Books in this series are published to communicate the results of World Bank research, analysis, and operational experience with the least possible delay. The extent of language editing varies from book to book.

This work is a product of the staff of The World Bank with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy, completeness, or currency of the data included in this work and does not assume responsibility for any errors, omissions, or discrepancies in the information, or liability with respect to the use of or failure to use the information, methods, processes, or conclusions set forth. The boundaries, colors, denominations, links/footnotes, and other information shown in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. The citation of works authored by others does not mean The World Bank endorses the views expressed by those authors or the content of their works.

Nothing herein shall constitute or be construed or considered to be a limitation upon or waiver of the privileges and immunities of The World Bank, all of which are specifically reserved.

Rights and Permissions

This work is available under the Creative Commons Attribution 3.0 IGO license (CC BY 3.0 IGO) http://creativecommons.org/licenses/by/3.0/igo. Under the Creative Commons Attribution license, you are free to copy, distribute, transmit, and adapt this work, including for commercial purposes, under the following conditions:

Attribution—Please cite the work as follows: Fietz, Katharina, Clement Joubert, Hugo Ñopo, Alberto J. Ocampo, Truman Packard, Josefina Posadas, and Lourdes Rodriguez Chamussy. 2025. (In)Formalizing Jobs in Latin America and the Caribbean: Taxes, Benefits, and Labor Market Incentives. International Development in Focus. Washington, DC: World Bank. doi:10.1596/978-1-4648-2238-4. License: Creative Commons Attribution CC BY 3.0 IGO

Translations—If you create a translation of this work, please add the following disclaimer along with the attribution: This translation was not created by The World Bank and should not be considered an official World Bank translation. The World Bank shall not be liable for any content or error in this translation

Adaptations—If you create an adaptation of this work, please add the following disclaimer along with the attribution: This is an adaptation of an original work by The World Bank. Views and opinions expressed in the adaptation are the sole responsibility of the author or authors of the adaptation and are not endorsed by The World Bank.

Third-party content—The World Bank does not necessarily own each component of the content contained within the work. The World Bank, therefore, does not warrant that the use of any thirdparty-owned individual component or part contained in the work will not infringe on the rights of those third parties. The risk of claims resulting from such infringement rests solely with you. If you wish to re-use a component of the work, it is your responsibility to determine whether permission is needed for that re-use and to obtain permission from the copyright owner. Examples of components can include, but are not limited to, tables, figures, or images.

All queries on rights and licenses should be addressed to World Bank Publications, The World Bank, 1818 H Street NW, Washington, DC 20433, USA; e-mail: pubrights@worldbank.org

Dimension 2: Changes in workers’ perceived value of complying and participating 118

What do changes in incentives mean for employment outcomes? 137

Notes 140

References 141

CHAPTER 7 Good Governance, Perceived Value, and Tax Morale 145

More than the tax wedge? 145

Institutional credibility and trust: Key aspects of reducing the “wedge” 147

Simulating the value of participation: Contributors’ “social security wealth” 149

The puzzle of compliance 154

Institutional credibility: The key to building and maintaining tax morale 156

How important is tax morale? Cross-country correlation analysis 157

Principles and practices to improve tax morale 161

Notes 161

References 162

CHAPTER 8 A Reform Roadmap: Guiding Principles, Objectives, and Milestones on the Path to Improved Incentives 165

Not a blueprint, but a roadmap 165

Five guiding principles for designing and navigating a reform roadmap 166

Three intermediate policy objectives and steps along the road to greater compliance and participation 172

Reforms of social insurance that have improved incentives 180

The politics and persistence of payroll taxes 182

The crisis not yet averted: Consequences of inaction 184

References 191

CHAPTER ANNEXES

Annex 2A Informality in 2019 197

Annex 3A Framework for Self-Employed Workers 205

Annex 3B Enforcement Index 207

Annex 4A Mapping Methodology for the De Jure Tax and Benefit Modeling 209

Annex 4B De Jure Mapping Tables 215

Annex 4C De Jure Analysis Figures 233

Annex 5A Steps to Calculate the Formalization Tax Rate 241

Annex 6A Results of the Simulation Exercises 243

Boxes

1.1 Selection and design of the Latin American and Caribbean country case studies 6

4.1 Differing costs of Brazil’s multiple options for legal employment 74

5.1 Strengths and shortcomings of the formalization tax rate 91

5.2 Implementing the formalization tax rate using micro survey data 94

5.3 A simple static bargaining model of worker registration 97

5.4 Gender dimension of labor supply decisions, taxes, and benefits 103

6.1 Workers’ response to changes in the formalization tax rate: A review of the evidence 108

6.2 Impact of tax and social protection reforms on (dis)incentives to formalize work in Colombia 138

8.1 Policy recommendations from a social protection white paper on risk sharing 169

8.2 The untapped potential of data and digital technology for better governance 176

8.3 Applications of AI in social protection and social insurance administration 178

Figures

2.1 Share of people working informally and income per capita, 1955–2023 20

2.2 Average share of people working informally, by size of the informal economy in LAC countries, 1993–2019 22

2.3 Informal work: Focus and scope of this report 23

2.4 Distribution of workers in select LAC countries, by informality category, 2022 25

2.5 Profile of workers in select LAC countries, by (in)formality category and job characteristics, 2022 26

2.6 Distribution of workers in select LAC countries, by informality category and per capita household income decile, 2022 34

2.7

Share of total labor income in select LAC countries, by informality category and per capita household income decile, 2022 36

2.8 Income distribution in select LAC countries, by informality category, 2022 37

2.9

Average labor income in select LAC countries, by informality category and per capita household income decile, 2022 39

3.1 Three factors that influence negotiations for formalization 50

3.2 Normalized indexes of labor market regulations in select LAC countries, 2019 53

3.3 Likelihood of observing compliance with labor laws and regulations and participation in voluntary insurance schemes 62

4.1 Total augmented tax wedge in select LAC countries, 2013–23 70

B4.1.1 Tax wedge at 1 minimum wage in Brazil, by type of employment 75

4.2 De jure tax wedges at 1 minimum wage: single-earner households in select LAC countries 80

4.3 De jure tax wedges at 1 minimum wage: households with two adults and two children in select LAC countries 82

4.4 Tax wedge under the full valuation and no valuation assumptions 85

B5.2.1 Steps in the implementation of the FTR 95

5.1 Distribution of formalization incentives, by country and employment status, 2019 99

5.2 Formalization incentives, by level of earnings, country, and employment status, 2019 100

5.3 Decomposition of formalization disincentives into social security contributions, income taxes, and transfers, by country, 2019 102

B5.4.1 Correlations between formalization disincentives and gender, age, education, and urban residence 104

5.4 Impact of benefit valuation on formalization incentives 105

6.1 Effects on the FTR due to a statutory increase in the minimum wage in Mexico, by worker type, 2018 115

6.2 Effects on the FTR due to statutory increases in the minimum wage in Colombia, by worker type, 2019 116

6.3 Changes in the FTR due to the real increase in the minimum wage in Colombia, 2019–24 117

6.4 Elimination of payroll taxes and changes in the FTR in Brazil, 2019 120

6.5 Changes in child care contributions and in the FTR in Mexico, 2018 121

6.6 “Universalizing” access to health coverage through reductions in statutory contributions for health in Mexico, 2018 122

6.7 FTR simulations of reduced contributions for the CCF in Colombia, 2019 124

6.8 Changes in the FTR under the proposed changes in contributions for the CCF in Colombia, 2019 125

6.9 Changes in the FTR with the introduction of an unemployment subsidy for independent workers in Uruguay, 2021 127

6.10 Lowering the minimum statutory contribution base in Colombia, 2019 128

6.11 Changes in the FTR under a lower minimum statutory contribution base in Colombia, 2019 129

6.12 FTR simulations of changes in health insurance in El Salvador, 2019 130

6.13 FTR simulations of changes in contributions in Peru, 2019 131

6.14 Distribution of the FTR in Brazil, 2019 134

6.15 Changes in the FTR with the elimination of the formal income cap in Uruguay, 2021 136

6.16 Results from the simulation of increasing the Bolsa Familia benefit in Brazil, 2019 137

7.1 Estimates of the augmented de jure tax wedge in LAC and OECD countries, 2019 and 2023 146

7.2 Observed contribution density: Portion of working life making contributions to social insurance 150

7.3 Estimates of social security wealth from social insurance pension plans in Argentina, Mexico, Peru, and Uruguay 153

7.4 Marginal correlations of the share of people working informally and income, tax morale, employment protection, minimum wages, and total payroll taxes in Argentina 160

