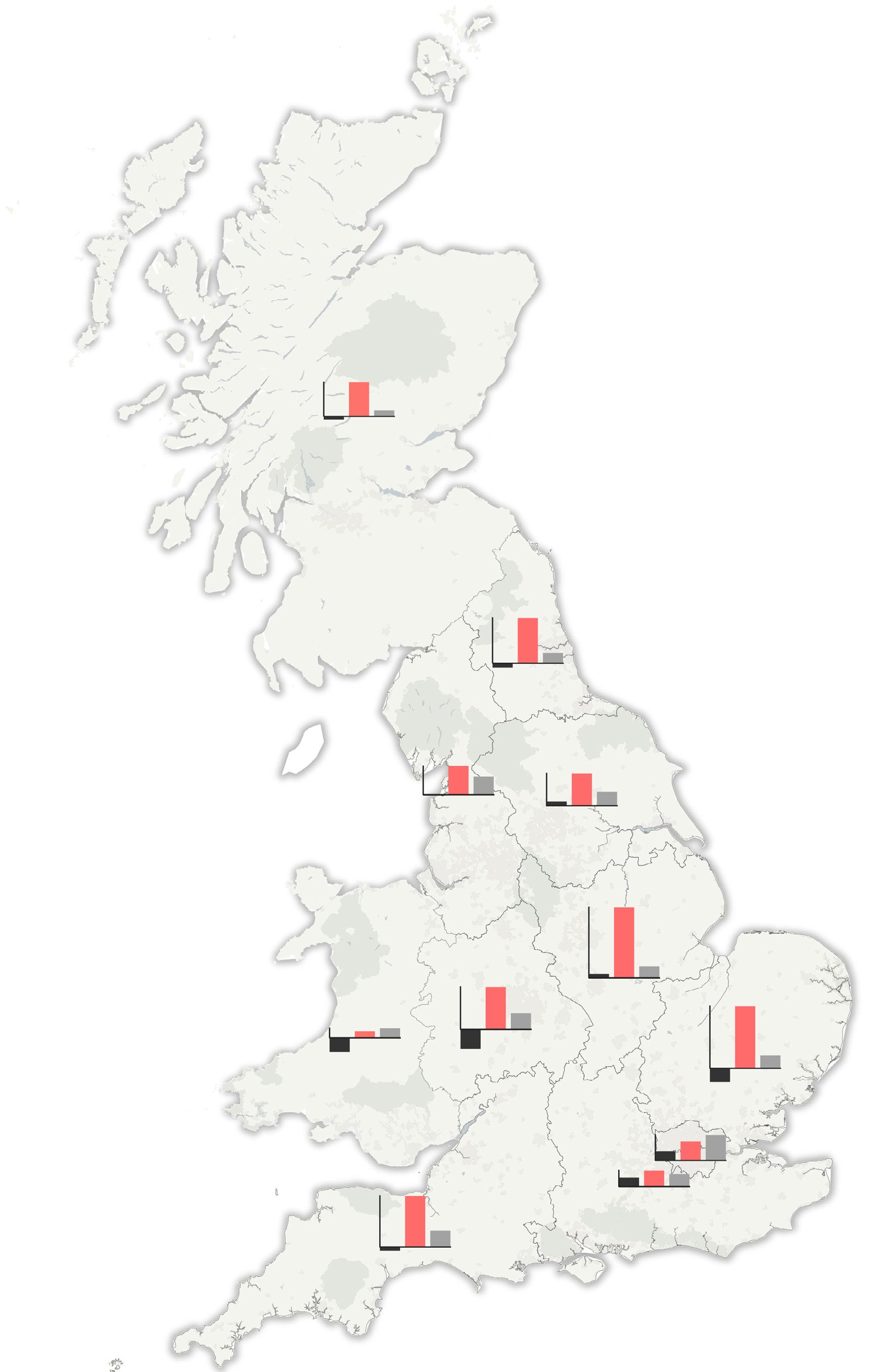

Employment growth in transport and storage has been strong across the nation, outperforming the wider economy everywhere except London, the South East and Wales. Over the last ten years the East Midlands, which contains much of the Logistics Golden Triangle, performed by far the best (+4.3% per annum), followed by the East of England (+3.8% per annum) and South West (+3.1% per annum).

There has been a more mixed picture in manufacturing, with little employment growth or

some contraction in most parts of the nation. This has been particularly pronounced in the West Midlands (-1.2% per annum) and Wales (-0.9% per annum). London and the South East have bucked the trend, seeing modest growth (+0.6% and +0.5% per annum respectively) backed by the food and beverage manufacturing sector, and by a variety of more advanced manufacturing sectors (for example electronics and defence).

While manufacturing employment has been static or even contracted slightly, this does not necessarily mean that the sector is shrinking or doesn’t need new industrial spaces.

Instead, economic output has been growing, up 4% across the nation over the last 10 years. This reflects continued automation and productivity gains,

3.2 Indexed employment growth in the UK from 2014 onwards

Source: Experian 2025

with manufacturing GVA per full-time equivalent employee up 11% in 10 years across the nation. As manufacturing continues to automate, more modern industrial premises will be needed.

In addition, some manufacturing sub-sectors have performed better than others. Growing subsectors may need more space in the future, buoying some industrial submarkets.

Manufacturing employment and GVA have grown in food, drink and tobacco (which has a large number of SMEs, has seen less automation and is very consumer-focused), and in pharmaceuticals. At the other end of the spectrum, printing and recorded media manufacturing has declined strongly in the face of competition from online media.

