Barkat Frisian Agro’s bet on the industrialization of food

Tariq Glass able to eke out growth despite softening market

Atlas Battery sticks with lead-acid, even as lithium-ion gains traction

BF Biosciences brings GLP-1 manufacturing to Pakistan

National Foods to divest Canadian wholesale and distribution subsidiary

Profits double at SPEL on

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi)

Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The company’s ability to reap profits has been predicated on the notion that Pakistanis will eat more processed food, as incomes rise and more women enter the workforce

By Zain Naeem

One of the best ways to make money is to create - or at the very least, pioneer - an entire category of products and services. The newly publicly listed Barkat Frisian Agro, a joint venture between a Dutch food company and a Pakistani industrial conglomerate, does just that.

The company buys up eggs from Pakistani poultry farmers and processes them so that they can be utilized in the manufacture of processed food, both by companies inside Pakistan as well as the Gulf Arab countries. It sounds like a simple enough business, and perhaps a bit niche, but here is what it represents: a bet that more women will enter the workforce, incomes will rise, and domestic labour in food preparation will have to be replaced with spending some of that extra income on buying more processed food rather than preparing from scratch.

And while this publication is not, nor will it ever be, in the business of making investment recommendations, it is noteworthy that BF Agro represents the kind of innovation and growth that many of the biggest names among publicly listed companies lack.

In this story, we explain the rise of BF Agro, what makes the company able to generate the kind of growth it has seen, its successful public listing, and why it represents something new and different in the Pakistani industrial landscape.

Background of company

Barkat Frisian Agro was created in January of 2017 as it became the first and only company in the country involved in producing pasteurized egg products. Pasteurized egg products are eggs that have been gently heat-treated to kill harmful bacteria like Salmonella without actually cooking the egg. They are available as liquid whole eggs, whites, or yolks, as frozen or dried powders, and sometimes as in-shell pasteurized eggs. In addition to these, other derivatives are also extracted which are used by food manufacturers of different sizes.

The company does not sell eggs that a consumer might buy in the supermarket or in their corner grocery store. It sells eggs to manufacturers that use eggs as an ingredient in processed foods.

These egg based products become the raw materials used in baking, cooking, protein supplements to name a few. These are also used in preparation of sauces and mayonnaise. With the added step of pasteurizing these products, these can be held for an extended shelf life and add nutritional value as the product is of high quality and hygienic in nature.

The company was established under a joint venture between the Karachi-based Buksh Group and the Frisian Egg group from the Netherlands.

The Buksh Group is based in Karachi and has a decades-long history. Its oldest company is Barkat Steel (Pvt) Ltd, which started as a steel drum manufacturing company in the 1950s in what was then-East Pakistan. The company moved to Karachi after the 1972 independence of Bangladesh.

In addition to the steel business, the group owns Buksh Industries, a readymade knitted garments manufacturer in Karachi that was established in 1989. It also owns Adorn

International (Pvt) Ltd, a poultry feed and poultry farming company, set up in 1991. The company’s experience in poultry farming is what was the origin of the Buksh Group’s interest in setting up the egg production company.

Frisian Egg International was set up in 1981 by Jappie Stuiver and has grown to process million of eggs daily after leading the egg processing industry. The company has over 40 years of experience in the Dutch market in terms of egg farming, processing and sale. It already had similar operations in the Netherlands, China and Egypt.

After the venture came into existence in 2017, the operations of the company started in 2019. The initial production facility of the company was set up at Bin Qasim Industrial Park in Karachi and had a capacity of 17,000 tons per year.

The biggest advantage enjoyed by Barkat Frisian was the fact that it was the only one supplying these products which meant that it could monopolize the market. There was no one who was providing the same quality of product at a similar scale which meant that the company had the first mover advantage.

As operations started to become successful, there were plans to set up a new plant at M-3 Industrial City situated in Faisalabad. This would help the company to not only meet local demand but also cater to international markets by exporting to UAE, Qatar, Kuwait, KSA, Bahrain, Egypt and Oman. In 2024, the export sales made up 10.4% of total sales. This would also be followed by a subsidiary being established in UAE as well which would cater primarily to the Middle Eastern market.

The Initial Public Offer is carried out

In order to fund the new plans, Barkat Frisian headed towards the stock market in order to procure the funds. The issue contemplated was going to be made up

of 67.7 million shares which would make up around 22% of the shareholding. The floor price determined for the issue was at Rs13 per share which would lead to proceeds of Rs88 crores.

Most of the funds raised were going to be used to fund the new production facility which was going to be built in Faisalabad. This would increase the total production capacity from 17,000 tons to 29,000 tons per annum. Barkat had taken out a loan of Rs7.3 crores from its sponsors initially and some of the proceeds from the Initial Public Offer would be used to pay off this loan. The remaining Rs81 crores would be used to set up the new production facility.

Before the offering was carried out, there was an expectation that the issue would do well as it was being carried out by a company which was the sole provider to the segment. The results of the issue surpassed even the most optimistic outlooks. The issue was oversubscribed by 16.25 times which means that there was a demand of more than 1 billion shares by the market.

Due to the high demand, the floor price of Rs13 became an after thought as the issue increased to Rs18.2 per share or 40% higher than the floor price. This is the limit that is placed by the market which meant that investors were willing to buy the shares at the maximum price that was allowed to be reached.

The price performance of the stock after the issue further strengthens the belief that Barkat Farisian is just getting started. Having been listed at a price of Rs18.2 in March 2025, the share price has steadily increased to Rs44 by the end of September 2025.

The secret behind the success

The key to success for the company is two fold. At one end, the company is the only one that is capable of supplying good quality raw

materials to many of the industries that it caters to. On the other is the fact that there is a wide range of customers that Barkat Frisian is able to sell to. The company caters to hotels, restaurants and catering businesses. In addition to that, the Fast Moving Consumer Goods (FMCG), both local and international, baking and cooking industries also need the goods that are produced by Barkat Frisian.

The client base of the company already bodes some big names in terms of their name recognition. At the local level, National Foods is the biggest customer for the company and there is a long term contract between the two parties. In terms of international clients, Mondelez International based in Singapore, Kerry Oman in Oman, AATCO Food Industries in Saudi Arabia and Sri Lankan Catering are some of the top clients.

Barkat Frisian has also been able to get a leg up in relation to other industries as well as it was established in a Special Economic Zone which meant that its income as exempt from any income tax for a grace period of 10 years from 2019 onwards. In addition to that, as the operations are primarily entred around the poultry sector, the company only has to pay a minimum turnover tax of 0.75% which gives it another advantage over other sectors.

The success that is being seen at the company has its seeds dating back to when the joint venture was being contemplated. The foundations that were laid at that point in time are now bearing fruit for the company. In 2017, the company set out to establish a state of the art production facility which was based on European standards of quality. Even though this took time and effort to gain the necessary certifications, that is the reason that the company saw the growth and expansion in the business over the years.

Barkat Frisian had the time to get these certifications and could take as long

as possible in this process as it was looking to establish a monopoly. No other company in the country was providing these goods so they had the benefit of being the first mover. Once they were able to establish themselves, many of the clients came running to the company to procure good quality raw materials for their own usage.

The certifications that were attained by the company included ISO 9001:2015, FSSC 22000, HALA and SMETA certifications. Each of these steps allowed the company to not only establish its own brand but to create serious barriers to entry for new entrants to enter the market. The establishment of a high quality production facility, certifications and expertise all came together to make sure that competitors could not easily enter such a market.

After 5 years of operating, the constant will to improve and get better did not rest. In 2004, an IPO was contemplated as the growing demand made a new production facility viable and justified. In order to fund this expansion, the capital markets were used which showed that Barkat Frisian was willing to trust the market and share the value creation around.

In response, the market did not disappoint. The book building was over subscribed and the constant increase in the listing price shows that the market also believes in the ethics of the company.

There is also an aim to expand the market that the company is catering to by looking to export its products across the border to keep expanding long into the future. As the new facility is expected to come online, the local demand will be transferred to this facility while the Karachi plant will look to meet export related demands into UAE, KSA, Bahrain, Oman, Qatar, Kuwait and Egypt. In relation to that, Bakery Line Catering, a distribution company in Kuwait has already been tasked with export distribution.

Revenue drivers

The first move advantage enjoyed by the company means that it is able to dominate the local market by being the only game in the industry. This allows it to leverage its monopoly, set and improve the industry standards and satisfy the needs of its customers all by itself. As it looks to keep pushing the envelope in relation to quality standards, they can make sure that they keep monopolizing the market perpetually.

There is a two way relationship between the company and its customers as they can develop high quality products on their own accord. The customers can also demand certain products from the company which it can provide tailoring the product to the needs of the market. As customers are heard and catered to, there is a higher likelihood that they will keep coming back.