B8.1.1 Optimal risk sharing in a national social protection system 170

8.1 Changes in the level of the statutory minimum wage relative to the median wage, select LAC countries, 1990–2022 175

8.2 Social spending and the dependent population in LAC countries, 2020 185

8.3 LAC countries have had far less time to contain fiscal costs than European countries have had, 1950–2100 186

8.4 Given the rising costs of aging, what does social insurance aim to achieve in LAC countries? 189

8.5 Households’ out-of-pocket payments for health and education in LAC countries, 2023 190

2A.1 Distribution of workers in select LAC countries, by informality category and country, circa 2019 198

2A.2 Formality rate among complying and participating workers in select LAC countries, by (in)formality category and per capita household income decile, circa 2019 201

2A.3 Share of total labor income in select LAC countries, by (in)formality category and per capita household income decile, circa 2019 202

2A.4 Distribution of labor income in select LAC countries, by (in)formality category, circa 2019 203

2A.5 Average labor income in select LAC countries, by (in)formality category and per capita household income decile, circa 2019 204

3A.1 Framework for the incentives for the self-employed to formalize 205

4C.1 Total taxes and contributions paid by workers and firms: Single-earner households in select LAC countries 233

4C.2 Pure tax wedge paid by workers and firms as a share of total labor cost, one-adult, single-earner households in select LAC countries 235

4C.3 De jure tax wedge for different types of contracts or work in select LAC countries 237

4C.4 Distribution of workers in select LAC countries, by type of employment 239

6A.1 Dimension 1: Policies affecting labor market competitiveness: increase in the minimum wage 244

2.1 Profile of workers in select LAC countries, by informality category and individuals’ characteristics, 2022 33

4.1 Categories and components of total labor costs 72

6.1 Select reform measures analyzed for their impact on the FTR 111

6.2 Proposed social security reform in Peru 131

6.3 Bolsa Familia rules in Brazil, 2019 and 2024 133

7.1 Pension plans for Argentina, Mexico, Peru, and Uruguay 152

7.2 Country-level variables used in the multivariate correlation analysis 158

7.3 Share of people working informally: Cross-country, multivariate correlation analysis 159

2A.1 Profile of workers in select LAC countries, by (in)formality category and job characteristics, circa 2019 199

2A.2 Profile of workers in select LAC countries, by (in)formality category and individuals’ characteristics, circa 2019 200

3B.1 Enforcement index: Average of the normalized variables, medium total penalty, number of inspectors, and trust in courts 208

4A.1 Overview of tax, contribution, and benefit classifications 210

4A.2 Overview of tax and benefit indicators 211

4A.3 Detailed explanation of the categories in table 4A.2 211

4B.1 De jure mapping for dependent workers in Brazil 215

4B.2 De jure mapping for independent workers in Brazil 217

4B.3 De jure mapping for dependent workers in Colombia 218

4B.4 De jure mapping for independent workers in Colombia 219

4B.5 De jure mapping for dependent workers in Jamaica 220

4B.6 De jure mapping for independent workers in Jamaica 221

4B.7 De jure mapping for dependent workers in Mexico 223

4B.8 De jure mapping for independent workers in Mexico 224

4B.9 De jure mapping for dependent workers in Peru 226

4B.10 De jure mapping for independent workers in Peru 227

4B.11 De jure mapping for dependent workers in El Salvador 228

4B.12 De jure mapping for independent workers in El Salvador 229

4B.13 De jure mapping for dependent workers in Uruguay 230

4B.14 De jure mapping for independent workers in Uruguay 232

Acknowledgments

This report is the culmination of a two-year analytical project conducted by the World Bank’s Poverty and Equity and Social Protection and Labor teams for Latin America and the Caribbean under the leadership of Willam maloney, Jaime Saavedra, Oscar Calvo-Gonzalez, Carlos Rodriguez Castelan, and William Wiseman. The authors are grateful for their support, guidance, and patience throughout the production of this report.

From the beginning, the authors sought to ensure the relevance of the project by keeping World Bank staff who work at the front lines of policy dialogue in the lead of the seven country case studies on which this report is based. The authors recognize and thank the following colleagues for their professionalism, painstaking work, and excellent contributions: Gonzalo Aguilar, Ignacio Apella, Clemente Avila, Gaston Blanco, Ana Lucia Cardenas, Luis Castellanos, Teodoro Crisologo, maria Davalos, Elisa Failache, Samuel Freije, Alexandra Gordina, Sofia Hidalgo Berrios, Roy Katayama, Gabriel Lara, mattia makovec, Fernando marin, Juan manuel monroy, Claudio montenegro, Gonzalo Rivera, Eliana Rubiano, Kajetan Wladyslaw Trzcinski, Diego Tuzman, and Gonzalo zunino. The contributions of these colleagues increase the likelihood that the recommendations made in this report will be closely considered.

The authors are additionally grateful for the excellent data management and research assistance provided by Sofia Hidalgo Berrios throughout the analysis and report writing. Her sense of urgency, tireless attention to detail, and persistence was vital in preparing the reproducible research package for this report.

Finally, the authors are indebted to Santiago Levy Algazi for hours of dialogue and advice throughout the course of the project, as well as to World Bank colleagues who read early drafts and provided excellent suggestions that have greatly strengthened this report. We thank melis Guven, Gabriela Inchauste Comboni, marcela melendez Arjona, matteo morgandi, Ana maria Oviedo Silva, Gonzalo Reyes Hartley, Iamele Rigolini, Ernesto Schargrodsky, Liliana Do

Couto Sousa, and Ekatarina Vostroknutova. Special thanks goes to Sebastian Nieto Parra for serving as external peer reviewer of the report.

We are grateful for the support of a highly professional editing and production team. Cindy Fisher was the acquisitions editor, Christina Davis was the production editor, Sandra Gain was the copy editor, and Greg Edmondson was the proofreader for this book. Lily Franchini provided excellent administrative support throughout.

About the Contributors

Katharina Fietz is an economist consultant at the World Bank, specializing in social protection and labor market policies in Latin America. She also is a research fellow at the German Institute for Global and Area Studies, focusing on informality, tax-benefit systems, and the design and evaluation of employment and social assistance programs. She holds a PhD in economics from the University of Göttingen in Germany.

Clement Joubert is a research economist in the World Bank’s Development Research Group. An applied microeconomist, he is interested in how households work and save in high-informality settings, the economic risks they face, and how to optimally design social protection programs for them. His research also covers gender inequality, underemployment, and radicalization. Before joining the World Bank, he was an assistant professor at the University of North Carolina at Chapel Hill. His research has been published in the Journal of Econometrics, the Review of Economics and Statistics, and the International Economics Review. He holds a PhD in economics from the University of Pennsylvania.

Hugo Ñopo is a senior economist in the Poverty and Equity Practice of the World Bank. He previously served as regional economist at the International Labor Organization and as lead education economist at the Inter-American Development Bank. He also has been a senior researcher at the Group for the Analysis of Development in his native Peru and an assistant professor at Middlebury College in Vermont. He has published extensively on a variety of topics in academic journals and books and, more recently, has participated in outreach and dissemination through opinion columns and TED talks. Currently, he is a research affiliate at the Institute for the Study of Labor in Bonn, Germany. He holds a PhD in economics from Northwestern University in Evanston, Illinois.

