AN ECONOMIC TUG-OF-WAR BALANCING GROWTH, INFLATION & THE FED

WHAT HAPPENS NEXT? OUR INVESTMENT COMMITTEE’S TOP PREDICTIONS FOR YEAR-END

WHAT EXACTLY IS THE TRUE STATE OF THE U.S. ECONOMY?

IS ARTIFICIAL INTELLIGENCE THE NEW SELF-FEEDING ECOSYSTEM?

JOHN NORRIS Chief Investment Officer

DAVID M C GRATH, CFA Managing Director

A Letter from Our CHIEF INVESTMENT OFFICER

In a lot of ways, the third quarter of 2025 was one of the more boring of my career. With everything happening in the world right now, that might seem like a crazy statement. However, when it comes to investing and dissecting economic data, it was about as plain vanilla as it gets.

Simply put, many investors continued buying stocks while the official economic reports remained somewhat lackluster, mediocre even. The only question anyone had was whether the Federal Reserve would eventually cut the target overnight lending rate.

As we all know by now, it did so at the Federal Open Market Committee (FOMC) meeting on Sept. 17, 2025. Further, it (mostly) left the door open for more rate cuts in the future. Frankly, this wasn’t terribly surprising.

The reasons are simple: official inflation gauges are much lower than they were a couple of years ago, and the U.S. labor market doesn’t appear to be as strong as it was. Yes, inflation is still higher than the Fed’s stated target of 2.0%, and the official unemployment rate was a low 4.3% in August 2025.

However, given where the upper bound of the overnight rate stood at the start of the third quarter, 4.50%, and where the trailing 12-month Consumer Price Index landed in August 2025, 2.9%, the Fed had a little wiggle room to do something if it so desired and thought it prudent.

Apparently, it did. Frankly, after waiting for so long for this cut, it was sort of anticlimactic.

Of arguably greater interest were the continued stories behind gold and artificial intelligence (AI).

The shiny stuff has appreciated significantly throughout 2025. According to Bloomberg Financial, the “Generic 1st Gold Future” closed the third quarter at $3,840.80 an ounce. At the end of 2024, one ounce would have set you back - if that is the right phrase - $2,641.00. Obviously, that is quite a move in a short period of time.

• Is it due to foreign central bank demand? That is certainly some of it.

• Growing mistrust of the global financial system? That could be part of it.

• Increased acceptance of commodities as an asset class for retail investors? There is probably some of that.

• A fear of missing out on a rally (a FOMO trade)? I suspect that is in the mix as well.

Associate Managing Director

The truth is, gold’s recent strength is probably a combination of all of it.

As for AI, it seems the mere mention of it in a business model is enough to get investors frothing at the mouth. While that statement is obviously hyperbolic, after a difficult start to the year, the AI sector has been on a period of strong performance in U.S. stock market. This is true even as investors are beginning to question its ability to upend jobs and entire industries. However, while the ultimate economic upheaval in the future remains to be seen, investors appear to be focusing on growth in the here and now.

All told, while there was a lot happening around the world during the third quarter of 2025, it was still sort of boring in a lot of ways. While, again, that might sound a little crazy, investors will take positive and boring over negative and exciting any day.

Thank you for your continued support.

John Norris Chief Investment Officer

As of September 30, 2025, Oakworth Capital currently advises on approximately $2.52 billion in client assets. The allocation breakdown is in the chart below.

THIRD-QUARTER KEY TAKEAWAYS

The third quarter was marked by resilient equity markets and a long-awaited rate cut, even as dicey labor data and pricey cheeseburgers cast doubt on the health of the U.S. economy. Tariffs pinched profits and investors shifted bets toward AI and crypto.

TECH STOCK VALUATIONS

History suggests U.S. investors have always loved their technology stocks at inflection points in the economy. Most people probably agree artificial intelligence (AI) will change our lives and the way we conduct business. However, Investor’s Business Daily notes that correctly valuing AI stocks and technology remains something of a guessing game.