Barkat Frisian has also proved to be the pioneer in the economy as it has brought higher safety standards where none existed before. In the past, there was a lack of compliance to global standards which left a huge gap in the market. Barkat Frisian was able to enter and dominate this niche by targeting food manufacturers, bakeries and the food service sector.

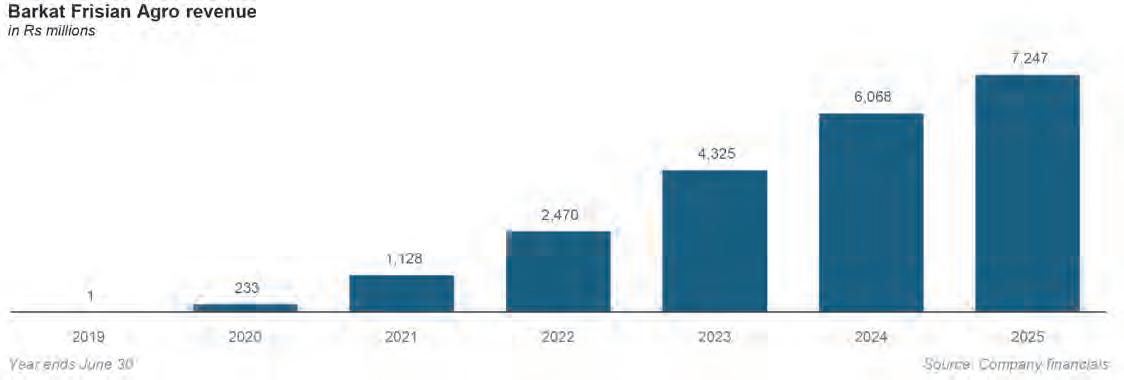

The local egg production demand has also seen an increase from 20 billion eggs being demanded in 2020 to more than 25 billion eggs in 2024. This is a compound annual growth rate (CAGR) of 5.8%. In the same period, Barkat Frisian has been able to grow its revenues from Rs23 crores in 2020 to Rs6 billion in 2024. This translates to a CAGR of 126%.

Not only has the company been able to keep competition out, it has also been able to amass high profile clients locally and internationally which has helped it to grow its top line. The company boasts a relationship with Unilever, English Biscuits Manufacturers and Ismail Industries to name a few. Due to the size of these clients, Barkat Frisian is guaranteed

that it will have a steady growth and demand which will yield profits.

Lastly, the will to not sit idle and rest on its laurels has meant that there is a constant struggle to innovate and expand the product portfolio. The innovation of egg powder, eggshell membrane and value added shell egg products has been carried out in order to diversify the product portfolio of he company itself.

After considering the revenue streams of the company, the next step is to see the costs that the company faces as well. The biggest cost for Barkat Frisian is the sourcing of fresh eggs which is the primary raw material for the company itself. Any changes or volatility caused in the price of eggs will have a direct impact on the direct costs faced. Market fluctuations, seasonality, quality and scale of purchase will have an impact on the total costs that are faced by the company. According to an estimate, 96% of the total cost of sales are made up of raw material related costs. In terms of supply chain management, Barkat Frisian has contracts with local egg suppliers which is helpful in decreasing volatility and uncertainty related to procurement of eggs.

Financial Performance

In terms of the financial performance, it can be seen that the company is getting better each year. In order to break down the financial performance, each element of the income statement and balance sheet has been considered from 2021 to 2025. Each of these indicators shows that the performance is actually getting better over time.

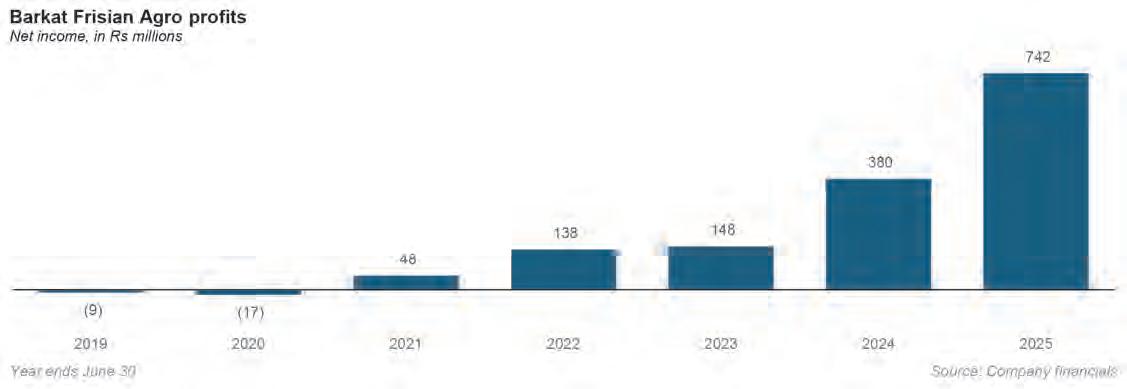

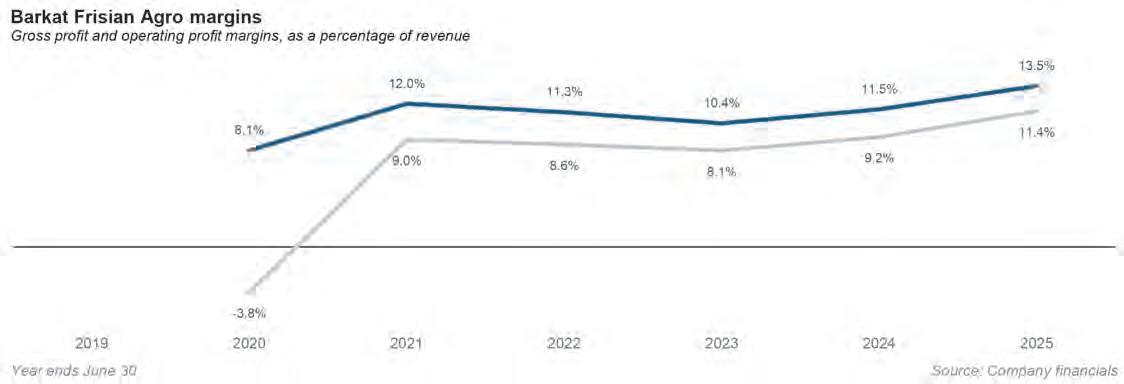

First of all, the net revenues of the company have grown from Rs1.1 billion in 2021 to Rs7.2 billion by the end of 2025. In relative terms, this is an increase of more than 6 times from 2021 which shows that the company is earning better revenues each year. The gross profits for the company has also increased from Rs14 crores in 2021 to Rs1 billion in 2025.

The growth in gross profits is complimented by the gross profit margin which is also improving with the increase in sales. Gross margin was 12% in 2021 which has increased to 13.5% in 2025. This means that not only has the company been able to increase its sales but it has also been able to decrease its direct costs which has led to gross margin improving to 13.5%.

One of the biggest indicators of improvement is that operating profits clocked in at Rs82 crores in 2025 which had actually been only Rs10 crores in 2021. Similarly, profit after tax was Rs74 crores in 2025 which were Rs5 crores in 2021. In terms of margins, operating margin went from 9% in 2021 to 11.3% in 2025 while net margin was 4.2% in 2021 which increased to 10.2% in 2025. The cost saving measures can be gauged by the fact that in 2021, other direct costs and expenses made up 8% of sales. By 2025, this ratio had fallen to only 2%.

Going down the balance sheet for the most recent years, it can be seen that the listing process has been able to strengthen the equity side of Barkat Frisian. In 2024, the shareholder’s equity was valued at Rs1 billion which increased to Rs3 billion. Most of this increase could be attributed to share premium of Rs1 billion while around 0.7 billion was attributed to the increasing unappropriated profits being earned.

The proceeds being used to pay off related party loans also meant that non-current liabilities of Rs20 crores in 2024 fell to just 8 crores a year later. With the fall in long term loans, the current liabilities also decreased from Rs79 crores to Rs66 crores which further consolidated the financial position.

As the company was able to get access to more funds than it was looking forward to, the excess funds were used in the working capital requirements of the business which allowed it to buy more inventory and allow lenient terms to its debtors which were able to grow the sales. Having more funds that required, the

company used them to pad its current assets by investing in short term investments, creating a derivative asset, allowing for greater trade debts and buying more inventory.

The derivative asset created was a forward exchange contract bought by the company to hedge any foreign currency risk that it was exposed to. By buying these contracts, Barkat Frisian would be protected from any appreciation that could take place in the market which would decrease the amount of rupees earned. Similarly, investment was carried out in Meezan Cash Fund and Pak Qatar Islamic Cash Plan which could be used to supplement the income earned on the excess funds it had.