Alberto J. Ocampo is an economist consultant at the World Bank, working on labor markets, social protection, and gender inequality in Latin America. He has conducted research with academic and policy institutions on labor economics, health economics, social welfare, migration, and economic development. As a lecturer, he has taught microeconomics and game theory at Universidad del Rosario and Universidad Jorge Tadeo Lozano, both in Colombia. He holds an mSc in economics from Universidad del Rosario.

Truman Packard is a lead economist in the Social Protection and Labor Practice of the World Bank. His last operational assignment was as human development practice leader for Colombia, mexico, and the República Bolivariana de Venezuela. He was lead author of the Social Protection and Labor white paper “Protecting All: Risk Sharing for a Diverse and Diversifying World of Work” and led the team for the report “East Asia Pacific at Work: Employment, Enterprise, and Well-being.” He also led the Human Development program in the Pacific Islands, Papua New Guinea, and Timor Leste and has been part of teams delivering financial and knowledge transfer services to governments in the East Asia and Pacific, Europe and Central Asia, and Latin America and the Caribbean regions. Trained as a labor economist, his work has focused primarily on the impact of social insurance, including pensions, unemployment insurance, and health coverage, on household labor supply decisions, saving behavior, and risk preferences. He holds a PhD in economics from the University of Oxford in the United Kingdom.

Josefina Posadas is a lead economist in the Social Protection and Labor Practice of the World Bank, where she works with client countries to develop and implement policies and programs to improve labor market access and success, particularly for vulnerable populations. Her most recent World Bank publications focus on developing advanced labor market information systems. Additional areas of expertise include entrepreneurship, gender equality, social assistance, delivery systems, aging, and poverty. She has provided policy advice to governments in East Asia, Eastern and Central Europe, and Latin America. Before joining the World Bank, she worked at the Inter-American Development Bank and the Universidad Nacional de La Plata in Argentina, as well as for national and local government offices on employment and fiscal federalism matters. She holds a PhD in economics from Boston University in massachusetts.

Lourdes Rodriguez Chamussy is a senior economist in the Poverty and Equity Practice of the World Bank, where she has worked in the Europe and Central Asia and Latin America and the Caribbean (LAC) regional units. Her work focuses on applied microeconomics, labor markets, political economy of development, and gender. She led the Gender Innovation Lab for the LAC region between 2019 and 2021. Before joining the World Bank, she worked at the Inter-American Development Bank, George Washington University, and the

Government of mexico. She has published articles and reports on poverty measurement, gender gaps in the labor market, the poverty impacts of climate shocks, and the distributive effects of government investments. She co-authored the book Cashing in on Education: Women, Childcare and Prosperity in Latin America and the Caribbean. She holds a PhD in agricultural and resource economics from the University of California, Berkeley.

Abbreviations

Abbreviations Acronyms

AFAm–PE Asignaciones Familiares–Plan de Equidad (Family Allowance and Equity Plan) (Uruguay)

AI artificial intelligence

ARG$ Argentine peso

BPC Beneficio de Prestação Continuada (Continuous Cash Benefit) (Brazil)

CCF Cajas de Compensación Familiar (Family Compensation Funds) (Colombia)

CIT corporate income tax

CLT Consolidation of Labor Laws (Brazil)

Col$ Colombian peso

CREE Contribución Empresarial para la Equidad (Business Contribution to Equity) (Colombia)

ECLAC United Nations Economic Commission for Latin America and the Caribbean

FTR formalization tax rate

GDP gross domestic product

HEART Human Employment and Resource Training (Jamaica)

HICs high-income countries

ILO International Labour Organization

ImSS mexican Social Security Institute

INCRA Instituto Nacional de Colonização e Reforma Agrária (National Institute for Colonization and Agrarian Reform) (Brazil)

ISSSTE Institute for Social Security and Services for State Workers in mexico

LAC Latin America and the Caribbean

Lm labor market

Abbreviations Acronyms

mEI Individual micro-Entrepreneur System (Brazil)

mex$ mexican peso

mIS management information system

mW minimum wage

OECD Organisation for Economic Co-operation and Development

OLS ordinary least squares

OOP out of pocket

p.p. percentage point

PAP Second Pillar Pension Benefit

PBU Universal Basic Pension

PCA principal component analysis

PIT personal income tax

PmG Guaranteed minimum Pension

PNC noncontributory pension

PPP purchasing power parity

QoG Quality of Government Institute

R$ Brazilian real

S/. Peruvian sole

SEDLAC Socio-Economic Database for Latin America and the Caribbean

SENATI National Training Service of Industrial Work (Peru)

SI social insurance

SImPLES Simplified Tax Regime (Brazil)

SISBEN System of Identification of Social Program Beneficiaries (Colombia)

SR reference salary

SS social security

SSW social security wealth

SUS Sistema Único de Saúde (Unified Health System) (Brazil)

TA acquisition rate

UmA Unidad de medida y Actualizacion (measurement and Updating Unit) (mexico)

UNESCO United Nations Educational, Scientific and Cultural Organization

Ur$ Uruguayan peso

WDI World Development Indicators

WGI Worldwide Governance Indicators

WHO World Health Organization

WVS World Values Survey

1 Introduction

WHY THIS REPORT NOW?

Designing and administering effective national social protection systems has long been a challenge for policy makers worldwide. For decades, the principal objection to social protection policies was that they encouraged sloth. Today, voters and the governments they put in place are less worried that taxes and social protections unintentionally create poverty traps than that they encourage workers to be static rather than dynamic, or to be averse to risk with new technologies scaling their economic activity (World Bank 2024).

The task of policy makers is to balance the objectives of greater inclusion, equity, and effective risk sharing at a sustainable cost (Guven and Wiseman 2022; Packard et al. 2019). On one side of the scale, governments seek to ensure that all people are protected from impoverishment regardless of their circumstances; can maintain an adequate standard of living; and have opportunities to build, preserve, and renew their human capital. On the other side, it is important to encourage people’s labor market participation, enterprise, and risk taking so that work is as productive as possible and fuels economic growth.

Governments in the Latin America and the Caribbean (LAC) region are particularly challenged to achieve and sustain the right balance. The region has the longest institutional history of social protection outside Europe, featuring deeply rooted institutions that provide opportunities as well as impose constraints on policy makers. As an example, on the one hand, in many countries the network of social insurance offices has grown to reach farther into remote areas than has other public service providers. On the other hand, the administrative procedures and operating systems have been in place so long that they have become politicized and difficult to modernize. Despite the region’s long history of social protection, in many LAC countries, the percentage of working people who are effectively protected from

A reproducibility package is available for this book in the Reproducible Research Repository at https://reproducibility.worldbank.org/catalog/330/

impoverishment and other risks to their well-being via coverage by social insurance plans—typically still the largest segments of social protection systems—has remained stubbornly low. The low share of working people who regularly contribute to social insurance has been a decades-long challenge.

In reaction to this widespread vulnerability, almost all governments in LAC have established so-called noncontributory programs alongside their contributory social insurance plans. Noncontributory programs provide a semblance of risk-pooling entitlements based on residence, citizenship, and need rather than the sector, manner, or place of employment. They are financed from sources of government revenue other than earmarked levies on firms’ payrolls and profits. In contrast, the eligibility conditions and financing structure of the so-called contributory plans grant benefits conditional on a personalized record of contributions and have been left relatively unchanged since their inception in several LAC countries during the interwar period. This has kept the relationship between what people are mandated to contribute and their eventual benefits difficult to understand and value relative to alternative insurance and savings options (Bozio et al. 2024).

All social insurance plans receive some subsidy financed from the government’s general revenues, to which almost all people contribute in one form or another. Therefore, the words contributory and noncontributory are italicized to emphasize that these labels are more cosmetic than categorical. In the era of human rights and given the codification in many of the region’s national constitutions of the rights of all people to health, education, and economic opportunity, the distinction created by social insurance laws between those “with rights” (“derechohabientes”) and others is a relic, albeit one with clear welfare, fiscal, and distributional implications. Yet, even if these distinctions may be arcane and mainly semantic from the perspective of those who design and finance these programs, they matter greatly to working people’s day-to-day choices.