Figure 3.3 Productivity in the manufacturing sector in the UK

Source: Experian 2025

Figure 3.4 Figure 3.3 Regional variation in industrial and logistics employment growth over the last ten years (2014-2024) compared to the broader economy.

Source: Experian 2025

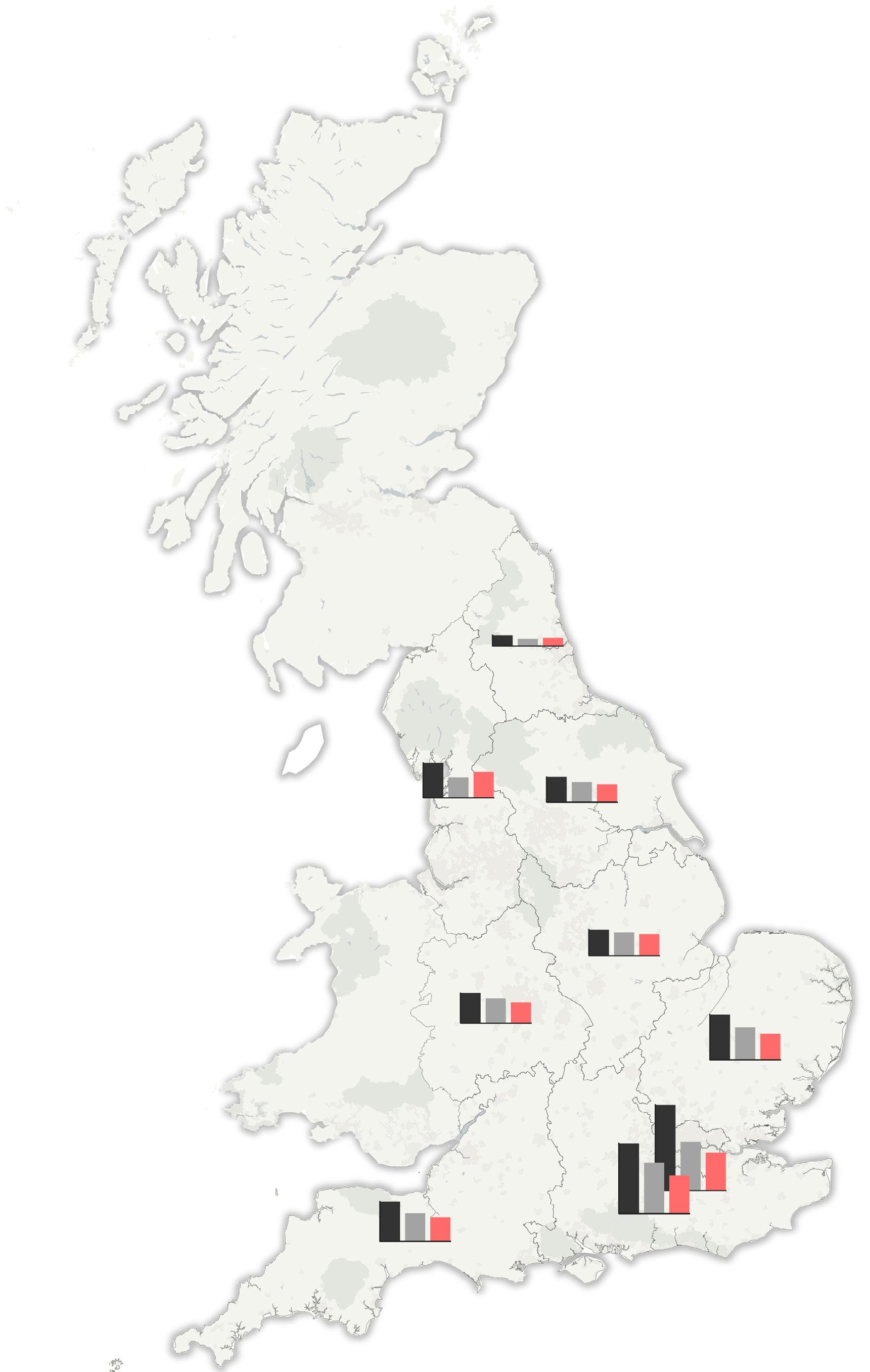

Net absorption of industrial and logistics space has consistently exceeded delivery of floorspace over the last decade. This has kept vacancy rates at a sub5% level indicating an ongoing lack of supply within the market. The market saw a slowdown in 2023 and 2024, with volatile economic and political conditions creating uncertainty within the market, pausing occupier expansion plans. Planned deliveries have slightly alleviated market vacancy, however CoStar forecasts indicates that market take-up will return in 2026 and increase year on year

Across all regions over the past decade vacancy rates have remained low, with a majority below 5%.

The North East and Yorkshire in particular have experienced low historical vacancy. Whilst levels of vacancy are now rising, the market still generally remains constrained (with London as an exception), with insufficient supply to achieve the optimal 5-10% rates that allow for market churn, business expansion and inward investment.

Taking account of planned and proposed development, CoStar forecasts that rates will still decline in 2026, through to 2030.

f I&L will continue to evolve responding to automation, power requirements, e-commerce demands, population change and infrastructure investment.

f UK Transport & storage employment growth is forecast as over 330,000 over the next 20 years, whilst losses in manufacturing may occur. However, based on past trends and a particularly favourable policy environment, jobs growth could exceed 465,000.