Barkat Frisian has been able to develop its revenue streams to such an extent that in 2025 it was able to record sales of Rs7.2 billion which had been Rs6 billion in 2024. Half of this increase was seen in local sales while 0.6 billion was attributable to export sales carried out.

All these factors combined to convert profit after tax of Rs38 crores in 2025 to Rs75 crores in 2025. At this point, it might seem difficult to understand why earning per share of Rs4.22 went on to become Rs3.68 just a year later when profits had almost doubled. The reason for this was the share issue that had taken place causing the number of shares to increase.

Based on the analysis carried out, it can be concluded that Barkat Frisian has been able to carve out a niche for itself. By positioning itself as a market leader, it has been able to establish itself as the only player in the game and yielding higher revenues on an yearly basis. With the Faisalabad plant expected to come online in 2026, it can be expected that the top line, bottom line and margins will keep improving in the coming years. With an established supply chain, export opportunities and subsidiaries under works in the UAE, it can be expected that things will only get better for the egg product manufacturer in the near future. n

Tariq Glass able to eke out growth despite softening market

The company’s production facilities are not operating at full capacity but it was able to increase pricing due to its commanding market share

Profit Report

Tariq Glass Industries Ltd squeezed out growth in a tricky year for Pakistan’s glass and ceramics market, leaning on pricing power and tighter cost control even as demand cooled enough to idle a furnace. The group’s subsidiary, Baluchistan Glass Ltd, remains in rehabilitation mode with all three of its plants temporarily shut, but a phased restart plan and a pivot toward pharmaceutical glass suggest a more constructive year ahead if energy supply stabilises.

Revenue growth was steady rather than spectacular: net sales increased 13% yearon-year to Rs33,562 million (from Rs29,599 million), while gross profit climbed 33% to Rs10,415 million, pushing the gross margin up to 31% from 26%. Operating profit grew 38% to Rs9,294 million as selling and administrative costs remained contained. The fourth-quarter picture echoed the full year: sales up 8%, gross profit up 30%, and operating profit up 34%. The net margin for FY25 eased to 14% from 15% owing to a heavier tax charge, but remained healthy given the backdrop of weak end-demand. (Financial table, page 2.)

Price leadership helped. Tariq Glass says it maintains around 50% share in float glass

and 60–70% in tableware, a dominance that underpins its ability to pass on cost inflation. Float glass contributes about 70% of revenue, with tableware making up the balance. The company also signalled that topline growth in FY25 was driven by margin improvement and product price increases, a vital lever at a time when industry utilisation was suboptimal.

Costs were managed actively through energy optimisation. The company expanded its solar capacity to 3.5 MW against a 10 MW requirement and dynamically shifts its energy mix daily to the cheapest available source. Even so, inputs remain pricey: management cited a weighted average gas cost of roughly Rs3,300 per MMBtu and grid electricity at around Rs38–39 per unit. Soda ash prices – a key raw material – were about Rs90,000 per ton, while silica sand sat near Rs6,000 per ton.

Demand softness was plain enough that one of Tariq Glass’s furnaces is currently non-operational, as is one major competitor’s plant. Management explained that glass furnaces are designed to run at full tilt; when downstream demand stalls, inventories swell and even breakeven exports become an option just to keep lines warm. Meanwhile, unplanned WAPDA outages have periodically hurt production, prompting the company to prioritise in-house power generation and push forward with a waste-heat recovery project now in the pipeline.

Put together, FY25 was a case study in pricing power offsetting volume lethargy. Tariq Glass protected margins through cost discipline, energy self-help and selective price rises, a playbook that allowed it to register incremental earnings growth despite operating below optimal capacity.

The contrast with the subsidiary could hardly be starker. Baluchistan Glass Limited (BGL) reported a loss per share of Rs1.97 for FY25 versus a loss of Rs1.94 in FY24. The fourth-quarter loss per share improved to Rs0.20 from Rs0.79 in the same period last year, but the company remains in the red as it works through a comprehensive plant rehabilitation.

All three BGL plants – Units 1, 2 and 3 – are currently shut for balancing, modernisation and replacement (BMR). Unit 1, located at Hub, is the first in line for revival, targeted for the third quarter of FY26 (roughly March to June 2026) subject to adequate gas pressure and regulatory approvals. Before the closure, Unit 1 operated at around 85% utilisation, producing 80–85 tons per day against a 110-ton nameplate capacity.

The immediate culprit for the shutdowns has been inadequate gas pressure and supply disruptions, which sometimes forced expensive HFO and LPG substitutes. To mitigate this, BGL has constructed an independent gas pipeline that is 90% complete, aimed at

eliminating the pressure issues associated with the previous shared pipeline. The company also faces differentiated gas pricing across sites: Units 2 and 3 (Lahore and Kot Abdul Malik), connected to SNGPL, buy RLNG at about Rs3,000 per MMBtu (variable monthly), while Unit 1 (Hub), connected to SSGCL, benefits from a mixed rate – roughly 90% Sui Gas and 10% RLNG – translating to an effective Rs2,300–2,350 per MMBtu.

BGL’s FY25 financial table underscores both the severity of the operating stress and the early signs of stabilisation: net sales of Rs718 million (up from Rs161 million as Tariq Glass channelled all output through its own network), a gross margin of –65%, an EBITDA loss of Rs286 million, and a full-year net margin of –99%. Fourth-quarter net sales slumped to Rs16 million as the shutdown deepened, but the quarterly loss per share narrowed as cost actions took hold and other income provided a cushion.

A key interim arrangement has helped preserve liquidity: Tariq Glass procured BGL’s entire production and moved it forward through its own channels, a step designed to avoid BGL’s cash getting stuck in building a distribution network while the subsidiary was non-operational. Once BGL is back on line, it intends to develop its own distribution over time.

The broader rehabilitation roadmap is straightforward: restart Unit 1, then commence renovation and potential redesign of the furnaces at Units 2 and 3. In parallel, BGL continues upgrading moulds, machinery, motors and hydraulic systems for energy efficiency, though capex quantum and design for Units 2 and 3 are still in early planning. Management’s stated first priority is to bring BGL to full potential on its own strength, a move they say will reintroduce “healthy competition” to the market.

Tariq Glass is one of Pakistan’s bestknown names in glass, with a multi-decade heritage in float glass for construction and tableware for household and institutional customers. Over time, the company has grown into a scale domestic producer with a differentiated portfolio and a national distribution footprint. That journey included the acquisition and stewardship of Baluchistan Glass, a move that provided a second production platform and access to strategic locations –Hub near the port, and Lahore/Kot Abdul Malik near major demand centres – albeit with today’s energy-related complications.

The Tariq Glass story has generally been one of capacity-led growth and product mix upgrades, punctuated by the familiar hurdles of Pakistan’s industrial sector: fuel availability, power outages and cyclical swings in real estate and consumer spending. The company’s operating philosophy – keep furnaces hot, run

at optimal load, and flex energy sources – is a product of that environment and helps explain why even temporary demand dips can have outsized effects on utilisation, inventories and export behaviour.

Baluchistan Glass, for its part, has cycled through periods of retooling and capital refresh. Today’s BMR phase is more comprehensive, reflecting both the structural need to secure reliable gas and the commercial opportunity to position Hub as a low-cost site for pharmaceutical glass with port-proximity advantages once the line is ready.

Tariq Glass’s portfolio is anchored by two pillars:

• Float glass: the sheet glass used in construction, automotive glazing and interior applications – accounts for about 70% of revenue and sits in a market where Tariq Glass commands roughly half the share.

• Tableware: tumblers, stemware and related household and hospitality items – contributes about 30% and is an area where the company estimates 60–70% share, reflecting brand strength, breadth of designs and scale.

On the input side, the company sources silica sand and soda ash domestically at the prices cited above, blending cost vigilance with energy self-generation to manage unit economics. The mention of a waste-heat recovery project signals further optimisation ahead, a common route for heat-intensive industries to trim fuel bills and carbon footprint.

Baluchistan Glass has traditionally produced a range of container and table glass from its three units, but with operations paused for BMR, management is preparing a pivot into pharmaceutical glass, leveraging Hub’s proximity to the port to enhance export competitiveness for vials and related products once production resumes. That focus mirrors regional trends, where pharma packaging has offered higher value-add and more resilient demand than some commodity container categories.

On the near-term outlook, Tariq Glass appears cautiously constructive.

With solar now at 3.5 MW out of a 10 MW need, management will continue to optimise the daily power mix, toggling between in-house generation and the grid to minimise costs. The waste-heat recovery plan is meant to harden that advantage and reduce exposure to WAPDA’s unplanned shutdowns, which have previously dented output.

Given soft demand, one furnace remains offline and may not be reignited until inventories normalise and local demand strengthens. If the real estate sector picks up as anticipated, float-glass demand should follow, allowing the first furnace – already at optimal capacity – to run harder and the offline unit to return.