In most countries in the LAC region, many of the shocks covered by contributory benefits are mirrored by coverage from seemingly “free” noncontributory benefits. In some cases, the latter are almost equal in generosity and quality to the former. Although the push to expand protection is well motivated and urgently needed, many scholars believe that it has created strong incentives for people to remain in relatively unproductive, “informal” work where government mandates can be minimally adhered to or avoided altogether but that impose a heavy burden on the productivity gains that sustain growth (Eslava et al. 2023; Levy and Cruces 2021; Perry et al. 2007). Hence, the best efforts of governments in LAC to kick-start growth are hindered by widespread, deeply rooted, and normalized avoidance and evasion of laws, regulations, and taxation (OECD 2024). Although full or even partial compliance can be an economic nonstarter for many workers and firms, in the aggregate, a self-reinforcing culture of noncompliance can trap countries at low- and middle-income levels of development and sustain social exclusion (World Bank 2024).

Whether cash transfer programs disincentivize or boost formal jobs can vary across contexts. Not all research shows that the advent of assistance through cash transfers in LAC has disincentivized formal work. It is important to distinguish between social protection policies and to scrutinize incentives and outcomes that are likely to differ both in character and in their significance across labor markets.

In some settings, the increased cash injections from social assistance transfers stimulate aggregate demand, even leading to a boost in formal employment (Gerard, Naritomi, and Silva 2021). moreover, recent broad and rigorous reviews of the literature conclude that the published empirical evidence on whether social protection encourages or discourages informal work is mixed (Ghorpade, Franco Restrepo, and Castellanos Rodriguez 2024; Orozco Corona and Vélez-Grajales 2024; Torm and Oehme 2024). Results vary across countries, with changes in focus across different programs, profiles of people, and even minor changes in data. These reviews also make the important point that the absence of integrated analyses of social assistance, social security, and taxation weakens the conclusions that can be drawn. It also reduces the set of reform recommendations to guide the design of comprehensive, coherent national social protection systems. This report is a response to the lack of integrated, systemwide analyses of incentives for formal employment.

Without an integrated, systemwide view of the problem, policy makers fail to account for the second-hand effects and individual responses to policies. That the impact on labor market incentives was not given greater consideration by policy makers when noncontributory programs were launched may reflect two aspects of policy making. First, governments felt that the need to extend protection was urgent. Second, governments lacked political strength in the face of powerful stakeholders and seemingly intractable challenges to reforming social insurance and labor institutions, which had proven over the years to be resilient, even during the region’s many episodes of economic and political instability.

Yet, the importance of incentives should not be underplayed. “Hecha la ley, hecha la trampa” (“once the law is made, so is the ‘work-around’”) is a common saying in the region, usually delivered with a wry smile and even some pride in the viveza criolla (cleverness) and ubiquitous jeitinhos (work-arounds of questionable legality). The latter are small, daily instances of strategic gaming to which market participants resort when the proverbial “rules of the game” allow and where gaming is socially acceptable because people perceive that government mandates are unreasonable and entitlements are of little value. Indeed, in societies where government corruption is long standing and even endemic, this gaming may be justified and even considered admirable.

That the share of social protection financed from general revenues has grown so quickly is not the problem. On the contrary, noncontributory programs are a welcome evolution of policy making, which is quickly

making up for the decades-long limitations and exclusions of purely “Bismarckian,” employment-based models through the nominal contributions of the working head of household (Esping-Andersen 1990).1 Equitable, effective, and sustainable social protection systems should include a variety of financing and eligibility requirements, determined principally according to the nature of the specific shocks that they intend to cover, labor market conditions, and governments’ administrative capacities (Packard et al. 2019). The crux of the matter is the harmony in which all contributory and noncontributory programs coexist without generating unintended perverse effects.

most reforms to date have been episodic, opportunistic, incremental, and implemented with little regard for the labor market and the broader existing system of benefits and taxation. This policy-making challenge is the subject of this report. In most LAC countries, further reforms to all branches of the social protection and personal taxation systems are needed so that noncontributory and contributory programs will work coherently and cohesively to achieve more-effective inclusion, redistribution, and risk sharing, while creating stronger incentives for people to take more risks and work more productively. Politically powerful interests stand as an obstacle. However, as pointed out in the 2024 World Development Report, “the handful of countries that have made speedy transitions from middle- to high-income status have done so by disciplining vested interests, building their talent pool, and modernizing policies and institutions” (World Bank 2024). Even if the nature of policy making in pluralistic representative democracies is necessarily episodic, opportunistic, and incremental, policy makers can still benefit greatly from a set of principles and a “roadmap” to keep their efforts moving in the right direction.

STRUCTURE OF THE REPORT

This report examines the incentives that people face as they encounter the opportunities and constraints that social protection policies and institutions create in the labor market. These institutions are cogs in a country’s broader public revenue and expenditure machine, and from the perspective of most market participants, they are inseparable from personal income taxation. Indeed, in many high-income countries, the objectives of social protection are increasingly pursued directly and explicitly through income taxation channels, as the growing preference for earned income tax credits and other so-called “negative income taxes” in many high-income countries attests. Although social insurance specialists are fastidious in distinguishing statutory “social contributions” from other mandated payments, these programs all entail a ration on the consumption of services—either more or less than people would consume if left to their own devices—provided by a single or tightly limited set of providers. This ration gives any mandated participation in a benefit plan— even one that is actuarially fair—an element of taxation, creating incentives for people to avoid and evade.

What makes a mandated payment a “tax” rather than a “contribution” from a working person’s perspective? This report responds to this key question. With the answers provided, the report identifies a course for policy making as well as specific reforms that could have substantial positive effects on people’s incentives to formalize their work.

The report is structured as follows:

• Chapter 2 sets the scope of the report by identifying the aspect of informal work that is of primary interest: the choices that working people make— whether they are working for themselves or for someone else—when government-mandated protections are partially or not fully enforced, leaving room for choice. This dimension is illustrated empirically, with a moregranular and -specific categorization of working people than the usual, simplistic, and increasingly ambiguous “formal” versus “informal” dichotomy. Using representative survey microdata, chapter 2 strives for greater precision, measuring among those who are subject to national mandates the shares that are “compliant” and “noncompliant.” Among those who are legally free to choose whether to contribute to social protection schemes, the chapter distinguishes the “participating” from the “nonparticipating” shares. The chapter analyzes informality in 2019, just prior to the COVID-19 pandemic, and in 2022, showing how little the shares of workers falling into the previously mentioned categories changed, even in the wake of such systemic and deep social and economic upheaval as the pandemic.

• Chapter 3 presents a conceptual framework grounded in microeconomic theory and evidence, which is used to analyze incentives along three dimensions. The three dimensions are (1) the economic context—specifically, the labor market—which is determined in part by government regulations and product market outcomes; (2) the perceived value that working people assign to the protections and entitlements they are awarded for their compliance with and participation in the social protection system; and (3) the likelihood that the government can detect noncompliance and, when it does, the penalties that it exacts. Each dimension of this conceptual framework is discussed and underpinned with detailed references to an already large and growing theoretical and empirical literature, much of which is not coincidentally focused on countries in LAC.

• Chapter 4 presents the results of de jure tax and benefit models drawn from seven country case studies (described in box 1.1). The de jure models detail the composition of income taxes, benefits, social insurance contributions, and other payroll levies at each point of the distribution of labor earnings as mandated by the government. The modeling allows easy visual identification of incentive “pressure points.” For example, the models show where in the earnings distribution a worker may lose eligibility for a social assistance transfer, the level of earnings at which workers are required to contribute to social insurance, the point at which this obligation changes abruptly with a higher contribution rate, or where exemptions to personal income taxation end or the marginal rate of taxation starts to steepen. The de jure modeling is

presented so that readers can consider the perspectives of an employee and an employer, as well as that of a self-employed person. In countries where alternative legal ways of contracting employees or different forms of selfemployment recognized by regulations are available, the de jure modeling captures these differences, showing clear cost and benefit advantages of one form of contracting over others. The modeling is also presented from a household perspective, as many of the taxes and benefits involve the family and not just the individual.