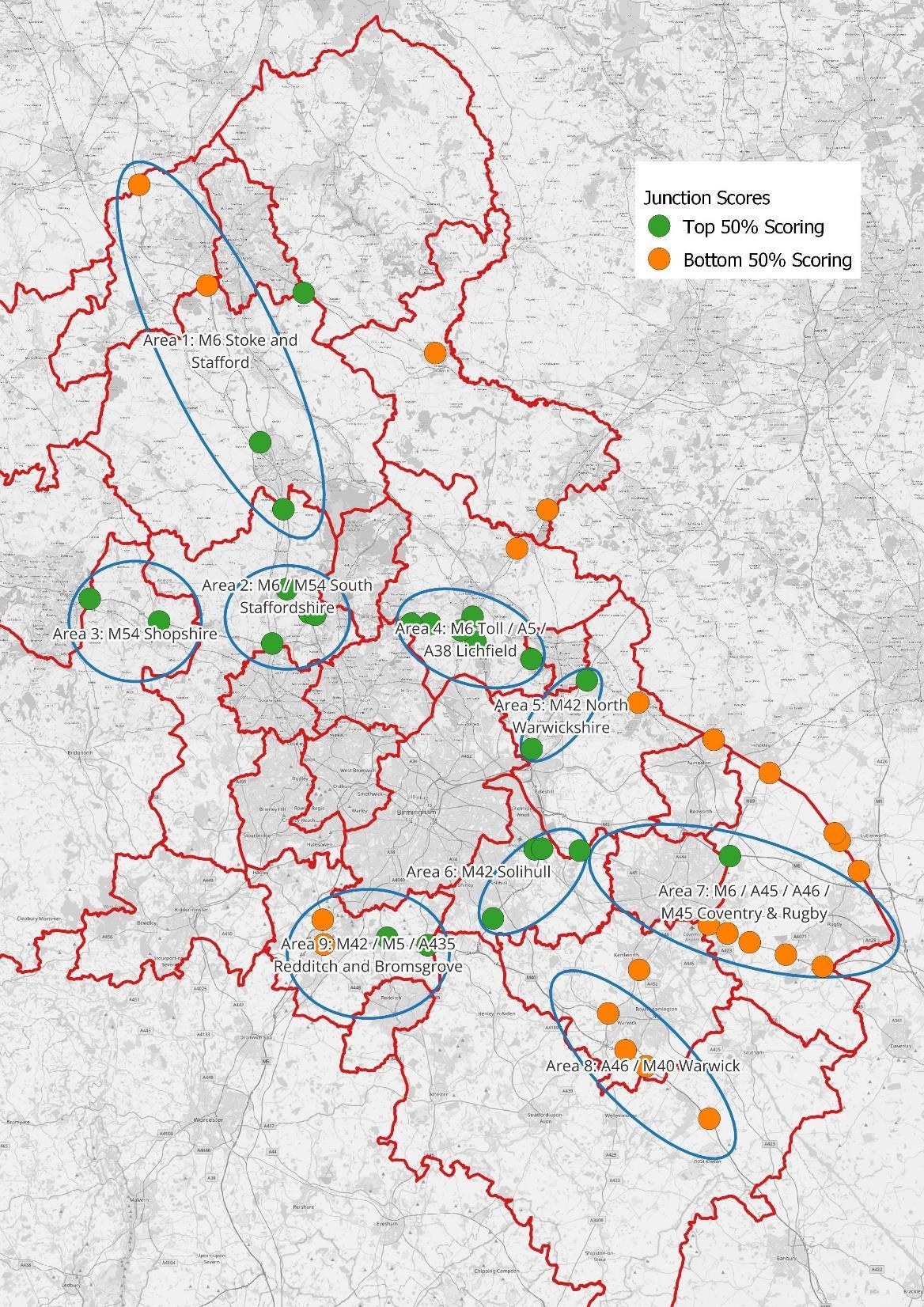

f Spatially, employment growth is forecast along a variety of key motorway junctions and corridors, particularly around the M25, M1, M6 and M3 corridors.

f Government and industry need to ensure that the workforce has the right skills in place to take advantage of the sector opportunity

Many of the trends which have been shaping industrial and logistics will continue to be relevant in the coming years, including:

f Automation, AI and digitalisation will continue to drive productivity gains, but may dampen labour demand in routine roles. This will mean a shift towards higher-skilled roles, and continued demand for modern fit-for-purpose industrial stock.

f Energy costs will be important for manufacturing competitiveness, with competition for energy with data centres and broader development. Shifts towards net zero in supply chains will influence product sourcing, pricing and substitution across several sectors.

f E-commerce and parcel networks - sustained demand for automated hubs and parcel networks will boost logistics output, even as job growth may slow somewhat.

f Freeports & infrastructure investment including major schemes like the Lower Thames Crossing

may boost connectivity, cluster growth and shape long-term logistics competitiveness

Experian forecast continued strong employment growth in the transport and storage sector, with 215,000 jobs to be added nation-wide over the next 10 years and 331,000 over the next 20. By contrast, manufacturing employment is forecast to continue to shrink as some sectors contract and others see further automation and consolidation.

However, economic growth is forecast across both manufacturing and transport and storage, with growth of over 20% in GVA forecast in manufacturing by 2044, and almost 30% in transport and storage.