The company’s commanding mar-

ket share provides room to defend margins through pricing, even if volumes advance slowly. FY25 data – gross margin at 31% and EBITDA up 32% – suggest this stance has worked so far.

For BGL, the priority is to complete the gas pipeline, secure consistent gas pressure and restart Unit 1 in Q3 FY26. Post-restart, distribution will be built gradually, replacing the current arrangement under which Tariq Glass channels sales. Units 2 and 3 will undergo renovation and possible furnace redesign thereafter.

Risks remain. Fuel and power costs are still elevated and volatile; grid outages can upset production schedules; and the broader macro environment may yet crimp construction activity. The FY25 tax burden also rose, clipping the net margin even as operating performance improved. But between self-help on energy, pricing power anchored in share, and a clear rehabilitation plan at the subsidiary, Tariq Glass looks positioned to navigate a slow-demand year while protecting profitability.

Glass is an unforgiving business: furnaces are capital-intensive, hungry for heat, and happiest when running flat out. When demand wobbles, the choices are all suboptimal – carry inventory, discount, or export at thin margins –and each carries a cash cost. Tariq Glass’s FY25 playbook shows how scale and share can soften that blow. By adjusting prices, watching costs and tightening the energy mix, the company delivered double-digit growth in operating profit with only low-teens growth in sales.

At BGL, the task is more elemental: secure gas, finish the pipeline, restart the plant. The cost differential between Hub (SSGCL blend) and Punjab (SNGPL RLNG) underscores why Unit 1 gets priority – the effective gas rate of roughly Rs2,300–2,350 per MMBtu at Hub is materially better than around Rs3,000 under RLNG in Lahore/Kot Abdul Malik. That gap, along with port adjacency for exports, is the economic logic behind a pharmaceutical-glass push out of Hub.

If management can reignite unit capacity as demand returns – particularly with any real-estate recovery – Tariq Glass’s float segment should see the most immediate lift, given its 70% contribution to revenue and the relatively low elasticity of architectural glass once building activity resumes. Tableware should continue to be a margin and mix lever, especially where the company enjoys 60–70% share.

For investors and industry watchers, FY25 will read as an exercise in controlled execution: growth eked out via price and cost, capacity held in reserve until demand warrants, and a subsidiary taking methodical steps back to production. It is not a roaring expansion story. But in a sector where energy arithmetic often dictates outcomes, it is a coherent one. n

Rehmat

Ali Hasnie

emphasizes role of financial ecosystems in driving national growth

MPress Release

r. Rehmat Ali Hasnie, President & CEO of National Bank of Pakistan (NBP), emphasized the crucial role of ecosystems and the financial and banking sector in driving national growth during the Pakistan Business Summit recently held in Peshawar.

The summit, themed “Shaping What’s Next,” was organized under the patronage of the Governor of Khyber Pakhtunkhwa and co-hosted by the Nutshell Group and Al Baraka Bank (Pakistan) Limited, with the Overseas Investors Chamber of Commerce and Industry (OICCI) serving as the Strategic Partner.

During the session titled “Dialogue on The Symphonies of Ecosystems”, Hasnie highlighted that NBP was the first institution in Pakistan to introduce renewable financing and reaffirmed the bank’s commitment to supporting sustainable energy and contributing to the country’s green transition. He noted that the bank’s profitability is closely linked to Pakistan’s development goals and the needs of its people. He added that reforms, along with efforts to build investor confidence, are essential to attract investments in challenging sectors.

“While the bank focuses on stable and impactful sectors rather than high-risk areas, building trust and investor confidence remains equally important for growth,” Hasnie said. He also stressed that empowering citizens through financial inclusion and broader access to finance turns them into active contributors to the economy, strengthening local communities and fueling sustainable development across the country.

The session was moderated by Sajeed Aslam, Partner & Co-Founder of Spectreco LLC, USA. Panelists included Muhammad Nassir Salim, President & CEO of HBL; Jahangir Piracha, MD & CEO of Fauji Fertilizer Company Limited; Jahanzeb Khan, President & CEO of easypaisa Digital Bank; and Muhammad Ali Gulfaraz, CEO of Dubai Islamic Bank Pakistan Limited.

Asif Saad

Pakistan’s Economic Gridlock: Why Ignoring the SME Sector Keeps the Economy Stagnant

Pakistan’s economy remains trapped in familiar cycles, from current account deficits, debt crises to IMF bailouts, and recurring promises of reform repeated umpteen times. Whilefiscal and monetary adjustments dominate public debate, the structural roots of Pakistan’s economic stagnation run much deeper. There are complex multi-dimensional issues but one key aspect which does not get much attention is that the country’s development strategy continues to prioritize large corporates and capital-intensive projects while sidelining small and medium enterprises (SMEs) which are the real drivers of innovation, jobs, and inclusive growth in most advanced economies. In the following paragraphs I will discuss why this is so and what can be done to change this model.

The Structural Bias Toward Big Business

For decades, successive governments have viewed mega-projects as symbols of national progress with mining ventures like Riko Diq, large energy plants, and CPEC infrastructure as some examples of this phenomenon.

The writer is a strategy consultant who has previously worked at various C-level positions for national and multinational corporations

While these projects are appreciated for attracting foreign capital, they have limited linkages with local industries, do not build domestic supply chains and play a minimal role in job creation. Pakistan’s heavy reliance on foreign-funded mega-projects is a symptom of short-term economic management rather than long-term strategy.

While large mega projects may improve infrastructure and generate additional tax revenues, they often come at the cost of government subsidies. Furthermore, they do little to strengthen the domestic industrial base. It’s not that these projects shouldn’t be pursued, but rather what should be prioritized.

The Missing Middle in Pakistan’s Economy

In contrast, SMEs provide the connective tissue of an economy, enabling productivity, creating jobs in the communities where they operate and providing social mobility for entrepreneurs and their families when the business is successful.

The real growth multiplier lies in empowering hundreds of thousands of SMEs, enterprises that reinvest profits locally, employ from within communities, and build resilient domestic supply chains.

Yet in Pakistan, they are hampered by excessive regulation, underfinancing and an absence of targeted policy support.

SMEs contribute roughly 40% of Pakistan’s GDP, employ more than 80% of non-agricultural labor, and account for about 25% of exports (SMEDA, 2023). However, they receive less than 8% of private sector credit (State Bank of Pakistan, 2023).

This imbalance has hollowed out the middle of the economy leaving a narrow corporate elite at the top, a massive informal sector at the bottom, and few scalable enterprises in between. Without medium-sized firms, productivity, innovation, and exports all stagnate.

Lessons from Developed Economies

While we often hear about large companies from developed countries due to their international brand names and global presence, we don’t realize that advanced economies owe much of their resilience to strong small and medium-sized enterprises (SMEs). The table below illustrates how SMEs underpin sustainable growth in some of these nations;

In contrast, underdeveloped economies like Pakistan, India, and Bangladesh have among the lowest SME contributions to GDP typically 25–40%, compared to 45–60% in developed markets (World Bank Enterprise Surveys, 2023; ADB SME Monitor, 2022). This gap underscores how lagging SME productivity and weak institutional support perpetuate low growth and limited formal employment across South Asia.

Protecting SMEs and Startups: A Case for Policy Shelter

If Pakistan wants its small enterprises to thrive, it must protect them from premature taxation and bureaucratic overload until they achieve viable scale. Overregulation and early compliance requirements discourage entrepreneurship and formalization.A new economic strategy must shift from top-heavy corporatism to bottom-up enterprise empowerment.The following policy recommendations may be considered for this change to be realized. It is important to note that these don’t come from a cookie-cutter governance, financial, or economist perspective. Instead, they come from my first-hand experience and knowledge gained from working in the corporate world and with many small and medium-sized businesses.

1. Graduated Taxation: Introduce turnover-based or simplified tax regimes for startups and micro-enterprises during their initial years. The first rupee in revenue in Pakistan attracts anywhere from approximately 5-20% sales tax and minimum turnover/income tax. This is before the business has any sound footing or ongoing customers.

United States ~44% ~47% SMEs drive innovation and tech diffusion. European Union (average) ~50–56% ~66% Simplified regulation and SME-friendly credit fuel competitiveness.

Japan ~53% ~70% SMEs form the backbone of high-value manufacturing.

South Korea ~48% ~88% Strong SME–chaebol linkages sustain export dynamism.

China ~60% ~80% SME clusters anchor industrial and export expansion

It can singularly destroy a business and any entrepreneurial spirit behind it. The fact that most business do not pay and end up gaming the system does not justify the existence of an onerous system in the first place.

Instead, a legal protection clause should be enshrined in law that SMEs remain exempt from complex taxation and heavy compliance until they cross defined turnover or employment thresholds.