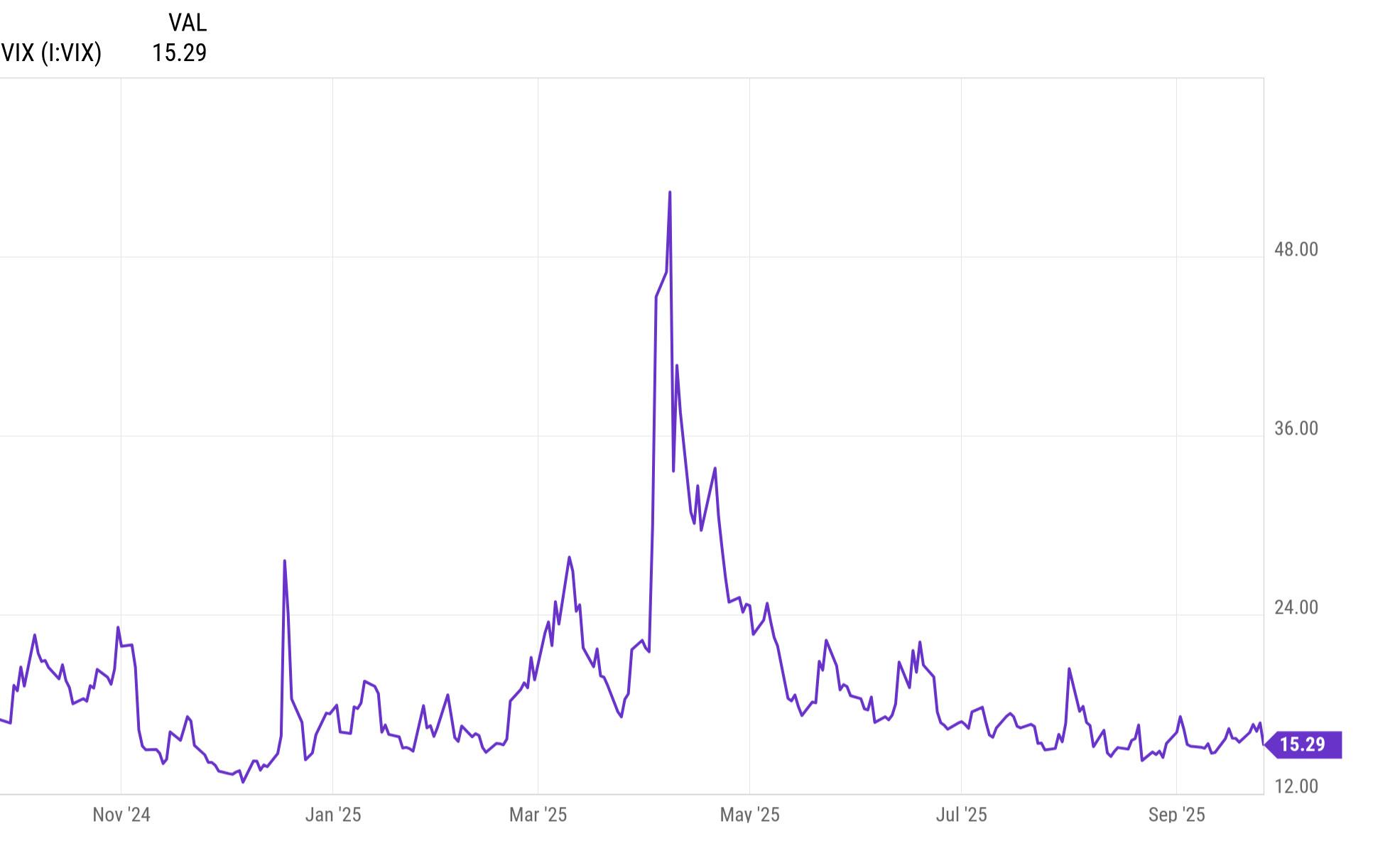

LOW MARKET VOLATILITY

Given today’s geopolitical turmoil and domestic challenges, one might expect the U.S. stock markets would have been livelier than they were during the third quarter of 2025. Instead, the CBOE Volatility Index (VIX) tells a different story: market volatility has been very low, signaling either investor complacency or optimism that the momentum will continue.

OVERSTATED JOBS DATA

After months of almost head-scratching labor market reports, the Bureau of Labor Statistics (BLS) announced it had overstated the number of payroll jobs the economy created between April 2024 and March 2025 by 911,000. This was a historically significant (0.6%) correction, which called into serious question the true health of the U.S. economy.

BEEFED UP GROCERY BILLS

Beef prices have continued to climb, thanks to the lowest domestic cattle herd since at least 1973, as reported by the U.S. Department of Agriculture. While no one likes it, the Consumer Price Index reported a 12.8% increase in ground beef prices over the 12 months ended in August 2025, Americans seem willing to pay the price to get their cheeseburgers. Guilty as charged.

THE GOLD RUSH CONTINUES

There seems to be no shortage of explanations for the recent surge in gold and other precious-metal prices. Foreign buying, U.S. inflation, distrust in global fiat currencies, the potential for a federal government shutdown and Fed rate cuts, among others, have all received the blame. Regardless of the reason, investors have started to wonder whether their jewelry is properly valued for insurance purposes.

CRACKER BARREL CROSSFIRE

Thanks to social media — and the baffling ways some issues go viral while others don’t — corporate rebranding has become a risky proposition. In the third quarter, Cracker Barrel rolled out updates to its logo and image. The backlash, whether real or fabricated, was intense. What are marketing teams to do if “bots” and “provocateurs” can throttle otherwise sound decisions?

THE FED FINALLY CUT RATES

After months of speculating and waiting, the Federal Reserve finally cut the target overnight lending rate at its September 2025 FOMC meeting. Although the official inflation gauges might be higher than the Fed would like, recent weakness in the labor markets apparently has it somewhat concerned.

BUT RATE CUTS DON’T EQUAL

CHEAPER MORTGAGES

U.S. consumers and residential real estate brokers and agents of all stripes are having to relearn that mortgage rates don’t necessarily fall when the Fed cuts the target overnight rate. In fact, they sometimes even go up. The reason for this is simple. The Fed cuts the one-day price of money in the U.S. economy, and mortgages generally have much longer final maturities than that.