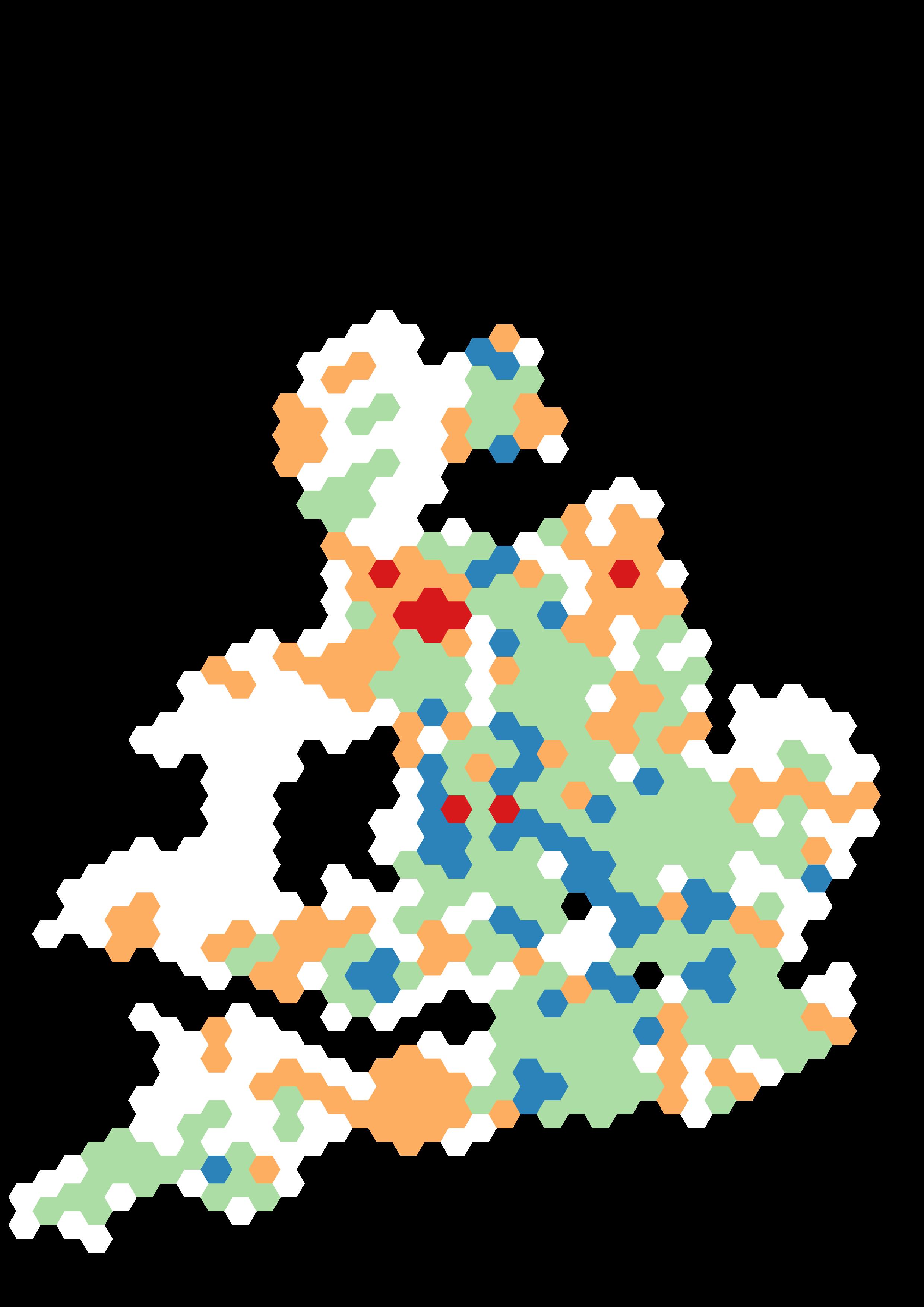

Overlaying locally specific forecasts with current employment patterns provides an indication of where industrial and logistics employment may grow and shrink in the future.

In line with the strong forecast for transport and storage employment, growth is forecast along a variety of key motorway junctions and corridors, particularly around London’s M25, the M3 and along the M1 / M6 corridor towards Birmingham.

By contrast, there are several areas in which employment is forecast to shrink, particularly around Manchester, Liverpool and Hull. These are places in which traditional manufacturing sectors have a large presence in the local industrial and logistics market.

A higher level of employment growth than forecast may be possible in the future, notwithstanding current headwinds. Considering how the sectors

Source: Experian 2025

Increase in I&L Employment

0 - 50

50 - 1,000

1,000 +

Increase in I&L Employment

500 +

50 - 500

0 - 50

have performed in the recent past, buoyed by higher rates of house-building and Government investment and programs, there could be sustained growth in the transport and storage sector (as opposed to the drop-off in growth rates forecast by Experian), while strong performance in key manufacturing sectors could limit job losses.

Under this scenario (created by Iceni to align more closely to rates of jobs growth over the last ten years), primary industrial and logistics sectors could add 468,000 instead of 122,000 jobs over the next twenty years. The bulk of this growth would still be in transport and storage, but key manufacturing sectors like advanced manufacturing, transport equipment, electronics and defence would also need to perform strongly.

This scenario would also imply higher growth in economic activity, with GVA growing by £56.1 billion (27.1%) in manufacturing and £27.5 billion (32.9%) in transport and storage over twenty years(2). This would mean an uplift in GVA across the two primary industrial sectors from growth of £69.2 billion to £83.6 billion.

Given the scale of potential economic growth for I&L, the public and private sectors need to ensure that a future workforce has the right skills to take advantage of these opportunities. This includes acknowledgement of the potential and profile raising of the sector and employment pathways.