Selection and design of the Latin American and Caribbean country case studies

Seven country case studies were chosen to reflect the diversity of the Latin America and the Caribbean (LAC) region. The seven countries— Brazil, Colombia, El Salvador, Jamaica, mex ico, Peru, and Uruguay—make up slightly more than two-thirds of LAC’s population. All the subregions in LAC are represented in this study.

Although the informal economy in most LAC countries is large, the prevalence of informal work and the form that it takes vary substantially across countries. Such variation is clearly mediated by legislation. Current social protection and tax policies—and their historical evolution—also differ substantially. For example, Brazil and Uruguay represent one extreme with almost no exemptions to the mandates for workers to contribute to social insurance and around one-third of workers not contributing. Colombia, El Salvador, and mex ico show similar distributions: one-third of workers mandated and complying, one-third mandated and noncomplying, and one-third exempt and noncomplying. Peru is an extreme case in which three-fourths of the working population are exempt from contributing and, indeed, noncomplying.

Similarities and differences exist along the income divide. Across all countries, formality is almost inexistent among working people in the lowest deciles of the income distribution, and informality is also present among the richest. The starkest contrasts are between the rates of formal work among those with higher household incomes.

Note: Further details are available in the annexes to chapter 4.

At one extreme, in Brazil, Colombia, and Uruguay, the share of formality among those with the highest incomes is around four-fifths. At the other extreme, in Peru, 1 in 5 workers is obliged to contribute. El Salvador and mex ico are in the middle. Other clear commonalities across countries are that informal jobs are concentrated in the service sectors and small firms. Workers who are not complying with mandates are predominantly men, and those who can choose and are not participating are predominantly women.

With one exception, the analysis of the country case studies focuses on 2019—or the closest prior year—for three important reasons. First, this focus avoids the systemic impact of the COVID-19 pandemic confounding attempts to identify individual and household incentives created by social protection programs. Second, it helps to steer clear of temporary policy responses to the pandemic crisis. Third, it provides a solid baseline and a substantial subsequent period of analysis for future efforts to measure the impacts of reforms on those incentives.

Each country case discusses changes to social protection and labor market policies and programs since 2019. Several of these changes form part of the analysis, along with ideas for future reform measures. For Uruguay, due to significant changes to the household survey of core relevance, the year of the analysis is 2021.

Box 1.1

• Chapter 5 expands on the traditional analysis of labor market incentives, centered on the tax wedge, by using a renewed definition of the formalization tax rate (FTR). The FTR is a composite measure of the incentives created by social protection and personal income taxation policies, originally conceived by Koettl and Weber (2012) for analysis of incentives to formalize work in Central and Southern European countries (Packard, Koettl, and montenegro 2012). The advantage of using the FTR is that it consolidates assistance transfers, social insurance contributions, mandated in-work benefits, and personal income taxation into a single indicator, calculated for all individuals according to their observed work and personal and household characteristics. The FTR is shown to be a statistically significant and important factor when used in econometric analysis of workers’ observed formal or informal employment. more importantly, it serves as the incentive “benchmark” for comparing the impact of competing or complementary policy reforms.

• Chapter 6 presents an analysis of specific reforms to the personal income tax and benefit policies and how these reforms alter labor market incentives. The reform measures analyzed here are drawn from World Bank policy dialogues since 2019 or have been identified in earlier analysis as important to encourage greater participation in social insurance plans. The chapter discusses the arguments for each reform measure, the share of workers who are likely to be impacted by the measure where they are in the household income distribution, and the extent to which incentives are altered with reductions (and, in some cases, increases) in the FTR.

• Chapter 7 presents a deeper assessment of the factors determining perceived value, specifically how “tax morale” is related to the prevalence of informal work. Given the importance of how mandates are valued by working people to the FTR and their likely impact on labor supply and employment decisions, looking beyond the explicit costs of regulations and mandates is vital. most social insurance plans in LAC present a net subsidy for most participants, although this varies across countries. The level of income at which current plans “subsidize” or “tax” participants also varies across workers according to their accumulated history of contributions (“contribution density”). This chapter compares estimates of the “social security wealth” measure given different levels of observed contribution history, as well as measures of net subsidies and net taxes in four countries. Furthermore, although it may indeed be necessary to minimize structural distortions caused by taxation and social protection policies, that alone is not a sufficient condition to shift economic activity to regulated and taxed markets. The nature of governance, institutional credibility, and social norms of compliance must be factored into the discussion to arrive at truly effective policy solutions that will bring more workers into formal work (Tommasi and Saavedra-Chanduvi 2007). Exploiting data on perceptions of government credibility and analysis of cross-country measures of governance, the chapter examines tax morale and its importance, controlling for labor regulations and other relevant contextual factors.

• Chapter 8 concludes the report with a summary of findings and guidance for policy makers in the region. The report’s most-important message to this audience is as follows. In countries in LAC where national social protection policies have been in place since the early 20th century, the option to start from a proverbial “clean slate” is not available. Nonetheless, population aging, the structural evolution of markets, and the imperative to raise productivity and grow make reforms urgent. many of the incentive problems created by current policies are well known, and more are being identified as talented analysts in the region make increasingly sophisticated use of more and better data. Over the years, as governments have attempted reforms, many features of social protection—especially social insurance—have been fiercely defended by powerful interest groups.2 Few governments have the political space to enact comprehensive reforms all at once, even if they have a well-crafted blueprint for structural changes in hand. As such, politically feasible reforms are likely to be only incremental, partial measures. Pessimists would point out that it was this aspect of tax and social protection policy making that brought about the current incoherence across programs and resulting incentive problems. more optimistically, in a policy-making environment where only incremental, partial reforms are possible, these can have meaningful, positive impact if they are guided by a clear vision of the eventual social protection systems the countries need, and based on sound policy principles and a roadmap to keep the reform efforts on the right course.

KEY STYLIZED FACTS

The existing literature and inference from the country case studies presented in this report led to the identification of several common features of social protection and personal income taxation in the region that are likely to shape incentives against compliance and participation.

Social protection policies still reflect outdated norms around work.

most social protection systems in the region reflect views of the labor market and the nature of work that were adopted from Continental Europe in the 1920s and 1930s. Yet, even at that time, those norms were far from the work experiences of most of the people in LAC countries, which is still the case today (Frolich et al. 2014; Kaplan and Levy 2014; Ribe, Robalino, and Walker 2012). This institutional inertia contrasts with a dynamic, diverse, and still diversifying world of work, leaving entire groups and large numbers of people explicitly or implicitly (statutorily) excluded.

Dependent workers on so-called “nonstandard” contracts, self-employed workers, and many women struggle to fit into the “mold” of the early-20thcentury industrial worker. In the first third of the 20th century, the expectation held by policy makers in Latin America was that most economically active

people would work in subordinated, dependent employment in factories and firms for the long employment spells necessary to meet stringent vesting requirements. The labor market was assumed to be a man’s world; women would dedicate most of their time to home and family responsibilities. Little thought was given to how mandates and incentives would change with more women choosing market work over remaining in their homes.

Only recently have Brazil’s social protection and labor systems been altered to allow less than full-time work. In mexico, affiliation with social insurance requires the place of work to be a business with a fixed location. The Bismarckian, employment-based model of the welfare state in Continental Europe was yet to be tested by shocks to full employment, rising labor turnover, deindustrialization, and demographic change. The model also offered a convenient solution to national governments with limited administrative capacity or power to assess and collect taxes: “delegation” of policy implementation to firms, requiring them to collect contributions on behalf of the state. This further bound effective protection to whether, where, and how people work (Frolich et al. 2014; Kaplan and Levy 2014; Palier 2010). Systemic shocks, sectoral and occupational mobility, production automation, and a large and growing share of people combining market and nonmarket activities, even maintaining a portfolio of concurrent jobs, are all characteristics of today’s world of work that challenge the foundational assumptions on which social protection systems still rest (Packard et al. 2019).