LAISSEZ LES BON TEMPS ROULER

Absent a severe outside shock or major downturn in the economy, the third quarter seemed to prove the U.S. stock market’s current path of least resistance is to move higher. While that can and will change over time, U.S. investors appear complacent to let the good times roll in their portfolios for a little while longer.

TARIFFS HIT PROFIT MARGINS

Thus far, it seems U.S. businesses and importers have absorbed much of the cost of the administration’s tariffs, perhaps helping to limit consumer price increases. However, ultimately, companies will likely have to cut costs elsewhere in order to maintain profit margins.

PROFITS FROM ACROSS THE POND

Despite talk of Europe’s increased irrelevance, investors have gobbled up euros, British pounds and other European currencies in 2025. If their issuers were truly irrelevant, would investors really be buying them? Probably not. Still, without reform, the European economy is in danger of falling further behind the U.S. and Asia.

CRYPTO CONTINUES TO CLIMB

Cryptocurrencies enjoyed another nice run during the quarter. Investors seem to favor them when geopolitical turmoil is relatively high and central banks start cutting rates. Easier access through retail products like ETFs may also be fueling demand — perhaps a combination of the two.

STATE OF THE ECONOMY

Contrary to popular belief, the U.S. economy is neither as bad as many believe nor as strong as some would contend — leaving markets caught between mixed signals and the looming possibility of rate cuts.

John Norris

WHAT IS THE TRUE STATE OF THE U.S. ECONOMY?

After all, it seems as though the powers that be seasonally adjust, revise and otherwise massage the data to such an extent, it is nearly impossible for the average American to know what is actually happening.

THE LABOR MARKET

To that end, this past quarter, the Bureau of Labor Statistics (BLS) announced that 911,000 previously reported payroll jobs didn’t actually exist for the period from April 2024 through March 2025. Obviously, that isn’t an insignificant revision. In fact, it is the largest one since at least 2000, coming on the heels of last year’s negative adjustment of 818,000.1

For its part, the Bureau of Economic Analysis (BEA) originally announced U.S. Gross Domestic Product (GDP) grew at an annualized 3.0% rate during the second quarter of 2025.

› Then, it reported it had actually grown 3.1%.

› Finally, just before the end of the third quarter, it announced the economy ultimately grew at a 3.8% annual rate for the previous quarter.

Who knows what the economic growth would be if the BEA just had enough time to keep revising its data? Further, the headline numbers can be a little deceiving even without all of the revisions.

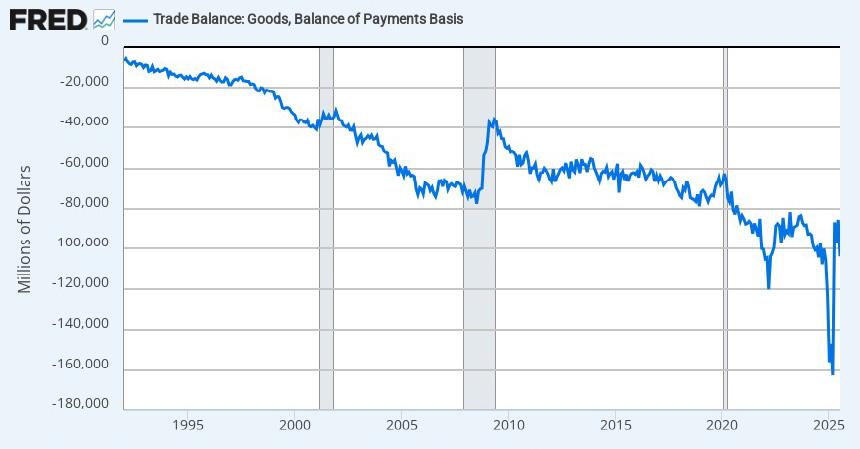

In fact, the BEA now estimates the U.S. economy shrank 0.6% during the first quarter of 2025. However, pretty much all the decline was due to businesses stocking up on their inventories and otherwise front-end loading purchases to stay ahead of the administration’s tariffs. Obviously, this caused our already-bloated trade deficit to balloon.

HISTORIC SWINGS IN THE TRADE DEFICIT IN 2025

*Source: Bloomberg Federal Reserve Bank of St. Louis

GDP AND TRADE

To put that in perspective, the BEA now reports the deterioration in our trade balance during the first quarter took 470 basis points (4.7%) off the overall GDP equation. Of course, a lot of those imports went straight into inventories, which the agency claims added 258 basis points back. Yes, it can be a little confusing.

Now, not surprisingly, the trade deficit improved dramatically during the second quarter as U.S. businesses drew down more inventories instead of buying more from overseas. That shift showed up in the GDP equation, adding 483 basis points (4.8%), while inventory drawdown subtracted 344 basis points (3.4%) to the GDP equation respectively. 2

Put simply, the economy wasn’t really as weak as the BEA reported for the first quarter. Conversely, it wasn’t as strong as it said it was during the second quarter. It is just the way the equation works, and the equation can sometimes be a little messy.

SO, BRASS TACKS, WHAT IS THE TRUE HEALTH OF THE U.S. ECONOMY?