Some of these tax regimes may already exist but are found too cumbersome for anyone to benefit on a consistent basis. The need is to simplify all aspects.

2. Credit Access: Mandate SME-lending quotas for banks and expand credit guarantee schemes to share default risk. Require financial institutions to allocate at least 20% of private-sector lending to SMEs and encourage them to take calculated risks as any business would. Bring in a regulatory regime for banks to do away with the requirements of securing debt to new businesses and start-ups.

3. Streamlined Compliance: Establish a digital “one-window” system for business registration, taxation, and reporting. Include

opening as well as shutting of businesses in this one-window operation. By facilitating closure of unfeasible businesses, make it acceptable for entrepreneurs to take risks and fail and learn from their experience.

4. Scale-Based Regulation: Apply incremental compliance thresholds (micro → small → medium) as firms expand. This is in line with the recommendation on taxation. Allow small businesses to survive and exist before putting the burden of compliance on them. Encourage early-stage corporatization but facilitate those who follow this path without overburdening them with so much regulatory compliance.

5. Digital and E-Commerce Enablement: Integrate small businesses into digital marketplaces and fintech networks to boost productivity and transparency. Instead of making fintechs and marketplaces behave like banks, structure these to facilitate SME transactions.

6. Vocational Alignment: Link technical education with SME needs in manufacturing and digital sectors. With a population growth at the highest levels in the world and our education system unable to meet the needs of this demographic boom, vocational training programs are imperative for the society. Linking these directly to the needs of SMEs can ensure that much needed employment is generated.

From Mega Projects to Micro Powerhouses

Pakistan’s future prosperity will not come from a single foreign investor or project, not from Riko Diq, CPEC, or IMF tranchesbut from hundreds of thousands of small enterprises that produce, innovate and employ. To make that possible, policymakers must protect small businesses from over-taxation and bureaucratic friction, giving them the room to grow. This is not charity; it is smart economics. Every developed economy has built its foundation on SMEs. Unless Pakistan learns that lesson and reorients toward bottom-up growth, its reform agenda will remain incomplete, and its economic sovereignty perpetually constrained. n

Trump’s tariffs on China are causing Pakistan’s food imports to go up, and possibly food prices to go down

The tariffs on China have caused a wave of discontent among Trump’s base in America’s corn-belt. Pakistan is among the many countries that offer part of a larger alternative

By Abdullah Niazi

On the 6th of May 2025, a delegation of the US Chamber of Commerce accompanied by United States Charge d’Affaires in Pakistan, Ms Natalie A. Baker met with Commerce Minister Jam Kamal Khan. Members of the US-Pakistan Business Council (USPBC) were also there.

In the world of business and trade diplomacy, this was a very small first step. Pakistan had been slapped with a 29% tariff by the Trump Administration in April as the US revealed a long list of countries hit by the new policy. The major brunt in the region had been taken by China. With Donald Trump claiming he was open to renegotiating the tariffs with different countries and striking trade deals, the sit-down meeting with the commerce minister was meant to open a channel of communication on the pressing issue.

But even as the delegations exchanged pleasantries, one topic dominated the conversation: soybeans. More specifically the import of soybeans from the United States into Pakistan. Soybeans are a major cash crop in the United States and vital to farmers that populate America’s midwest region. Traditionally, China has been the biggest market for soybeans, buying more than half of the $24.5 billion worth of soy products produced in the US. Those orders have fallen by more than half since the tariffs went into effect.

The sentiment among American farmers has slowly but surely been turning. States like Iowa, Illinois, Indiana, Ohio, Missouri, Kansas, Kentucky, and Nebraska make up not just the heart of Trump Country but also the bulk of US soybean production. These farmers have been complaining vocally, and Trump is fast losing goodwill in the region.

While the US has its horns locked with China in the trade tussle, in the meantime the Trump Administration has been trying to find other markets for its soybeans. Among these is Pakistan. Charge d’Affaires Baker made it a point to mention that the resumption of US soybean exports to Pakistan signifies the growing partnership between the two countries in the meeting with the commerce minister. Pakistan has been an importer of US Soybeans

for some years, but a major hurdle emerged in 2023 when consignments of soybeans were stopped at Karachi port and the government placed a ban on them over GMO issues. A year of lobbying and diplomatic engagement have reversed that ban, and soybeans were poised to be a major commodity that could help seal a trade deal between Pakistan and the United States.

The day after the meeting, India launched strikes into Pakistan triggering a conflict that saw both sides breach territorial sovereignty to hit strategic targets. The discussion on soybeans was lost in the chaos. After four days of fighting President Trump announced he had brokered a ceasefire, leveraging trade with the United States as a bargaining chip.

That was six months ago. Since then Pakistan has continued to import soybeans from the States. In fact, soybean imports are one of the reasons Pakistan’s food import bill has gone up so drastically this year. In the first three months of this financial year, soyabean imports reached 52,054 metric tonnes, up 70.89% from 30,460 metric tonnes in the same time period last year. In terms of value the imports hit $56.5 million compared to $29.57 million last year.

Overall, Pakistan is expected to import 1.1 million metric tonnes of soybeans this year worth over $500 million. This is a significant increase compared to how much soybean Pakistan imported even before the 2023 ban. In the years preceding the ban, Pakistan was importing 950,000 metric tonnes of soybeans at $380 million on average every year from 2019 to 2022 according to the United States Department of Agriculture.

On the surface, the increased import of soybeans is a strain on Pakistan’s dollar reserves. The food import bill has already been rising because of the excesses of the sugar industry, rising demand of other commodities, and increasing prices in the global markets. However, if Pakistan’s policymakers can leverage Trump’s trade war with China, soybeans can be a reason for cooperation between the two countries that might help Pakistan get better trading terms with the United States compared to the rest of the world. On top of this, if used correctly, soybean can play a part in making protein like chicken, fish, and even meat cheaper in Pakistan.

The soy story

Before we get into the details of how this is possible, it is important to understand the position that soy holds in global trade. Soy has an image problem. The term ‘Soy Boy’ is listed on Urban Dictionary with the uninspiring definition of “Used pejoratively, to describe a man perceived as lacking traditional masculine traits, typically implying passivity, timidity, or emotional sensitivity.” The term emerged from the use of soy in vegan products such as tofu, soy milk, and veggie burgers.

The reality is starkly different. As a recent article by Vox describes it, Soy is actually “the invisible backbone supporting modern, meat-heavy diets. The overwhelming majority of soy on Earth (about 77%) is grown to feed not humans but the billions of chickens, pigs, and cows raised to feed us, supplying the chief protein source in livestock diets.

Soy has gone from a niche East Asian crop grown to produce Miso and Tofu to a behemoth of American Agriculture. First planted in North America in 1765, soy farmers have strong associations and collectives that not just lobby for their interests but also advocate and market US Soy across the globe. Back in May, the very same day that the US delegation was meeting with Pakistan’s commerce minister, another event related to soy was taking place in Colombo. At a sustainability summit organised by US organisations, representatives from the United States, Sri Lanka, Pakistan, India, and Bangladesh were in attendance and held discussions with a number of American soy farmers. Profit’s correspondent attended this summit.

In the wake of the tariffs imposed on China, soy farmers expressed alarm. The conversations were strange. All of the farmers we spoke to said they had voted for Trump, yet none of them were happy with the tariffs on China. All of them agreed that in the absence of Chinese buyers, they would have to focus on the South Asian market to get by. The strategy was clear. The farmers were going to push to open the Chinese markets up again, but until that happened, it was worth developing other countries.

Pakistan’s position in this has been a bit nightmarish because of what happened in 2023.

Keeping channels open

Pakistan already imports a lot of edible oil. In fiscal year 2024-25, Pakistan’s palm oil imports were projected to reach 3.8 million tons, accounting for over 75% of the nation’s edible oil consumption. In the first three months of this fiscal year, the value of palm oil imports surged to $1 billion, up from $746.41 million in the same time period last year. Soybeans have remained the second biggest import for Pakistan when it comes to edible oil.

In 2023, shipments worth $300 million were stopped at Port Qasim over concerns regarding GMOs. The main concern regarding soybean has been that since the soy grown in the United States is genetically modified, there is something wrong or unnatural about it. This is a position not supported by science, but the concerns surrounding this remain as prevalent in Pakistan as homeopathy. That story has been covered in quite some detail by Profit in the past.

However, now that the soy is being imported there might be some benefits to it. In the three decades since 1990, the consumption of oilseed meals as feed for livestock has tripled in the country – a big reason for which is the growth of the poultry industry.

Pakistan’s poultry equation

This is what it all boils down to. Chicken is important to Pakistan, and this is not a particularly old phenomenon.

Commercial poultry production in Pakistan started in the 1960’s and has been providing a significant portion of daily proteins to the Pakistani population ever since. In fact, up until the 1960s, chicken was a meat more expensive than beef.