Source: Iceni analysis of Experian Forecasts 2025 4.8

f Housing and population growth are key drivers of demand for industrial and logistics space, both lastmile logistics as well as supporting local employment and business activity.

f The current UK population projections project the highest level of growth of any recent projection series. The population is projected to grow by over 6.1 million people over the next 20 years.

f The Government’s Standard Method housing need sees housing requirements across England increased by almost 150,000 per annum or 66%, from around 223,000 to nearly 371,000. This effects every region in England but are by far the highest in London and the South East. These changes will continue to reinforce the importance planning for sustainably located industrial space.

f Emerging London Plan policies on approaches to managing industrial need may also see a greater level of substitution out of the urban capital to the fringes.

f The Government has endorsed the New Towns Taskforce, published September 2025 recommending 12 locations as potential new towns, including the importance of delivering employment within new towns. Based on Iceni research, these could generate demand for 2.5 million sq.m (27 million sqft) of commercial floorspace of which around 82% is industrial and warehousing space.

f Regarding last mile facilities, Knight Frank estimate over the next five years online retail alone is likely to require an additional 7-9 million sq ft of last mile logistics floorspace.

Implied housing need has increased in every region in England. However, both the Standard Method figures and the increase from previous requirements are by far the highest in London and the South East. The East of England and the South West also have relatively high requirements under the new Standard Method.

Figure 5.1 UK population projections from the last 15 years

(Migration Variant)

Housing and population growth are key drivers of demand for industrial and logistics space, particularly last-mile logistics servicing goods to new households and to the shops and services they use.

Housing growth also drives economic growth and supports local employment and business activity in industrial space. Significant housing expansion needs to be matched by new industrial land, so that services, supply chains, local trades, and delivery networks can keep pace with population growth.

The current official UK population projections (2022 based national projections) project the highest level of growth of any recent projection series. The population is projected to grow by over 6.1 million people over the next 20 years.

From an industrial and logistics perspective, increasing residential development is a direct driver for demand, so planning for I&L alongside residential development is essential. Gains may be at a lower level than for complete ‘new towns’ (see below), due to the ability to increase efficiencies in existing spaces, but clear influence remains and needs to be embedded into future plans. The Golden Triangle and Midlands more broadly are likely to be key beneficiaries, as is the Thames Estuary.

Emerging London Plan policies on approaches to managing industrial need may also see a greater level of substitution out of the urban capital to the fringes.

With the revised standard method driving up housing need across all regions, new towns become a key tool to deliver the additional housing requirement. The New Towns Taskforce published a report(3) on 28th September 2025 recommending 12 locations as potential new towns, which the government has responded in welcoming all 12 locations.

Figure 5.2 Increase in homes required across England under the new Standard Method

Source: Iceni analysis

The News Taskforce Report emphasises the importance of delivering employment within new towns, with one of the key recommendations for the framework for new towns being ‘business creation and employment opportunities’, recognising that new towns must be places that provide jobs for residents and enable businesses to grow.

Providing commercial premises alongside housing development is key to placemaking, improving sustainability and stimulating business growth. At a local level, housing developments need to be future proofed to be able to accommodate sustained demand for home deliveries. This could include space for cargo bikes and parcel lockers as part of a local centre.

In considering employment land requirement needed to support the proposed new towns, it is helpful to consider ratios of commercial floorspace and dwellings in other historical ‘new towns’.

Assuming on average new towns deliver 10,000 homes, these 12 proposals could support 120,000 new households. Under an average floorspace to household ratio of 21 sq.m per household this would require approximately 2.5 million sq.m of commercial floorspace to be developed over the next decade or more, of which approximately an average of 82% is industrial and warehousing space.

This space is vital to support the new communities, providing sustainable logistics function (especially last mile) for consumers and businesses, in addition to supporting population-serving industrial activities.

Source: Iceni analysis

Population and housing growth is a key driver for retail spend, online sales and last mile deliveries.

The ONS report that growth in the market share of online retail has slowed since COVID and is sitting at around 26% (exc seasonal peaks). However, the total volume of online sales has continued to increase, driving demand for regional and final mile deliveries. This is shown in the figure below, which depicts an index of retail sales at current prices.

Knight Frank estimate that for each £billion of online retail sales, a total of 1.36 million sq ft of warehouse space is required, of which around 320,000 sq ft is last-mile logistics space. Taking into account

short terms change in household growth, over the next five years online retail over is likely to require an additional 7-9 million sq ft of last mile logistics floorspace . This is in additional to business to business and other services demand.

f The UK’s Modern Industrial Strategy 2025 highlights key sectors of advanced manufacturing, clean energy, creative industries, defence, digital, financial services, life sciences and professional & business. Industrial and logistics space is a key component of many of these as set out in the following case studies.

f Defence - MOD’s Defence Fulfilment Centre – Shropshire

f Advanced Manufacturing - Tritax Park Oxford – Siemens

f Advanced Manufacturing - JLR Mercia Park, Leicestershire

f Clean Energy / Advanced Manufacturing - GigafactoriesGravity Campus, Somerset

f Life Sciences - Astra Zeneca at Speke, Liverpool Image Credit: IM Group

UK government initiatives focus on boosting the defence sector through a new Defence Industrial Strategy, launching £250 million Defence Growth Deals to foster collaboration and stimulate regional economies and investment in five regions: Plymouth, South Yorkshire, Scotland, Wales, and Northern Ireland, whilst fostering innovation in areas like AI and quantum.