While it is impossible to give a definitive answer — especially since the agencies in charge of calculating such things keep revising their data — the BEA includes something called “final sales to domestic purchasers” in its GDP report. While far from perfect, it’s probably as good a reflection of what the “average American” feels as any.

Right now, by this measure and before any future revisions, the U.S. economy probably grew around 1.4% during the first three months of the year, and about 2.4% last quarter. Again, probably.

Perhaps that helps to explain why the Federal Reserve cut the target overnight lending rate during September, even though the BEA was reporting 3.8% GDP growth. Obviously, that wouldn’t make a lot of sense otherwise.

Further, it wouldn’t make a lot of sense if the BLS hadn’t made such a massive negative revision to the payroll data it had previously reported.

You see, the Fed has a dual mandate: price stability and full employment. Maximum economic growth, interestingly enough, is not a part of that equation.

INFLATION

To that end, anyone who has recently been to the grocery store will tell you inflation is still a problem. If not inflation — the growth rate of price changes — then prices themselves. However, it is far from clear whether tinkering around with the overnight rate will actually have any impact on all of the items in your cart.

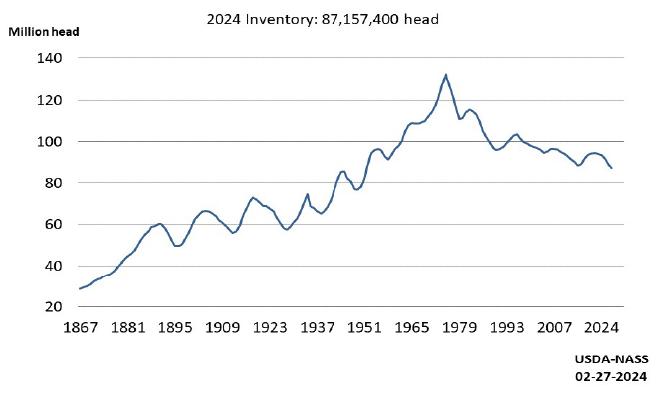

Beef is a perfect example, and the cut doesn’t matter. Ground beef, roasts, steaks and even oxtails are all up sharply in price. Why? Drought conditions in the Midwest drove up the cost of fodder a few years ago, and farmers processed a larger than normal amount, including heifers. Obviously, fewer heifers means fewer calves. Fewer calves mean fewer cows to process. Fewer cows mean higher beef prices. Voilà.

ALL CATTLE AND CALVES INVENTORY -- UNITED STATES: JANUARY 1

I am not sure what the overnight rate has to do with it. In fact, some can argue higher interest rates might actually exacerbate the problem. The U.S. cattle supply is at its lowest level in decades.

THE HOUSING MARKET

Housing faces a strikingly similar challenge. There simply aren’t enough homes available for sale. As a result, prices have increased substantially, which has forced many potential homebuyers into the rental market. Unfortunately, a greater demand for rental units drives rents higher.

Since the “owners’ equivalent rent of primary residence” constitutes roughly 26% of the Consumer Price Index (CPI), there is upside pressure on the official inflation gauges when people can’t afford to buy single-family homes.

Basically, anything that drives down rental demand should put downward pressure on the official inflation gauges.

In essence, changes in monetary policy will have little impact on some items that are currently hitting consumers’ wallets. Further, and admittedly somewhat counterintuitively, higher interest rates

Put another way, higher interest rates generally make housing less affordable. When housing is unaffordable, more people are forced into leasing, which causes rents to go up. This causes the inflation gauges to remain elevated, which forces the Fed to keep the overnight rate higher than anyone would like.3

may be inflationary in certain economic sectors, like housing.

Therefore, some believe the Fed could support U.S. consumers’ purchasing power by actually lowering the overnight rate, making money less expensive in the financial system, thereby reducing financing costs. Go figure.

As for full employment, well, if you have liked the labor markets over the past several quarters, you will probably like them for a little

while longer. Nothing in the crystal ball or tea leaves suggests the U.S. economy is going to come to a screeching halt. As such, there is little to suggest hiring will collapse in the near term.4

However, given the relatively modest economic growth rates we have recently experienced, a sudden surge in new employment is equally unlikely. Essentially, the U.S. economy should be a net creator of new jobs over the next couple of quarters, but the numbers are likely to be underwhelming.

*Source: Federal Reserve Bank of St. Louis

ARTIFICIAL INTELLIGENCE

I would be remiss if I didn’t mention something about artificial intelligence (AI). After all, it has been a — if not the — primary topic in the business world for some time. Will AI wreck the economy or be a blessing for it? Inquiring minds want to know.

The probable-case scenario is that AI will play havoc with individuals while creating massive benefits for the economy as a whole. You see, the people who don’t learn to adapt to and utilize the newest technologies will be at a severe disadvantage in the workforce. They will be the first ones to lose their jobs.5

Intuitively, this set of workers probably doesn’t drive much valueadd or wealth creation in the U.S. economy. Conversely, those that do adapt and use AI effectively will develop new technologies, industries and jobs which don’t currently exist! Frankly, this makes AI far more exciting than terrifying to me.