Before 1963, Pakistan’s poultry industry was dominated by the native “desi” chicken, which produced only around 73 eggs annually. A turning point came in 1966 when the University of Agriculture Faisalabad developed the “Lyallpur Silver Black,” a new breed capable of producing over 150 eggs per year and gaining 1.4 kg in 12 weeks. This breakthrough made poultry farming more profitable and accessible, prompting government support through tax exemptions, the establishment of hatcheries and feed mills, and FAO-assisted research centers.

Institutionalisation followed with the creation of the Federal Poultry Board in 1972, and the 1970s saw rapid expansion as Sindh offered land leases and investors shifted capital from nationalised industries into poultry. Between 1976 and 1980, commercial egg output nearly doubled to 1.2 billion, and broiler production rose from 7.2 to 17.4 million birds.

Despite periodic setbacks due to disease

and infrastructure challenges, poultry emerged as Pakistan’s most affordable protein source. A 2020 Planning Commission report noted poultry prices remained 50% lower than beef and below CPI growth, spurring higher consumption. Today, poultry is Pakistan’s second-largest industry, contributing nearly 29% to total meat production and providing livelihoods to millions across rural areas. It also provided an alternative source of protein. “Mutton prices are about 100% higher than beef prices whereas poultry prices are 50% lower than beef. This price trend has induced poultry meat consumption while discouraging mutton and beef consumption during the period,” it reads.

“The prices of all types of meat are increasing, but the increases in mutton and beef prices are the highest, higher than the CPI, while the increase in poultry price is lower than that in CPI. Partly beef and mainly poultry can fill the gap created by the declining mutton consumption in the country because of the exorbitant increase in price of the latter and relatively cheaper prices of the former two meats. A common observation is that the red meat butcher shops have added chicken to their offering.”

Poultry’s role in Pakistan depends entirely on access to good poultry feed that increases the protein levels found in chicken meat. Soybeans provide a source for nutritious meals for chicken. When the import of United States soy was banned back in 2023, the impact on price was almost immediate. In various markets of Rawalpindi and Islamabad, Rs 60 per kilogramme price difference for live chicken was being observed, with the rates ranging between Rs 390 and Rs 450 per kg, according to a report in Dawn.

A simple equation

Pakistan is left with a very simple equation here. On the one hand, increasing imports are bad for the economy. On the other, in a very fast changing

world, Pakistan needs to establish a mutually beneficial trading relationship with the United States. For the Trump Administration, it is important to find buyers for soybean farmers. Since there is a genuine demand for soybeans in Pakistan, imports of the commodity can be used to find areas of mutual interest for both.

While Pakistan is not particularly important to the United States, the US is a very important economic relationship for Pakistan. Despite accounting for just 0.16% of total U.S. imports, the American market holds outsize significance for Pakistan’s export economy, serving as its single largest export destination with an annual volume of around $6 billion — roughly 18% of Pakistan’s total exports.

Many Pakistani analysts have been examining the tariffs placed on Pakistani exports in the context of how high the tariffs are on countries that compete in the same export sectors. There is certainly at least some value to measuring that number.

However, one important way to think about the potential impact on global trade from these tariffs is to consider not just whether they will shift demand away from Vietnam and towards Pakistan, but rather to ask what will be the absolute level of tariff impact. If history is any guide, the results could be quite catastrophic.

Pakistan has been lucky enough after the conflict with India that the Trump Administration has been very welcoming to the Pakistani leadership. Along with cooperation on global issues, there have been discussions of investments in minerals. In the midst of this, soybeans are a small aspect, but it is definitely important to this particular administration given that farmers are part of their base. Pakistan would do well to remember it is a commodity they can use to their advantage not just in securing better trade terms, but also as a valuable addition to the country’s food supply chain. n

Atlas Battery sticks with lead-acid, even as lithium-ion gains traction

Revenue down 15%, profits down 93% in 2025 as management insists that lead-acid manufacturing remains their core strategy

Profit Report

Atlas Battery Ltd closed fiscal 2025 with sharply weaker results and a steadfast message: despite the lithium wave, lead-acid remains its core.

The company’s stance sets up a revealing contrast with Treet, which is moving into lithium-ion through a tie-up with a Chinese partner and, according to recent reporting, is preparing local manufacturing capability. The strategic fork comes just as Pakistan’s policy push and consumer interest edge toward electric mobility – a category dominated by lithium-ion chemistry.

Atlas Battery’s top line fell and profitability deteriorated materially in FY25. Net sales declined 15% year-on-year to Rs35.2 billion (FY24: Rs41.5 billion) as unit volumes slipped and consumers migrated from heavy to medium-sized batteries, which carry lower average realisations. Gross profit dropped 33% to Rs4.0 billion, pulling the gross margin down to 11% from 14% a year earlier. Operating profit tumbled 54% to Rs1.8 billion, while EBITDA fell 47%. After finance costs and tax, profit after tax plunged 93% to Rs91 million, dragging net margin to effectively 0% (FY24: 3%) and earnings per share to Rs2.60 (FY24: Rs38.37). The company paid no dividend for FY25 (FY24: Rs20).

The fourth quarter told the same story in miniature. Q4 sales were down 8% versus the same period last year; gross profit fell 43%; operating profit sank 62%; and quarterly EPS slid to Rs2.15 from Rs16.84 a year earlier.

Management said the mix shift away from heavy batteries – historically a richer profit pool – and a visible consumer move toward medium-sized units were key drags on margin resilience. With 82% of sales coming from the automotive replacement market, the company is highly sensitive to changes in vehicle-park behaviour and affordability.

Two other pressure points came through in management’s briefing. First, the company reported a 10% decline in AMB sales within replacements, partially offset by a 22% rise in MCB volumes – a mix effect that further diluted average selling prices. Second, while Atlas does not see a major import threat in conventional lead-acid, it does worry about the “rising influx” of lithium-iron batteries – often premium-coated, imported variants – which could squeeze local makers on pricing. Management does not expect margins to improve over the next two years, given the demand shift away from heavy vehicles, which used to contribute a disproportionately high share of profits.

The macro backdrop has not fully filtered into sales volumes, management said, but unit sales were still down 6–7% year-on-year. Atlas intends to keep focusing on operational efficiencies and says it will pass through 80–90% of any cost benefits to customers – a reminder that in a commoditising pool, pricing remains the primary competitive lever. On market structure, the company estimates Pakistan’s total battery demand at roughly 10 million units annually, with Atlas holding around 20% share, underlining how sensitive its P&L is to even slight shifts in mix and channel.

If Atlas Battery’s posture is one of in-

crementalism – drive efficiencies in lead-acid; watch lithium from the sidelines; and consider selective, low-capex adjacent steps – Treet Battery is striking a different tone. In September, Treet announced a strategic agreement with Highstar Digital Energy Technology (Guangdong) Co., a Chinese energy-storage specialist, to import and sell lithium-ion batteries in Pakistan, explicitly marking an entry into the lithium segment alongside its legacy lead-acid franchise. Multiple outlets covered the move and framed it as the company’s first formal step into lithium in anticipation of growing demand from energy storage and electric mobility.

Beyond distribution, recent business reporting also indicates Treet’s plan to set up a lithium-ion battery plant in collaboration with a Chinese partner, signalling an intention to localise at least part of the value chain rather than rely solely on imports. While timelines and capex envelopes remain to be fully disclosed, the direction is clear: Treet is aligning itself with the chemistry that powers EVs and stationary storage globally.

Atlas, by contrast, told investors it sees lithium-iron battery manufacturing as unviable in Pakistan for now because of high capex, though partial or full-scale assembly could be feasible. The company acknowledged that over 20 importers are already bringing in surplus lithium-iron stock from China and “dumping where there is demand,” a market dynamic that favours traders over manufacturers at this stage. Even so, management added that it plans to enter the lithium-iron space by next year via a low-capex approach – a qualifier that suggests distribution, assembly or small-

scale localisation, not a greenfield cell or pack gigafactory.

This strategic divergence matters. As lithium-ion batteries become the default for EVs and advanced storage – and as costs continue to fall – the competitive frontier will shift toward players that can offer reliable lithium products, whether imported, assembled or locally manufactured. Atlas’s focus on lead-acid, with selective lithium adjacency, tracks its installed capabilities and brand strength; Treet, in contrast, is leaning into the new chemistry early, betting that demand will justify deeper localisation over time.

Pakistan’s EV transition is still in its early innings, but momentum is building – particularly in two- and three-wheelers, where total cost of ownership can flip in favour of electrics sooner. The federal government unveiled an updated EV Policy 2025–30 this year, including over Rs100 billion in subsidies targeted at electric bikes and rickshaws, and reiterating ambitions for faster adoption. Earlier frameworks – the National EV Policy (2019) and related guidelines – already created incentives such as reduced customs duties on EV-specific parts and components, sales-tax relief, and duty exemptions on charging infrastructure equipment.