Research from Savills(6) forecasts the sector will need an additional 400,000 square metres of space per year in the UK up to 2033. This equates to two-thirds of current annual take-up by the entire UK manufacturing sector.

The Defence Fulfilment Centre (DFC) is a fully modern £83 million MOD logistics centre based at Donnington in Shropshire. The facility marks a step change in the way the MOD will deliver logistics support to the UK Armed Forces. The hub is at the heart of the current drive to modernise a huge part of the MOD’s supply chain.

The 860,000 sq ft facility consists of two warehouses and a support building, and also contains an industrial-sized fridge specifically for medicines which plays a crucial role in getting medicines to personnel. During the Covid-19 pandemic, over 6,800 ventilators were distributed from the DFC.

Demand for medical devices in the UK is high and growing, driven by an aging population and the need for more advanced, digital solutions. The UK is Europe’s third-largest market and among the largest in the world, with in excess of 3,000 manufacturers producing a significant number of devices.

Tritax Park Oxford is situated directly alongside the M40 at J9 and the A41. The site provides prominence for occupiers and excellent transport links to the national motorway and trunk road network.

Siemens Healthineers have chosen the site for a new 604,000 sq ft global production facility. This will design and manufacture superconducting magnets used for MRI patient scans in healthcare facilities globally.

Tritax Park Oxford can accommodate a range of uses from Logistics and Advanced Manufacturing in buildings from 90,000 – 500,000 sq ft.

The UK automotive sector significantly contributes to the economy, with manufacturing alone adding approximately £21 billion to the UK’s economic output in 2024 and supporting around 139,000 jobs. The sector is a major exporter, with most vehicles produced for the global market, especially the EU and US. Key challenges include a significant decline in vehicle production from the mid-2010s, the high cost of energy and labour, and the crucial need to transition to electric vehicle (EV) production to stay competitive and meet zero-emission target

Mercia Park is a 3.5m sq ft manufacturing and logistics development off J11 of the M42 on the Leicestershire-Derbyshire border, home to Jaguar Land Rover’s Global Logistics Centre alongside a flagship facility for global transport and logistics company DSV.

The campus replaces a number of smaller Jaguar and Land Rover warehouses across the UK.

The park isn’t only about the physical buildings, as there has been equal focus on delivering high quality green and blue infrastructure including a 4km cycle and footpath wrapping around the site, and over 40,000 newly planted trees.

According to the Faraday Institute, the demand for gigafactories in the UK is projected to grow significantly, requiring the equivalent of 10 gigafactories by 2040 as demand for EV batteries rises to 200 GWh annually. However, significant investment is still needed to meet this demand, as currently announced plans will only cover a portion of this projected need.

Formerly the Royal Ordnance Factory Bridgwater, Gravity is now the UK’s first gigafactory commercial smart campus. In 2024 Agratas – Tata Group’s global battery business – confirmed Gravity as the location of its 40GWh UK Gigafactory, representing £4bn of investment and creating up to 4,000 jobs. This will be Britain’s biggest electric vehicle battery manufacturing facility.

Gravity is a 616 acre site of scalable, flexible and shared workspace. Ideally located in the South West with unrivalled transport links.

The University of Bristol University and Bridgwater & Taunton College sign a landmark Memorandum of Understanding (MoU) to create a framework for jointly fostering a home-grown workforce in the emerging clean growth sectors in the South West.

+ 616 acres with direct access to the M5 J23

+ Outline planning consent B1, B2, B8 and leisure + Plot sizes can accommodate up to 7,500,000 sq ft / 697,000 sq m

+ On-site rail for passenger and freight; direct access to Bristol Deep Sea Port

+ Proximity to Bristol and Exeter International Airports

+ Designated Enterprise Zone status

+ Talented labour pool; proximity to world-leading research universities

+ Significant grid connections together with renewable / low carbon on-site energy solutions provided by E.ON

+ Large scale water abstraction licence

+ Resilient

connectivity

The UK life sciences sector is a global leader, attracting significant private investment and government support through programs like the £200 million Life Sciences Investment Programme (LSIP) and the £520 million Life Sciences Innovative Manufacturing Fund (LSIMF).

At Speke, Astra Zeneca manufactures an influenza vaccine in partnership with its sister site located in Philadelphia, USA.

Around 400 employees comprised of scientists, manufacturing associates, engineers, quality professionals and support personnel form an integral part of AstraZeneca’s new Vaccine & Immune Therapy Area.

At Speke, Astra Zeneca are embarking on new and exciting ways to maximise learning and development, by advancing research, driving continuous improvement, and embracing digital by introducing collaborative robots and automation to our processes.

f UK Government considers data centres to “underpin almost all economic activity and innovation” and its desire for increased data centre capacity has been acknowledged within a range of policy.

f The UK has around 450 data centres adding GVA of £4.7 billion per annum. It is estimated that around 100 new data centres could be built in next 5 years.

f The UK’s data centre industry has traditionally been focused on London (still Europe’s largest data centre market), but recent months have seen an uptick in regional growth.

f Data centres are now considered Critical National Infrastructure. The government’s industrial strategy builds on the Artificial Intelligence Action Plan (January 2025) which include future publication of a long-term data centre capacity strategy.

f The National Planning Policy Framework highlights the need for Local Planning Authorities to meet the “needs of a modern economy, including by identifying suitable locations for uses such as…data centres”.

f The Compute Roadmap also focusses on facilitating new investment through AI Growth Zones (AIGZs). Three AIGZ have so far been confirmed – Blyth in Northumberland, Cobalt Park in North Tyneside, and Culham, Oxfordshire. The former Teeside Steelworks, Middleborough is expected to be another designation.

f The National Energy Systems Operator is also developing a Strategic Spatial Energy Plan (expected 2026) to plan energy networks and anticipate demand. The SSEP will seek to identity optimal locations for 1 to 2 GW of data centre capacity.

billion, based on an average from a range of international studies.

f The UK’s data centre industry has traditionally been focused on London (still Europe’s largest data centre market), but this is quickly expanding to regional growth.

f The UK’s data centre capacity is expected to grow by between 3.3-6.3 GW by 2030 , with approximately £45 billion of private investment committed to the sector since July 2024 .