Policies segment the labor market, creating barriers to mobility and challenging the continuity of coverage.

Policies can create barriers to mobility and challenge the continuity of coverage, even for people in mainly formal standard employment. Reflecting the origins of national social insurance plans in the region, segmentation by sector or occupation—taking the form of separate plans or special treatment of certain forms of work—is still common.

For example, in mexico, the mandate to participate in social insurance is constitutionally limited to people in subordinated, dependent employment, but it takes different forms for work in the public and private sectors and even across subnational governments. Brazil is similarly plagued by disparities based on sector, geography, and even occupation. This segmentation can exacerbate the gaps in participation among workers who choose to relocate or find themselves in changed circumstances—whether moving in and out of public employment, switching sectors and geographies, or altering the nature of their economic activity.

Recent efforts to remedy and bridge this segmentation have created additional segments, with special treatment of certain groups, most notably various forms of self-employment and online gig platform workers. Inequities, inconsistencies, and incoherence in how policies and programs are designed to

create ample opportunities for arbitrage, gaming, and outright evasion. many people simply fall out of coverage as life events move them across the cleavages that lie between these segments.

Levies on payroll are intensively used, and indeed abused, for purposes beyond financing social insurance.

Nominally Bismarckian systems, which are designed to tie benefit levels and eligibility tightly to contributions, have been redirected to achieve ambitious redistribution, inclusion, and other social policy objectives for which the original model is poorly suited. The employment relationship—specifically, the earmarked taxation of firms’ payrolls—has become a primary source of finance for interventions designed to redistribute resources to the wider population, including those not or not yet working, and to help resolve social problems unrelated to the workplace or even to the labor market. However, in many instances, this repurposing has led to fiscally regressive outcomes.

As presented painstakingly in this report, nonwage labor costs vary widely, defying simple cross-country comparisons based only on averages. However, the intensity with which governments in the region use payroll taxes for broader social policy conflates the original contributory and “insurance” principles, resulting in levies that bear little relationship to benefits. The de jure mapping from the seven country cases in chapter 4 shows that Jamaica is an extreme case in this regard, with between 5 and 10 percentage points of payroll taxes financing “indirect” programs (although it admittedly has a different social policy tradition than the Continental European model on which other countries’ programs are based).

For example, in Brazil, about 5.8 percent of the levies on payroll finance programs to which workers—in whose name these payments are made—may or may not have a claim. In Colombia, between 4 and 17 percentage points of payroll taxes have a similar character. The explicit and implicit redistribution and cross-subsidization that result make it difficult for contributing workers to accept mandated contributions as deferred remuneration. Population aging and unrevised or even rising expectations of what social insurance should provide make greater fiscal effort an imperative for most LAC governments and raise the costs of poor taxation practices.

Administrative rules, although operationally convenient, create exclusion.

First and foremost among these is the minimum “base” of earned income on which social insurance contributions can be applied, which is typically set equal to the statutory monthly minimum wage for full-time work. A statutory floor on wages can be an effective policy tool to encourage labor supply and improve employment outcomes when it is deployed carefully in monopsonistic and oligopsonistic labor markets. However, when the minimum wage is used as the minimum basis for participation in social insurance, the parameter becomes

a de facto barrier to participation for any person whose capacity to earn falls below the floor. This exclusion is most salient in Colombia.

Few statutory minimum wages in LAC countries are set with strict regard to the level of and changes in median worker productivity. As statutory wage floors are raised relative to the earnings capacity of the median worker, a greater share of working people will be “priced out” of government risk-sharing instruments. Other effectively exclusionary parameters include minimum contribution history requirements to become “vested” for benefits, which are often set with little regard to workers’ likely total spells in formal work, and discrete benefit levels that bear little relation to what most workers can contribute. many such parameters were chosen to make administration, assessment of eligibility, and benefit delivery possible when governments’ capacity was constrained by analog technologies—a constraint that is loosening and could be loosened faster or eliminated altogether with the right investments to augment governments’ administrative capacity.

MAIN MESSAGES FOR POLICY MAKERS

Few policy areas are as notoriously controversial, polarizing, and provocative of popular protest as social protection, labor, and personal income taxation. Interest groups with strong stakes in the status quo are among the best organized, and some are as economically as they are politically powerful. Opposition to wellthought-through and thoroughly appraised reform proposals presented in the past creates curious confederacies that might not otherwise catalyze and that quickly disband when the threat of change subsides.

many changes and additions to social protection and personal income taxation in recent years, although well motivated, introduced or aggravated the inconsistencies in and incoherence of existing policies and programs. This critique may be too easy to make from a technocratic distance. Although specific countries’ contexts and considerations are provided with the presentation of the reform analysis in chapter 6, the report (humbly) suggests that policy makers should keep the following messages in mind. A fuller discussion of these points is provided in chapter 8, which concludes the report.

Job creation and greater productivity are the priority policy means to achieve sustained reductions of poverty and inequality.

This priority entails reforms that move social protection systems in a direction that matches the evolution of the labor market. Income earned through the labor market is consistently found to be the strongest, mosteffective instrument for helping people overcome and stay out of poverty. Governments interested in eradicating poverty should release the labor market mechanism so that it is as unconstrained as possible to create jobs and growth. Yet, as is the case with most markets, the market for labor is rife with failures.

Those issues most germane to this report include the uneven distribution of bargaining power, inadequate information between sellers and buyers of labor, and missing or unaffordable insurance. These market failures are among the foundational motivations for social protection and labor policies, but it is important for policy makers to remember that these are intended as remedial to improve job quality and help people to manage risks rather than as ends in themselves. As such, they would ideally be dynamic and evolve as the communities, societies, economies, and nature of risks in the world of work evolve.

A neutral, agnostic policy stance with respect to how people earn their living is paramount.

Borrowed from the taxation principle of avoiding favorable treatment of income from one source over another, “neutrality” should also apply to how mandates on market work are designed and deployed. Although it remains a matter of debate, the rationale for having a mandate to guide people’s savings and insurance choices is widely accepted. It is not easy to defend the notion that this rationale no longer applies if a person moves from one form of work to another. It is difficult to argue that individuals somehow overcome myopia and other cognitive limitations when they move from a subordinated, dependent form of employment to working for themselves.

If a mandate to save and insure is legitimate, it should be so for all people. Similarly, the arguments for fetishizing certain sectors or ways of working over others, with special tax treatment and exemptions, are growing stale, as work in service sectors grows to be as productive as or more productive than manufacturing jobs (Nayyar and Cruz 2018; Nayyar and Davies 2023). Overnight elimination of the special regimes that have opened the doors of social security to many self-employed workers—like the special social insurance system for self-employed persons registered as small contributors (monotributo) in Uruguay or the Simplified Tax Regime (SImPLES) and Individual microEntrepreneur (mEI) registration option in Brazil—would be rash.

However, ensuring that the application of mandates and taxes is consistent across the ways people work would eliminate incentives to avoid and evade. A careful analysis of special regimes and reforms that would ensure proportionality—steps toward consistency and eventual convergence—could eliminate incentives for strategic gaming, which today often takes the form of firms and workers disguising their employment as self-employment, outsourcing, and subcontracting.

Program financing should be steered toward best taxation practices.

Although the debate over earmarking taxes is ongoing, sufficient consensus exists for aspects that are core to social protection financing. Namely, the use of statutory, individualized payroll taxes should be reserved for programs that cover risks and losses influenced by the parties to employment contracts and

the nature of the workplace, such as the risk of work injury and termination of employment. These losses typically have few or no externalities, for which coverage entitlements and benefits are fully owned by the contributing individuals and their dependents. Inclusion and redistribution—poverty alleviation and prevention, the welfare of historically disenfranchised groups, and income redistribution—are laudable policy objectives but also are better pursued with financing from general revenues. This is the rationale for the restructuring of social insurance financing proposed by Palacios and Robalino (2020), albeit for a far-lower target pension benefit than those promised by social insurance plans in LAC.