When people ask me about AI’s potential impact on the U.S. labor markets, I usually tell them there could be some short-term pain for some. However, in the longer term, it may prove to be a massive job creator, and I can’t wait to see what changes it brings us.

SO, WHERE DOES THAT LEAVE US? WHAT IS THE TRUE STATE OF THE ECONOMY? WHAT IS LIKELY TO HAPPEN MOVING FORWARD?

Contrary to popular belief, the U.S. economy is neither as bad as many believe nor as strong as some would contend. However, the potential for error appears to be the downside due to a somewhat softer labor market. As a result, in our view, the market should expect the Federal Reserve to cut the target overnight lending rate at least three more times before this easing cycle is over, though the number and timing remain uncertain.

Hopefully, that will be enough to get things humming again.

SOURCES:

1. The Bureau of Labor Statistics Economic – Current Employment Statistics Preliminary Benchmark Summary (September 2025)

2. The Bureau of Economic Analysis – Second Quarter Gross Domestic Product 2025 by Industry, Corporate Profits and Annual Update (Sept. 25, 2025)

3. The Bureau of Labor Statistics – Consumer Price Index Relative Importance and Weight

4. The Bureau of Labor Statistics – The Employment Situation (August 2025)

Oakworth Asset Management is a registered investment advisor. All advisory services, including investment management and financial planning, are offered through Oakworth Asset Management, LLC. Oakworth Asset Management is owned by Oakworth Capital Bank, member FDIC, Equal Housing Lender.

Investment products and services offered via Oakworth Asset Management, LLC are independent of the products and services offered by Oakworth Capital Bank and are NOT FDIC INSURED, NOT BANK GUARANTEED, and MAY LOSE VALUE.

The information, opinions, comments, statements, views or recommendations expressed are general in nature and should not be considered professional, tax or legal advice; or as an offer to buy or sell or to make or consider any investment or course of action.

SPECIAL REPORT: CIRCULAR FINANCING IN ARTIFICIAL INTELLIGENCE

Many have debated whether AI’s explosive growth really reflects a genuine technological breakthrough that has revolutionized efficiency - or if we are simply watching a self-feeding bubble take shape.

Ryan Bernal

In a gold rush, the miners rarely strike it rich – it’s the companies selling the picks and shovels that do. This is termed “the picks and shovels play” and has been an interesting strategy employed across many different industries. In this dual role, NVIDIA has taken this to a new level — not only acting as the supplier of picks and shovels, but stepping into the miners’ shoes, too. This illustrates how vertical integration can accelerate ecosystem growth. For years now, NVIDIA has been supplying the much-soughtafter semiconductor chips that artificial intelligence (AI) and tech companies demand, growing the company into the largest in the world, with a market cap of $4.55 trillion. But that wasn’t enough – it is now investing directly into the companies that purchase its products and create infrastructure for the growing AI world. This has created a new “self-feeding” ecosystem that is isolated from the broader economy – but is becoming a larger and larger part of it.

It probably won’t come as a surprise when I say we are in the midst of a new gold rush – some have dubbed it the “AI

Revolution.” While AI has been in development for decades, it has only recently exploded into the zeitgeist since the COVID-19 pandemic. One of the largest contributors to this surge in popularity was OpenAI’s release of ChatGPT in late 2022, which revolutionized how people interacted with AI. Its impact was immediate: companies and individuals alike saw its vast potential and raced to harness it.

This led directly to a boom in new AI startups. Some looked to compete directly with OpenAI and its large language models (such as Anthropic), while others tried to create useful applications using OpenAI as their engine. OpenAI’s business model includes selling access to their API, a backend solution to power new applications using its technology. This allowed the startups to leverage new technology without the massive cost and expertise required to develop large language models from scratch. Today, ChatGPTstyle applications are everywhere, from Perplexity.ai, which specializes in deep-dive research, to my personal favorite, FinanceGPT, a finance-focused tool that provides AI-driven

market analysis. But with this explosion of new applications, OpenAI must keep pace with demand — requiring ever more processing power, which translates into more data centers and ultimately, greater reliance on NVIDIA’s all-important chips.

While startups were jockeying for the next round of funding, the largest tech players were gearing up for their own expansion into AI. Industry giants started to pour massive amounts of resources into their AI departments, hoping to increase the efficiency of their existing business model. According to the New York Times, Microsoft has allocated about $80 billion for AI infrastructure and data center spending in the 2025 fiscal year, while Meta has earmarked around $68 billion to build out their AI framework.1 Even search leader Google has entered the AI arms race, unveiling Gemini, its new flagship AI-driven chat tool. To realize these ambitions, companies are offering eye-popping compensation packages to the best AI talent — deals now rivaling the salaries of NBA and NFL stars. 2

Despite the spending craze, it has not all been smooth sailing. Investors have started to question the return on investment

for these huge capital expenditures, challenging businesses to rethink their approach. For NVIDIA, the current answer appears to be partnerships. Over the past six months, the company has announced several high-flying deals, aiming to invest in some of its largest customers. One of the most prominent deals is with OpenAI, which could see NVIDIA invest over $100 billion, an amount tied directly to how many chips OpenAI agrees to purchase and deploy, according to CNBC, Sept. 22, 2025. Another is a $5 billion stake in fellow chipmaker Intel, aimed at co-developing custom data center and PC products. 3 Investors have rewarded this strategy so far, as NVIDIA’s stock sharply increased following these announcements. In some cases, NVIDIA’s market cap increased more than the total amount pledged in the partnership.