The on-ground signal has followed: local media report surging sales of electric motorbikes, with around 15,000 units in July 2025 alone across dozens of assemblers – up from a mere 2,000 units in 2022 and 6,000 in 2023. While four-wheel EV penetration remains small and overall industry analysts still call EV share “negligible” in Pakistan’s auto market, the policy tilt and consumer experimentation are unmistakable.

Global currents are stronger still. Worldwide EV sales hit a record 2.1 million in September 2025, up roughly 26% year-on-year, driven by China, Europe and the U.S., according to research firm Rho Motion – a reminder that the technology learning curve and supply-chain scale continue to improve. Pakistan will not be immune to the deflationary pull of that global scale, especially as local assembly footprints emerge.

Indeed, EV localisation steps are being announced. BYD – the world’s largest EV maker – says it aims to begin assembling EVs in Pakistan by mid-2026 via a joint venture with a local partner, initially targeting 25,000 units per year on double shifts. Earlier, the firm’s local venture projected that EVs could account for up to 50% of sales by 2030 (ambitious by any measure), and highlighted plans for early charging-station roll-outs. Even if real-world penetration ends closer to 30% in that timeframe, the direction of travel clearly favours lithium chemistry.

Why does this matter for Atlas? Because

EVs do not use lead-acid traction batteries. While lead-acid will remain relevant for starter-lighting-ignition (SLI) in internal-combustion and for some backup applications, the growth wedge – the incremental market that expands total demand – is in lithium-ion across two-wheelers, three-wheelers, buses, cars and stationary storage. In that sense, a lead-acid-only stance risks becoming the proverbial “buggy whip” during the rise of cars: still necessary for a time, but progressively peripheral as the core market pivots.

To its credit, Atlas is not entirely ignoring lithium. Management’s plan to explore a low-capex entry and its acknowledgement that medium-sized batteries (including for energy storage) are gaining share show a pragmatic appreciation of where demand is going. But with over 20 importers already active and competitors like Treet planting lithium flags, speed and clarity of execution will matter – especially if policy nudges accelerate EV adoption and domestic assembly catalyses price declines.

Atlas’s sales mix is dominated by lead-acid batteries across automotive and energy applications. Management describes a visible shift from heavy to medium-sized batteries – used both in vehicles and energy-storage – driven by more efficient appliances and the growing adoption of lithium technology, which is reshaping demand patterns even within the incumbent chemistry’s addressable spaces. In the replacement market – which accounts for roughly four-fifths of total sales – Atlas competes primarily on brand, distribution reach and service.

Historically, Atlas has marketed its products under the AGS brand (a portmanteau of Atlas and GS, after its Japanese technical collaborator). Its range spans conventional flooded lead-acid batteries for passenger cars, trucks, tractors and heavy vehicles, as well as motorcycle units and batteries for industrial and stationary uses. In recent years the company has also offered maintenance-free and deep-cycle variants for UPS/solar segments, consistent with broader market evolution.

Yet even in these traditional lines, the unit-economics are getting harder. As the FY25 numbers show, a tilt to mid-sized batteries and muted pricing power can squeeze gross margins. Atlas does not expect margin relief for two years, absent a reversal in mix or a step-change in cost structure. Meanwhile, in lithium-iron (a term local market participants often use interchangeably with lithium-ion iron phosphate), the company says traders currently capture more value than manufacturers, because they can opportunistically source surplus Chinese stock and dump into pockets of demand. That dynamic is difficult to counter without stronger localisation or a differentiated brand and service proposition in lithium.

Atlas Battery is one of the oldest companies in the Atlas Group, established in 1966 as part of a strategy to bring Japanese battery technology to Pakistan. In 1969, the company signed a technical collaboration with Japan Storage Battery Co. – now GS Yuasa – and began production under the AGS brand, where “A” stands for Atlas and “GS” for Genzo Shimadzu, the Japanese firm’s founder. Over five decades, Atlas has grown into a nationwide operation with manufacturing in Karachi and branch networks in major cities, supplying batteries for the full spectrum of automotive and industrial uses.

The group pedigree matters. Atlas Group’s long-standing joint ventures with Japanese manufacturers (notably in two-wheelers and cars) steeped the battery company in quality and process discipline, which helped AGS build a loyal base in the replacement market. But the same legacy strengths can become anchors if they delay decisive pivots when technology shifts. The move from hard-rubber to polypropylene casings, from conventional to maintenance-free, and now from lead-acid to lithium-ion are all chapters in that continuous upgrade curve.

The FY25 update shows Atlas at a crossroads common to many legacy battery makers worldwide. The company still commands significant share in a 10-million-unit national market, but the growth engine is moving. Management’s own briefing notes acknowledge that lithium-iron manufacturing is capital-intensive and not yet viable locally; nevertheless, the firm says it intends to enter the space next year with a low-capex approach. That line suggests Atlas sees lithium as inevitable – the question is how and when to participate without breaking its balance sheet.

Atlas Battery’s FY25 numbers reveal a business grappling with an unforgiving combination: softer volumes, adverse mix and margin compression. Management remains convinced that lead-acid will be its anchor for the foreseeable future, though it now concedes the need for a low-capex entry into lithium-iron. That caution contrasts with Treet’s more assertive push into lithium through an international partnership and reported manufacturing ambitions.

In an environment where policy nudges, consumer curiosity and global cost curves are all leaning toward lithium-ion, a purely lead-acid posture risks becoming the “buggy whip” of Pakistan’s battery industry. Atlas still has a strong brand, a powerful replacement channel and a large domestic market – but the growth narrative is shifting to where the electrons are: lithium packs for two- and three-wheelers, autos and storage. FY25 may be remembered as the year the company’s numbers forced the strategy debate into the open. n

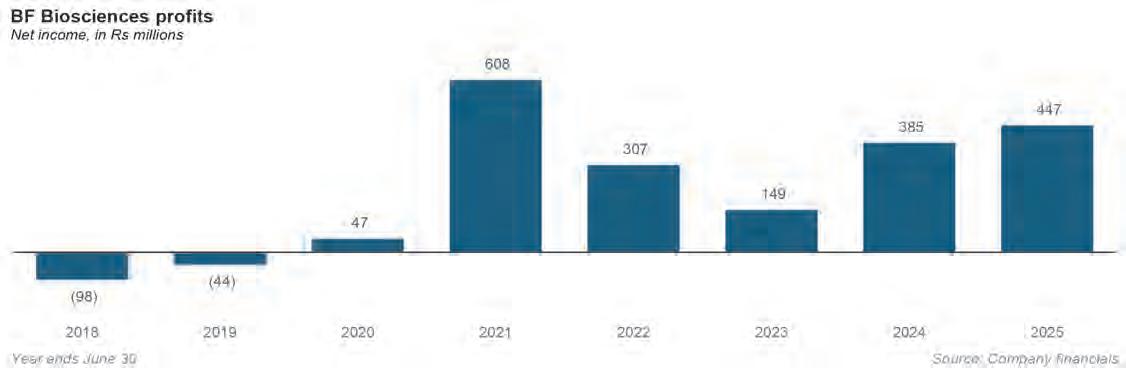

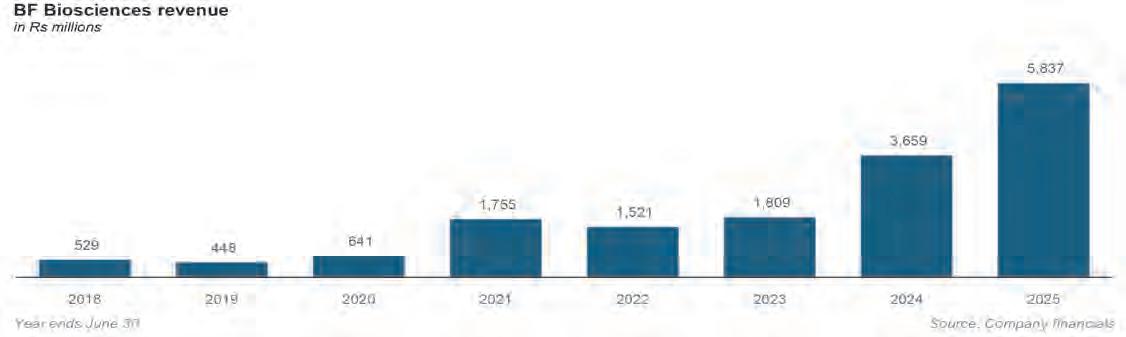

BF Biosciences brings GLP-1 manufacturing to Pakistan

The biopharmaceutical company is producing tirzepatide – marketed globally by Eli Lilly as Zepbound – at a factory built with its IPO proceeds

BProfit Report

F Biosciences Ltd has begun local manufacturing of tirzepatide, bringing one of the world’s most sought-after metabolic drugs into production on Pakistani soil. In a material disclosure to the Pakistan Stock Exchange, the company said it has launched Zeptide (tirzepatide) in an easy-to-use pre-filled syringe, produced at its new European-specification pre-filled syringes facility. The company added that developing Zeptide was included in the utilisation plan for its initial public offering (IPO) proceeds, signalling that funds raised from public investors are now translating into tangible capacity and product roll-out.