If a program is important for social welfare—vis-à-vis the social consequences for society of someone going without it are dire—why make its financing reliant on the good behavior of employers and workers? Reserving the use of payroll taxes strictly for individual coverage and entitlements would dramatically lower the perceived tax element of mandates to save and insure (Palacios and Robalino 2020). In doing so, it would increase the value that working people place on participating and the benefits that flow from contributions.

With a few exceptions, the policies and programs for which a new financing model would be required if governments followed this advice can serve important ends. As a regional study, it is not within the scope of this report to present specific proposals for how they should be financed in lieu of payroll taxes, although some World Bank reports have presented the broad principles that can guide structural reforms (Packard et al. 2019; Ribe, Robalino, and Walker 2012). Rather, the analysis discussed here adds to the growing number of arguments for governments in LAC to broaden their tax bases and pursue a more-balanced deployment of revenue instruments (for example, refer to Vuletin 2024).

Administrative and enforcement capacity needs to be modernized, strengthened, and sustained.

The dangers of moral hazard and the temptations for people to “free ride” can be minimized with better-designed policies and programs, leveraging opportunities offered by digital technologies. However, moral hazard and free riding are human reactions to the availability of risk-pooling and other collective actions and, as such, cannot be eliminated entirely. mitigating behavioral risks requires substantial investment in governments’ monitoring and enforcement capacities, making full use of digital technologies and the growing predictive power of machine learning (zaber, Casu, and Brodersohn 2024).

These investments can also bring the transaction costs of compliance to morereasonable levels. The increasing focus on improvements in service delivery is a step in the right direction. Some of the region’s innovations in the delivery of social assistance provide the best examples of the path to follow—such as

registration and delivery procedures designed around the way people live and work, replacement of proxy measures with systems that observe actual income, and interoperability of administrative datasets to lighten the burden of identification and validation on households. By modernizing administrative capacity, outdated design features that create disincentives to registration and participation can be eliminated—for example, the assumed earned income base set equal to multiples of the minimum wage and long minimum contribution requirements to become vested for pensions.

Trust in policy promises and the credibility of government to follow through is the most-important factor and can be rebuilt.

Governments in LAC have been providing social protection directly or through para-governmental institutions for a sufficiently long period to have wellknown track records. Somewhat paradoxically, although these institutions have stood the test of time and are among the strongest in LAC countries, whether due to inflation, administrative incompetence, or outright corruption, many are viewed with distrust and cynicism. This view has led to erosion of the perceived value of registering work and participating fully in social protection and other taxation systems (Perry et al. 2007; Tommasi and Saavedra-Chanduvi 2007).

When a sufficiently large proportion of the population shares these perceptions, it is more difficult for a single worker or firm to choose full or even partial compliance. This issue is a key insight into the nature of compliance: The importance of perceived fairness in tax systems—the psychological and social aspects of taxation—suggests that people are more willing to pay taxes when they believe others are also paying their fair share. The positive message for policy makers is that governments in countries with similar track records—most notably among countries in Southern and Central Europe—have been able to shift these perceptions in a positive direction, raising trust in institutions, tax morale, and compliance with mandates (for example, refer to Packard et al. 2012).

These key messages form the principles that underlie and orient recommendations for reform.

The key messages in this chapter form the principles that underlie and orient the specific reform recommendations made in chapter 8. As those charged with formulating policies are rarely afforded the choice of when and in what circumstances to propose or pass reforms, the chapter proposes a metaphorical “roadmap” and “milestones” to keep governments on track. Thus, if the reform process is inevitably incremental and opportunistic, hopefully this report—and the instruments for policy reform analysis that it develops—can serve as a tool for navigating the region’s economies toward a system of taxation and social protection that delivers inclusion, equity, and risk sharing more effectively and in a way that attracts and facilitates compliance and participation.

NOTES

1. Bismarckian social insurance is a reference to the original mandated model of risk sharing first introduced in the late 19th century by German Chancellor Otto von Bismarck.

2. There have been efforts to create contributory social protection programs that are appealing to individuals working outside registered, dependent employment, with low, irregular incomes, who typically face financial exclusion and pressing liquidity constraints. However, there have been few success stories so far (Banerjee, Duflo, and Sharma 2021; Guven, Jain, and Joubert 2021; Hu and Stewart 2009).

REFERENCES

Banerjee, A., E. Duflo, and G. Sharma. 2021. “Long-Term Effects of the Targeting the Ultra Poor Program.” American Economic Review: Insights 3 (4): 471–86.

Bozio, A., T. Breda, J. Grenet, and A. Guillouzouic. 2024. “Does Tax-Benefit Linkage matter for the Incidence of Payroll Taxes?” PSE Working Papers halshs-02191315, HAL, Paris School of Economics, Paris.

Eslava, m., m meléndez, L. Tenjo, and N. Urdaneta. 2023. “Business Size, Development, and Inequality in Latin America: A Tale of One Tail.” Policy Research Working Paper 10584, World Bank, Washington, DC.

Esping-Andersen, G. 1990. The Three Worlds of Welfare Capitalism. Princeton, NJ: Princeton University Press.

Frolich, m., D. Kaplan, C. Pages, J. Rigolini, and D. Robalino, eds. 2014. Social Insurance, Informality and Labor Markets: How to Protect Workers While Creating Good Jobs Oxford, UK: Oxford University Press.

Gerard, F., J. Naritomi, and J. Silva. 2021. “Cash Transfers and Formal Labor markets: Evidence from Brazil.” Policy Research Working Paper 9778, World Bank, Washington, DC.

Ghorpade, Y., C. Franco Restrepo, and L. Castellanos Rodriguez. 2024. “Social Protection and Labor market Policies for the Informally Employed: A Review of Evidence from Low- and middle-Income Countries.” Social Protection and Jobs Discussion Paper 2403, World Bank, Washington, DC.

Guven, m., H. Jain, and C. Joubert. 2021. Social Protection for the Informal Economy: Operational Lessons for Developing Countries in Africa and Beyond. Washington, DC: World Bank.

Guven, m., and W. Wiseman. 2022. Charting a Course Towards Universal Social Protection: Resilience, Equity, and Opportunity for All. Washington, DC: World Bank. Hu, Y., and F. Stewart. 2009. “Pension Coverage and Informal Sector Workers: International Experiences.” OECD Working Papers on Insurance and Private Pensions No. 31, Organisation for Economic Co-operation and Development, Paris. Kaplan, D., and S. Levy. 2014. “The Evolution of Social Security Systems in Latin America.” In Social Insurance, Informality and Labor Markets, edited by m. Frolich, D. Kaplan, C. Pages, J. Rigolini, and D. Robalino. Oxford, UK: Oxford University Press. Koettl, J., and m. Weber. 2012. “Does Formal Work Pay? The Role of Labor Taxation and Social Benefit Design in the New EU member States.” IzA Discussion Paper No. 6313, Institute of Labor Economics, Bonn, Germany.

Levy, S., and G. Cruces. 2021. “Time for a New Course: An Essay on Social Protection and Growth in Latin America.” UNDP LAC Working Paper No. 24, Background Paper for the UNDP LAC 2021 Regional Human Development Report, United Nations Development Programme, New York.

Nayyar, G., and m. Cruz. 2018. “Developing Countries and Services in the New Industrial Paradigm.” Policy Research Working Paper 8659, World Bank, Washington, DC.

Nayyar, G., and E. Davies. 2023. “Services-Led Growth: Better Prospects after the Pandemic?” Policy Research Working Paper 10382, World Bank, Washington, DC.

OECD (Organisation for Economic Co-operation and Development). 2024. Taxing Wages 2024: Tax and Gender through the Lens of the Second Earner. Paris: OECD. https://doi.org/10.1787/dbcbac85-en.

Orozco Corona, m., and R. Vélez-Grajales. 2024. “Does Social Protection Cause Informality? A Critical Review of the Literature on the Relationship between Social Protection, Formal and Informal Employment.” Women in Informal Employment: Globalizing and Organizing (WIEGO) Working Paper No. 48, WIEGO, manchester, UK.