And don’t think NVIDIA is only gunning for the top dogs. The largest company in the world has also made significant investments in the AI startup space, taking a 91% stake in cloud AI company CoreWeave, along with other smaller stakes in ARM Holdings, Applied Digital and others. 4

WHO’S POWERING THE AI BOOM: GPU SHIPMENTS BY CUSTOMER

Microsoft’s Spending On NVIDIA’s Ai Chips Has Far Outstripped Rivals’ 2024 Shipments Of NVIDIA Hopper GPUs (‘000) Nvidia’s Hopper Generation Includes H100, H800, H20, H200 | Source: Omdia

These investments from NVIDIA represent a significant boost to the cash reserves for receiving companies. Flush with cash, most companies have opted to, you guessed it, purchase even more chips from NVIDIA. This phenomenon, often referred to as “circular financing,” is a self-reinforcing strategy in which a company invests in its own customers to accelerate their growth. That growth then drives increased demand for the company’s core products, boosting revenues and ultimately delivering a positive return on the original investment.5

An example from history can be found in the late 1990s with Intel. A subsidiary called Intel Capital was founded in 1991; its main purpose was to invest in hardware, networking and other PC startups to accelerate the adoption of personal computers worldwide. The investing arm began subsidizing PC makers that featured Intel chips inside, leading to the famous “Intel Inside” campaign, which can still be seen on computers today. Investors questioned the capital expenditures back then as well, stating that Intel was overspending and inflating the PC boom. This eventually led to an antitrust investigation in the late 1990s and early 2000s, which culminated in a settlement that ordered Intel to change its licensing and marketing practices, eliminating what prosecutors called “hidden rebates” for companies using Intel’s chips. 6 While this wasn’t the end of the story for Intel, many argue it fueled the flames of the irrational exuberance that technology companies saw at the turn of the century.

So — is this good or bad for the overall economy? The jury is still out, but we can examine the pros and cons of the strategy and its possible long-term effects.

One potential benefit that may arise is the co-development of new technologies through these partnerships. Chipmaking and AI programming require extreme expertise, and the hardware and software must work together in perfect harmony. If they are designed to work together from the start, the components may have a better chance of success.

Then there is the financing situation. It requires massive amounts of resources to create and train these large language models such as ChatGPT, and OpenAI itself is not yet profitable. The solution the market has seemingly proposed is to secure funding for this cutting-edge research from one of the largest and most profitable companies in the world, which also happens to understand the environment in which it operates.

On the other hand, there are some inherent risks with this strategy. Although NVIDIA’s stock growth has been nothing short of meteoric, it seems the stock has been priced to perfection. In the investing world, this means investors are assuming near-flawless performance with near-perfect conditions to justify the current price.

Some analysts have begun labeling the AI boom a potential bubble , pointing to the recycling of NVIDIA’s cash through its customer acquisitions and partnerships as evidence. 7 Another potential downside comes from Intel’s history lesson. Their strategy was foiled by litigation, specifically antitrust concerns. Being on the losing end of such cases has often led prosecutors to seek breakups of these corporations, which would almost certainly reduce NVIDIA’s business moat in the AI space, which could spell the end of its dominance.

If the company experiences any significant hiccups, the house of cards could come crumbling down.

As the effects of this new-age gold rush continue to be seen, one thing is clear: AI and its ecosystem have come to dominate domestic markets in a way that few other industries have before. The technology sector now represents more than a quarter of the total S&P 500 weighting, with NVIDIA alone accounting for a staggering 8% of the total weight.

This raises an interesting question: Is this explosive growth really driven by a technological breakthrough that has revolutionized efficiency? Or is it simply a self-feeding

SOURCES

investment loop that has created artificial value? If these companies are correct in their bet on AI — which they have signaled with their dollars — If these companies are correct — and if their projected efficiencies are realized — current valuations could prove reasonable. However, if profitability expectations fall short, broad market valuations may adjust. Much like in the dot-com bubble, there is often a fine line between revolutionary technology and speculative market euphoria. 1. Investing.com – “NVIDIA Stock Up as Meta Boosts AI Capex, Microsoft Datacenter Demand Not Slowing “(April 2025)

(Sept. 19, 2025)

4. HedgeFollow – “Top 50 NVIDIA Corp Holdings”

5. The National Bureau of Economic Research – “The Determinants of Corporate Venture Capital Success”

6. The Federal Trade Commission – “Intel Corporation, In the Matter of 1999”

7. Yahoo Finance – “NVIDIA’s $100 billion OpenAI Investment Raises Eyebrows and a Key Question: How much of the AI Boom is Just NVIDIA’s Cash Being Recycled?”

This material is provided for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. The opinions and information contained herein are based on sources believed to be reliable, but their accuracy and completeness cannot be guaranteed. References to specific securities or companies are for illustrative purposes only and do not constitute an offer, solicitation, or recommendation for any particular investment strategy. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal.