The Government considers data centres to “underpin almost all economic activity and innovation, including the development of AI and other technology, public service delivery, and how we interact with one another”.

The Government’s desire for increased data centre capacity across the UK has been keenly acknowledged within recently-published planning and industrial policy at both a UK-wide and national level. There is significant support within Government for data centre development, and an appetite to address strategic issues that could hinder such investment.

Many of these initiatives and statistics are summarised within a recent House of Commons Library Research Briefing (August 2025) .

f The UK has around 450 data centres amounting to 1.6 GW of data centre capacity (2024). UK data centres contribute an annual GVA of £4.7

f Based on planning data, it is estimated that almost 100 new UK data centres could be built in next 5 years .

f Future uptake in Artificial Intelligence (AI) technology may necessitate smaller data centres close to population centres connected within a wider network anchored by larger AI facilities in more remote locations.

The accelerated delivery of data centres in suitable locations is considered crucial to achieving the Government’s economic ambitions. Data centre competition is global, and there are benefits to facilitating data centre operations in the UK. These include better access to high quality processing power, more efficient deployment of AI technologies, ensuring future related growth is focussed on the UK, and better and more transparent industry regulation.

Several key policy documents and announcements followed the Labour Government’s accession to power in July 2024. These include:

f Data centres as Critical National Infrastructure (September 2024)

f The UK’s Modern Industrial Strategy (June 2025)

f Artificial Intelligence (AI) Action Plan (January 2025)

f UK Compute Roadmap (July 2025)

f AI Energy Council

f AI Growth Zones

f NPPF (December 2024)

f Nationally Strategic Infrastructure Projects

f Planning and Infrastructure Bill

An announcement in September 2024 confirmed that data centres are now considered Critical National Infrastructure (CNI) . This is logical, given how reliant society and the economy have become on digital services. A dedicated CNI data infrastructure team provides strategic support for the sector, seeking to ensure sovereign, secure and sustainable systems. The importance for the nation in maintaining a regulatory edge is emphasised in ensuing policies.

The UK’s Modern Industrial Strategy (2025) places a new focus digital and technological industries, and on the development of the Artificial Intelligence (AI) capabilities of the country. This includes plans for a Connections Accelerator Service by 2026, prioritising electricity grid connections for projects that create high-quality jobs and bring the greatest economic value. The National Energy Systems Operator (NESO) is also developing a Strategic Spatial Energy Plan (SSEP) (expected 2026) to plan energy networks and anticipate demand. The SSEP will seek to identity optimal locations for 1 to 2 GW of data centre capacity.

The government’s industrial strategy builds on the Artificial Intelligence Action Plan (January 2025) which identified key opportunities to encourage growth in the sector. The Action Plan sees Government involvement including support, information-sharing, intervention, and instruction.

Concrete outcomes of the AI Action Plan include the publication of a long-term data centre capacity (or ‘compute’) strategy to ensure the UK has the infrastructure it needs and is capitalising on related opportunities; the establishment of an AI Energy Council to identify renewable and clean energy solutions for the industry; and AI Growth Zones, the provision of large-scale data centres in publicprivate partnerships.

The AI Energy Council provides expert insight on the energy needs of AI, opportunities to accelerate investment in the development of renewable and innovative energy solutions, including Small Modular

Reactors (SMRs) and the role of AI in a modern, efficient and sustainable energy system.

The UK Compute Roadmap (July 2025) aims to significantly upgrade public research capacity for AI and wider science and ensure that the UK attracts and generates industry leaders. The Roadmap outlines the foundations for AI adoption across the public sector.

The Compute Roadmap also focusses on facilitating new investment through AI Growth Zones (AIGZs). AIGZ will ‘unlock investment […] by improving access to power and providing planning support’. AIGZs have the potential to deliver employment, infrastructure and sustainability benefits. They could drive rejuvenation regionally, as data centres specialising in AI training do not need to be located near to large population centres like other types of data centres.

Regional and local authorities, as well as industry actors were invited to apply for AIGZ status and the call for applications will remain open indefinitely. 200 applications were reportedly received in April and May 2025, with three AIGZ now confirmed – Blyth in Northumberland, Cobalt Park in North Tyneside, and Culham, Oxfordshire. The former Teeside Steelworks, Middleborough is expected to be another designation.

The National Planning Policy Framework (NPPF) 2024 highlights the need for Local Planning Authorities (LPA) to plan and provide for data centres, noting that planning policies should “set

criteria, and identify strategic sites, for local and inward investment to match [the Council’s] strategy and to meet anticipated needs over the plan period.” Further, Councils should pay regard to facilitating development to meet the “needs of a modern economy, including by identifying suitable locations for uses such as…data centres”.