Tirzepatide – an injectable therapy that acts as a dual agonist of the GLP-1 (glucagon-like peptide-1) and GIP (glucose-dependent insulinotropic polypeptide) receptors – is approved by the United States Food and Drug Administration (FDA) for treating type-2 diabetes and obesity. The formulation is being released in patient-friendly, pre-filled syringes, a format the company says reduces dosing errors. Independent testing of Zeptide’s quality and potency has been conducted at leading mass spectrometry facilities in the US and at a national university in Pakistan, according to the filing.

While Eli Lilly markets tirzepatide globally under the brands Mounjaro (for type2 diabetes) and Zepbound (for obesity), BF

Biosciences is introducing the molecule locally as Zeptide. The company did not disclose a branded-product licensing arrangement with Lilly in its filing; instead, it framed Zeptide simply as locally manufactured tirzepatide developed as part of its IPO investment plan, leaving the provenance of its intellectual property undisclosed.

The start of tirzepatide manufacturing is a notable first for Pakistan’s life-sciences sector. GLP-1-based medicines – and now dual GLP-1/GIP agonists – are reshaping standards of care in diabetes and obesity worldwide. By commissioning a pre-filled syringe line and launching Zeptide, BF Biosciences is positioning itself at the leading edge of this therapeutic wave.

In its PSX notice, the company said Zeptide is produced at a newly commissioned European pre-filled syringes facility, and the product’s development featured in the IPO proceeds utilisation detailed in its prospectus. This indicates that capital raised in late 2024 has been deployed into high-value, high-complexity sterile fill-finish infrastructure rather than only into working capital or incremental upgrades.

Market watchers had anticipated such a move from BFBIO since its listing. Reporting at the time of the announcement captured the company’s intent to leverage the new plant to address critical unmet needs in metabolic disease, with local media noting the commercial launch of Zeptide and the company’s confidence that it would support growth.

From Ferozsons

subsidiary to listed biotech

BF Biosciences is best understood as the biopharmaceutical manufacturing arm born out of Ferozsons Laboratories Ltd, one of Pakistan’s best-known pharmaceutical groups. Established in 2006, BF Biosciences began life as a joint venture between Ferozsons (then 80%) and Argentina’s Bagó Group (20%), with a remit to build Pakistan’s first biotech formulation plant. Over the past decade and a half it has specialised in complex products – including oncology and hepatology – and has increasingly invested in sterile and pre-filled syringe capacity.

The company listed on the Pakistan Stock Exchange in October 2024 after a well-received IPO. The prospectus set a floor price of Rs55 per share, which the company easily exceeded with a final strike price of Rs77 per share, raising Rs1.93 billion in the offering. The post-IPO shareholding is Ferozsons (about 57.4%) and Bagó (about 14.3%), with the free float held by public investors – establishing BF Biosciences as a publicly traded, Ferozsons-anchored platform for complex manufacturing.

PSX and financial-press coverage of the listing underscored BF Biosciences’ role in catalysing biotech manufacturing in the country. A PSX gong ceremony press note described the company as a joint venture that has “spearheaded Pakistan’s emergence in biotech manufacturing”

– an ambition now extending into metabolic disease with Zeptide.

BF Biosciences’ filing explicitly links Zeptide’s development to the IPO utilisation plan, indicating that public capital is underwriting not only capacity but also the rapid localisation of globally validated therapies.

The rise of GLP-1s –and how tirzepatide stacks up against semaglutide

GLP-1 receptor agonists have become the most consequential class in metabolic medicine in a generation. Their use has expanded from glycaemic control to weight management and potential benefits across cardiometabolic endpoints. Within this class, tirzepatide (Lilly’s Zepbound/ Mounjaro) stands out because it is a dual agonist – binding both GLP-1 and GIP receptors – while semaglutide (Novo Nordisk’s Wegovy/Ozempic) is a GLP-1-only agonist.

A landmark head-to-head, randomised trial (SURMOUNT-5) published in the New England Journal of Medicine compared tirzepatide with semaglutide in adults with obesity without diabetes. At maximal labelled doses over 72 weeks, tirzepatide produced greater mean weight loss and larger reductions in waist circumference than semaglutide, with broadly similar gastrointestinal side-effect profiles.

That said, the evidence base is nuanced and still evolving. An observational, real-world analysis presented in 2025 suggested that semaglutide (Wegovy) was associated with a larger relative reduction in major adverse cardiovascular events than tirzepatide among high-risk patients without diabetes – an outcome that, while not from a head-to-head randomised CV outcomes trial, may weigh on prescribing for certain patient groups. As always, differences in study design and populations caution against over-extrapolation, but such data underscore how GLP-1 competition will likely be decided on multiple dimensions: weight loss, glycaemic control,

cardiovascular protection, tolerability, access and price. From a supply and market-access standpoint, the GLP-1 surge has strained global manufacturing. In late 2024, the U.S. FDA declared that shortages of tirzepatide products had been resolved, instructing compounders to wind down non-originator supply. Lilly subsequently said it was ramping production and easing startdose constraints. These developments matter for Pakistan because local manufacturing can buffer against global bottlenecks – especially if BF Biosciences’ fill-finish capacity proves scalable and compliant with export-market standards over time. Against that backdrop, BF Biosciences’ move can be read as a deliberate attempt to place Pakistan at the centre of the GLP-1 supply chain locally, with an eye to regional opportunities once registrations and certifications are in place.

Pakistan’s diabetes burden: the world’s highest prevalence

If the commercial logic for Zeptide seems compelling, the public-health logic is overwhelming. Pakistan’s diabetes burden is among the heaviest worldwide – and by some measures the heaviest of all.

The International Diabetes Federation (IDF) reports that Pakistan has the highest diabetes prevalence (ages 20–79) globally, with tens of millions living with the disease today and projections rising sharply to mid-century. The country also ranks near the top by absolute numbers of adults with diabetes – underscoring the scale of demand for safe, effective and accessible therapies. Earlier IDF editions and Lancet commentary painted a similarly stark picture: around 33 million Pakistanis living with diabetes in 2021, millions undiagnosed, and a rapidly worsening disease burden. Local press, citing IDF’s 10th edition, highlighted that roughly one in four adults –about 26.7% – were living with diabetes, placing Pakistan at or near the top of global prevalence rankings even then.

Whether the exact percentages vary by survey and definition, the combined picture is unambiguous: a population-level crisis in

weight-related and glycaemic health.

What does this mean for the tirzepatide opportunity? Millions are undiagnosed, and many of those diagnosed struggle with control and adherence. Long-acting injectables that improve glycaemic control and reduce weight can significantly affect downstream complications and costs if access barriers are addressed. Pakistan’s diabetes care has long leaned on oral agents and human insulin; the diffusion of GLP-1s has been constrained by price, availability and delivery formats. Local manufacturing of pre-filled syringes may modestly lower costs and improve convenience, supporting broader uptake.

Strategic implications for Pakistan’s lifesciences ecosystem

By investing in European-standard prefilled syringe lines, BF Biosciences is upgrading Pakistan’s sterile-injectables ecosystem. The company has already been expanding capacity with Drug Regulatory Authority of Pakistan (DRAP) approvals for additional pre-filled, liquid and lyophilised lines –steps that align with a pipeline that now includes high-demand metabolic products.

Medium-term, Pakistan could convert metabolic-drug manufacturing into export earnings if plants meet international GMP and secure registrations in targeted markets. Precedent exists in oncology and hepatology products made locally; GLP-1/GIP therapies add a new vector where demand is global and rising. BF Biosciences’ own communications around its IPO and listings pointed to ambitions beyond the domestic market, including certifications that enable exports. Tirzepatide is only one node in a crowded and fast-moving class. Semaglutide remains dominant globally in some segments –particularly with strong cardiovascular outcomes evidence – while oral GLP-1s, small-molecule incretin mimetics, and next-generation dual/ triple agonists are advancing. The local edge may therefore come from reliable supply, cost discipline, and delivery innovation (pens, titration packs) rather than molecule exclusivity alone. n

National Foods to divest Canadian wholesale and distribution subsidiary

Subsidiary sold for a valuation likely exceeding C$100 million, off an initial investment of C$6 million.

Profit Report