Packard, T., U. Gentilini, m. Grosh, P. O’Keefe, R. Palacios, D. Robalino, and I. Santos. 2019. Protecting All: Risk Sharing for a Diverse and Diversifying World of Work. Human Development Perspectives. Washington, DC: World Bank. https://openknowledge.worldbank.org/handle/10986/32353

Packard, T., J. Koettl, and C. E. montenegro. 2012. In From the Shadow: Integrating Europe’s Informal Labor. Directions in Development: Human Development. Washington, DC: World Bank. http://hdl.handle.net/10986/9377

Palacios, R., and D. Robalino. 2020. “Integrating Social Insurance and Social Assistance Programs for the Future World of Labor.” IzA Working Paper No. 13258, Institute of Labor Economics, Bonn, Germany.

Palier, B., ed. 2010. A Long Goodbye to Bismarck? The Politics of Welfare Reforms in Continental Europe. Amsterdam: Amsterdam University Press.

Perry, G. E., W. F. maloney, O. S. Arias, P. Fajnzylber, A. D. mason, and J. Saavedra-Chanduvi. 2007. Informality: Exit and Exclusion. Latin American and Caribbean Studies. Washington, DC: World Bank. https://openknowledge .worldbank.org/handle/10986/6730

Ribe, H., D. Robalino, and I. Walker. 2012. From Right to Reality: Incentives, Labor Markets, and the Challenge of Universal Social Protection in Latin America and the Caribbean. Washington, DC: World Bank. https://openknowledge.worldbank.org /handle/10986/6008.

Tommasi, m., and J. Saavedra-Chanduvi. 2007. “Informality, the State and the Social Contract in Latin America: A Preliminary Exploration.” International Labour Review 146 (3–4): 279–309.

Torm, N., and m. Oehme. 2024. “Social Protection and Formalization in Low- and middle-Income Countries: A Scoping Review of the Literature.” World Development 181: 106662.

Vuletin, G. 2024. “Progressive Taxation for Growth in LAC.” Draft Regional Study for the Chief Economist’s Office, Latin America and Caribbean Regional Office, World Bank, Washington, DC.

World Bank. 2024. World Development Report 2024: The Middle-Income Trap. Washington, DC: World Bank.

zaber, m., O. Casu, and E. Brodersohn. 2024. “Artificial Intelligence in Social Security Organizations.” International Social Security Association and United Nations University, Geneva.

2 Focus and Scope of the Report

“INFORMALITY”:

WHAT IS IT, AND WHY SHOULD WE CARE?

Few public policy phenomena are as ambiguously defined and difficult to measure as the “informal sector.” A form of economic activity that first captured the interest of anthropologists and development economists in the early 1970s (Harris and Todaro 1970; Hart 1973), the informal sector became a central focus of policy in the late 1980s and early 1990s, when sufficient data were first available to show that the informal economy was far more than cottage industries, taxi drivers, and children selling candy on street corners (de Soto 1989).

What is the informal economy? It is inherently difficult to observe something that, by its nature, people are trying to hide (Schneider and Enste 2000). Definitions change according to who is asking and what motivates their question. A minister of finance might ask to know where and how many untapped sources of additional tax revenue can be found. A minister of labor or the leader of a trade union might ask to have a better idea of where to concentrate their efforts to ensure that the rights and protections of labor market regulation are upheld. A minister of trade and industry or the head of the local chamber of commerce might ask to know where opportunities to expand sales, ensure fairer competition, and improve productivity might lie. From each perspective, a different definition of the informal economy can be drawn.

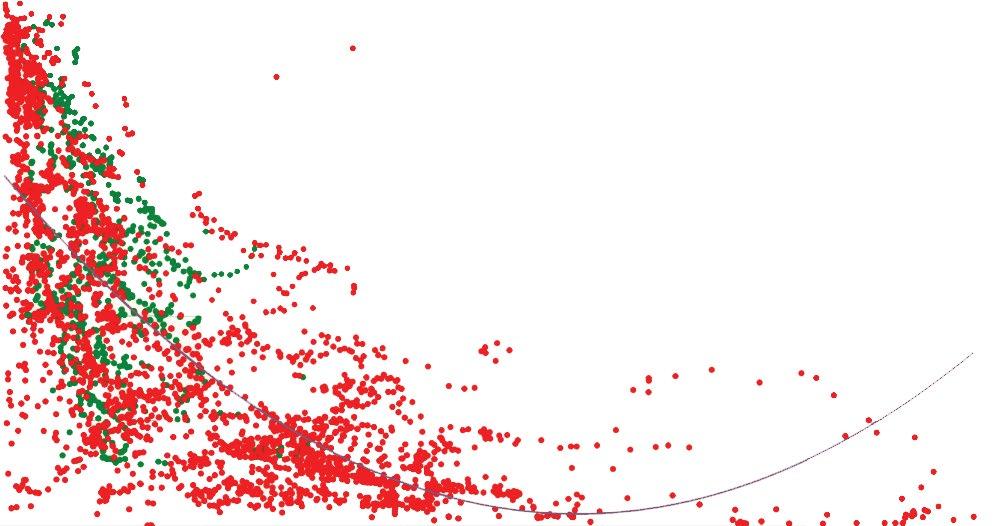

Why should policy makers be concerned about the extent and determinants of the informal economy and informal work? The most-reliable predictor of the size of the informal economy and the share of people working informally is a country’s gross domestic product per capita (refer to figure 2.1). However, just as consistently, the data show that, even at similar levels of per capita income, substantial differences exist in the extent of

A reproducibility package is available for this book in the Reproducible Research Repository at https://reproducibility.worldbank.org/catalog/330/

informal work across countries. What is going on? People work and do business outside the confines of social, labor, and business regulations for many reasons. Some choose to work in the informal economy to escape regulatory costs or enjoy greater flexibility. Others are excluded from the formal economy due to a lack of opportunities for advancement and actual barriers to better-protected, higher-productivity jobs.

Whether people are working informally because they exited or are excluded from formal work, widespread informal employment can be treated as evidence of inadequate and unsustainable social institutions. Thus, the extent of informality reveals the insufficiency of the institutions the state has put in place to help households build, sustain, and protect their investment in human capital as they enter the labor market to seek a return on this investment. Indeed, a large and growing informal economy can be seen as the consequence of a mass opting out of institutions by firms and individuals and “a blunt societal indictment of the quality of the State’s services provision” (Perry et al. 2007, 2).

GDP per capita (constant 2017 international $)

Sources: Original figure for this publication, using calculations based on data from Ohnsorge and Yu 2022; International Labour Organization (ILO.org); the Income Inequality Distribution Database (I2D2), World Bank; the Luxembourg Income Study; and the Organisation for Economic Co-operation and Development.

Note: Observations for countries in Latin America and the Caribbean are in green, covering 21 countries, each with 60–78 observations over 1955–2023. “People working informally as a share of working people” is a composite indicator of people working in firms of 5 or fewer workers, self-employed workers, and nonremunerated family workers. Indicators of informal work from each source are positively correlated, with coefficients of 0.725 to 1.000. GDP = gross domestic product; PPP = purchasing power parity.

FIGURE

The extent of informal work has long concerned policy makers for several reasons:

• First, it is a problem for individuals and their families. People working informally and their dependents face explicit and implicit barriers to public and privately provided insurance instruments to manage potentially impoverishing shocks. Even if people can manage many risks to their wellbeing without help from the state, they may find it difficult to assess accurately the costs of certain needs. These needs may include health care, help during a period of job search, or sufficient provision for losses in the future, such as adequate income arrangements for when they can no longer work in old age. Nor do people who work informally have easy access to credit or recourse to rights and the legal protections these afford when things go wrong. Furthermore, few purely private risk management instruments can withstand a systemic shock. Households that depend solely on the informal economy are far more difficult to reach in the wake of a crisis, such as the recent COVID-19 pandemic.