The updated NPPF also introduces the potential for data centre schemes to opt into Nationally Strategic Infrastructure Projects (NSIP), which would involve the procurement of a Development Consent Order (DCO) rather than standard planning permission. The NSIP route has not yet been formalised and will require statutory instrument to come forward. Further detailed advice via a National Policy Statement is expected.

f The Planning and Infrastructure Bill will enable the government to introduce a system of strategic planning through Spatial Development Strategies. These provide an opportunity for establishing the need for, and locations for, development and investment in strategic industrial and logistics facilities.

f Spatial Development Strategies may overcome the issue that plan making authorities tend to focus on local industrial and logistics needs rather than identifying strategic scale needs and locations for development.

f The English Devolution White Paper sets the government’s ambition for universal coverage of strategic authorities. These will have responsibility for preparing Local Growth Plans which are intended as the ‘guiding star’ for other plans including Strategics

Development Strategies. Local Growth Plans will shape strategic authorities funding including support for UK’s Industrial Strategy key sectors.

f It is essential that strategic authorities recognise the critical importance of industrial and logistics as an economic driver both in its own right and as a part of the UK’s Industrial Strategy. Spatial Development Strategies should be a tool to identify potential growth in this sector and provide funding support for facilitating infrastructure.

assessments rather than working collectively and collaboratively to consider larger scale development requirements. SDSs therefore create a platform for identifying the scale and locations for development.

authorities have. Local Growth Plans should highlight connections to the UK’s Industrial Strategy and 8 sectors highlighted.

The Planning and Infrastructure Bill will enable the government to introduce a system of strategic planning across England. The strategic planning tool being introduced is the Spatial Development Strategy (SDS).

Whilst SDSs are directly established to “apportion and distribute housing need to the most appropriate locations” they also provide a major opportunity for establishing the need for and locations for development and investment in industrial and logistics facilities.

The planning practice guidance states that regarding strategic [logistics] facilities, where a need … may exist, strategic policy-making authorities should collaborate with other authorities, infrastructure providers and other interests to identify the scale of need across the relevant market areas… then consider the most appropriate locations for meeting these identified needs.

However, in practice, many plan making authorities focus on local industrial and logistics needs in their

There are limited examples of where strategic assessment work has been undertaken. One particular case is the West Midlands Strategic Employment Sites Study 2024, undertaken by Iceni Projects, the first full regional assessment of need since the Regional Spatial Strategies. This sets out how an additional 800 ha of land is required across the region and a recommended distribution by sub markets.

The English Devolution White Paper published in December 2024, includes the government’s ambition for universal coverage of strategic authorities across England. These may take the form of either combined authorities or combined county authorities, and will eventually all become mayoral strategic authorities. The proposed structure aims to create a consistent two-tier system throughout England comprising strategic authorities with principal authorities (unitary authorities) sitting underneath, similar to arrangements already established in London and Greater Manchester. Strategic authorities will have responsibility for preparing Strategic Development Strategies as well as transport and local infrastructure, skills and employment and economic development and regeneration. This will include preparing Local Growth Plans which are intended as the ‘guiding star’ for all other plans including Strategic Development Strategies. Local Growth Plans will shape the spend of funding that mayoral strategic

In the context of the above, it is essential that strategic authorities recognise the critical importance of industrial and logistics as an economic driver both in its own right and as a part of the UK’s Industrial Strategy. Spatial Development Strategies should be a tool to identify potential growth in this sector and provide funding support for facilitating infrastructure, including through joint public / private initiatives.

(1) Iceni analysis of ONS UK input-output analytical tables: industry by industry (2022 table)

(2) Assuming that as job growth is higher, productivity growth is somewhat lower than forecast by Experian, meaning that the uplift in GVA is only half as much as the policy-on jobs scenario would otherwise suggest.

(3) https://www.gov.uk/government/publications/newtowns-taskforce-report-to-government

(4) https://www.knightfrank.com/research/article/202110-21-how-much-space-is-needed-to-servicethe-lastmile-and-where-is-consumer-demandgreatest#:~:text=%22Based%20our%20analysis%20 of%20e,centres%20or%20in%2Dstore%20fulfilment.

(5) https://www.knightfrank.com/research/article/202401-18-consumerdriven-demand-changing-lifestyles

(6) https://www.savills.co.uk/research_ articles/229130/380332-0

(7) Data centres: planning policy, sustainability, and resilience, Adam Cark, August 2025

(8) techUK, Foundations for the future: how data centres can supercharge UK economic growth, 4 November 2024

(9) DSIT, UK Compute Roadmap: evidence annex, 17 July 2025, p13-14

(10) HL8423, 26 June 2025

(11) BBC News, Data centres to be expanded across UK as concerns mount, 15 August 2025 (via Data Centre Construction Projects: The Surge in the UK - Barbour ABI https://barbour-abi.com/whats-driving-the-surgein-data-centre-construction-projects-in-the-uk/)

Archaeology | Built Heritage & Townscape | Design | Economics | Engagement | Impact Management

Landscape | Place | Planning | Transport

Birmingham: 20 Colmore Circus Queensway, Birmingham, B4 6AT

Edinburgh : 14 -18 Hill Street, Edinburgh, EH2 3JZ

Glasgow : 201 West George Street, Glasgow, G2 2LW

London : Da Vinci House, 44 Saffron Hill, London, EC1N 8FH

Manchester : WeWork, Dalton Place, 29 John Dalton Street, Manchester, M2 6FW www.iceniprojects.com | iceni-projects | iceniprojects