THIRD-QUARTER EQUITIES

The fourth quarter of 2025 could be a very interesting quarter for the stock market. The labor market has fallen into a “Goldilocks” zone — cool enough for Fed rate cuts, but not so cold to have yet caused a broader decline in corporate earnings.

The question is…will it last?

David McGrath, CFA®

The Fed

The labor market showed enough weakness in the third quarter, alongside stable inflation numbers, for the Federal Reserve to reduce interest rates by 25 basis points in September, with the possibility of even more cuts in late October and mid-December.

Historically, small-cap stocks perform well during Fed rate-cut cycles, and the third quarter this year was no different. The S&P SmallCap 600 returned 8.7% — above the S&P 500 — trailing only the Nasdaq composite.1

AI and the Magnificent Seven

While the Fed had an influence on the equity markets last quarter, the Magnificent Seven and the AI trend remained significant drivers of stock returns. The stocks with the largest impact on the S&P 500’s strong quarterly return include Apple (+26.7%), NVIDIA (+15.3%), Google (+36.8%) and Tesla (+37.0%), all cardcarrying members of the Magnificent Seven. Other technology stocks, including Oracle (+34.8%) and Broadcom (+22.0%), also added to the S&P 500’s move higher.

Those same large-growth companies that dominate the S&P 500 make up an even larger percentage of the Nasdaq, which led all index returns in the third quarter with an 8.8% return.

All three economic sectors that include members of the Magnificent Seven — technology (+11.3%), consumer discretionary (+10.3%) and communication services (+9.1%) — were the three best-performing sectors of the quarter. The defensive sectors were among the worst performing. Consumer staples fell 3% while healthcare gained a modest 1.5%.

The exception among defensive sectors was utilities, posting a return of 6.8% in the third quarter (see chart below)1. This positive

return may have been influenced by ongoing AI infrastructure buildout. If AI infrastructure continues to expand at the current rate, the current electric grid will likely face significantly increased demand. Economics 101 tells us that in most cases when a product’s demand is growing faster than the supply, prices tend to rise. This may bode well for electric-utility sector fundamentals.

After significantly outperforming domestic stocks in the first quarter, and keeping pace in the second quarter, international stocks struggled in the third quarter. Over the last three months, the largest international stock index, the MSCI EAFE index, gained 3.5% — a lower return than any domestic stock index.

Source: Bloomberg Financial

As we entered the third quarter,

As we entered the third quarter, there were three main questions that, in our opinion, could influence whether stocks could continue their climb higher.

• Would the Federal Reserve cut the federal funds rate?

• Could the elevated pace of spending on artificial intelligence (AI) infrastructure continue?

• Would corporate earnings season remain strong in the face of new tariffs?

The quick answer to all three questions appears to be a resounding yes.

There were some questions as we entered second-quarter earnings season. With new tariffs being implemented, would corporations pass the increase in costs along to the consumer? Would that lead to a downturn in spending? Or would companies absorb the tariffs, leading to lower profit margins?

In the end, both profit margins and consumer spending held firm, resulting in a strong second-quarter earnings season, led once again by the Magnificent Seven. Those companies posted year-over-year earnings growth of 26.6%; the other 493 members of the S&P 500 showed earnings growth of 8.1%. Looking ahead to the next few quarters, analysts are expecting earnings growth rate for the Magnificent Seven to fall to 14.5%. 2 Earnings Season

S&P 500 EARNING AND EXPECTED GROWTH (Y/Y): MAGNIFICENT SEVEN VS THE OTHER 493

Source: FactSet

One unexpected shift in the third quarter was the drop in market volatility. I am not sure we can attribute that to a lack of news headlines over the past three months, as the first two quarters of the year were extremely volatile for stocks. During the first and second quarters of 2025, the S&P 500 saw 40 trading days with a price change (both positive and negative) of greater than 1%. Third quarter only gave us four of those volatile days. Is it possible that investors are becoming numb to the news cycle and simply look past the daily headlines?

It was a “drift higher” quarter for the stock market. This has left stocks trading at elevated valuation levels. As we have mentioned before, valuations are historically not a great predictor of stock returns, but experience shows that it does increase the potential downside risk. Both growth stocks (28.5 times earnings) and value stocks (18.4 times earnings) are trading near recent highs.3

FORWARD P/E RATIOS FOR S&P 500 GROWTH AND VALUE (WEEKLY)

Looking Forward

The fourth quarter of 2025 could be a very interesting quarter for the stock market. The labor market has fallen into a “Goldilocks” zone for equities; cool enough to allow the Fed to cut interest rates, but not so cold that we have seen a decline in corporate earnings. The question is … will it stay there?

Roughly two-thirds of all spending in this economy is driven by consumers, and people tend to spend less when they are fearful of losing their job. We seem to be on the tail end of the strongest labor market in decades, and most workers have felt very confident in their job security. They have spent accordingly.

Hiring seems to have slowed to a near halt, but we have not gotten to the point of significant layoffs. If weakness in the labor markets continues and the unemployment rate starts to move higher in the next few quarters, corporate earnings could take a hit. In the short term, stock prices may be vulnerable due to a combination of heightened valuations and potential earnings cuts.

The silver lining of a rising unemployment rate would be a Fed that is more active in bringing interest rates down, while lower consumer spending puts a cap on inflation. This is the textbook end of a business cycle, as some near-term pain typically leads to long-term opportunity. However, with the impressive AI spending and strength among higher-end consumers, this cycle could go on for longer than normal.

SPECIAL REPORT: GOLD, CURRENCIES AND THE REAL-WORLD RIPPLE EFFECTS

The relationship between gold and fiat currencies has entered a new era — one where precious metals carry weight far beyond their shine.

Chris Cooper

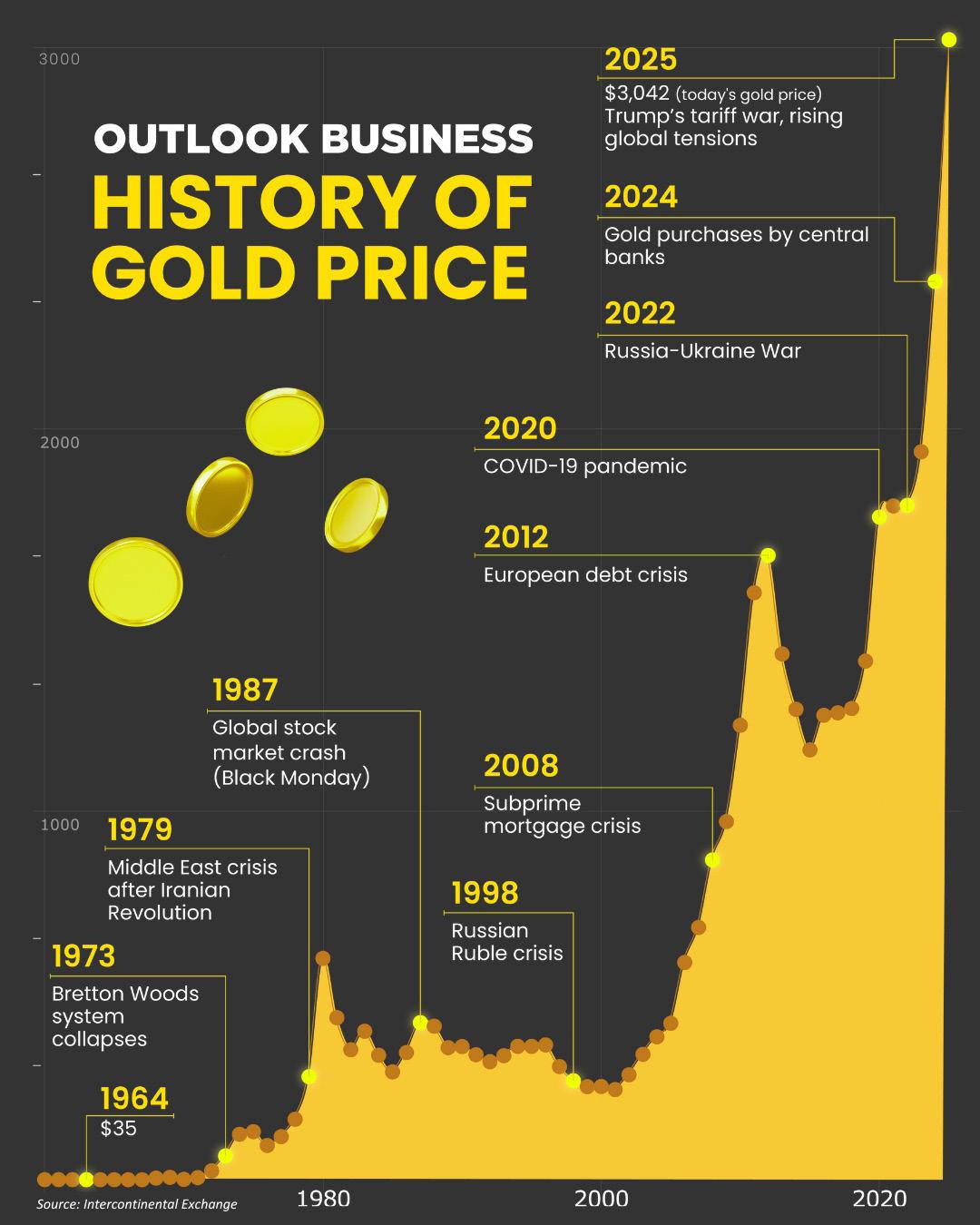

Over the last few years, precious metals – especially gold – have regained relevance in global finance. Once dismissed by some as an outdated relic of archaic systems, gold is again commanding serious attention. Recent price action has garnered the eye of investors and major money managers, many of whom are revisiting the asset class for the first time in years.

This makes it timely for us to re-examine how gold’s rise interacts with the U.S. dollar and global currency markets, and to discuss potential effects on broader economies and markets. It might seem “boring” at first, but beneath the surface its implications for investors could be profound.

GOLD’S GOLDEN RUN

Consider this:

• In late 2022, gold was trading near $1,800 per troy ounce

• By the end of 2023 it approached $1,940

• By December 2024 it was roughly $2,386

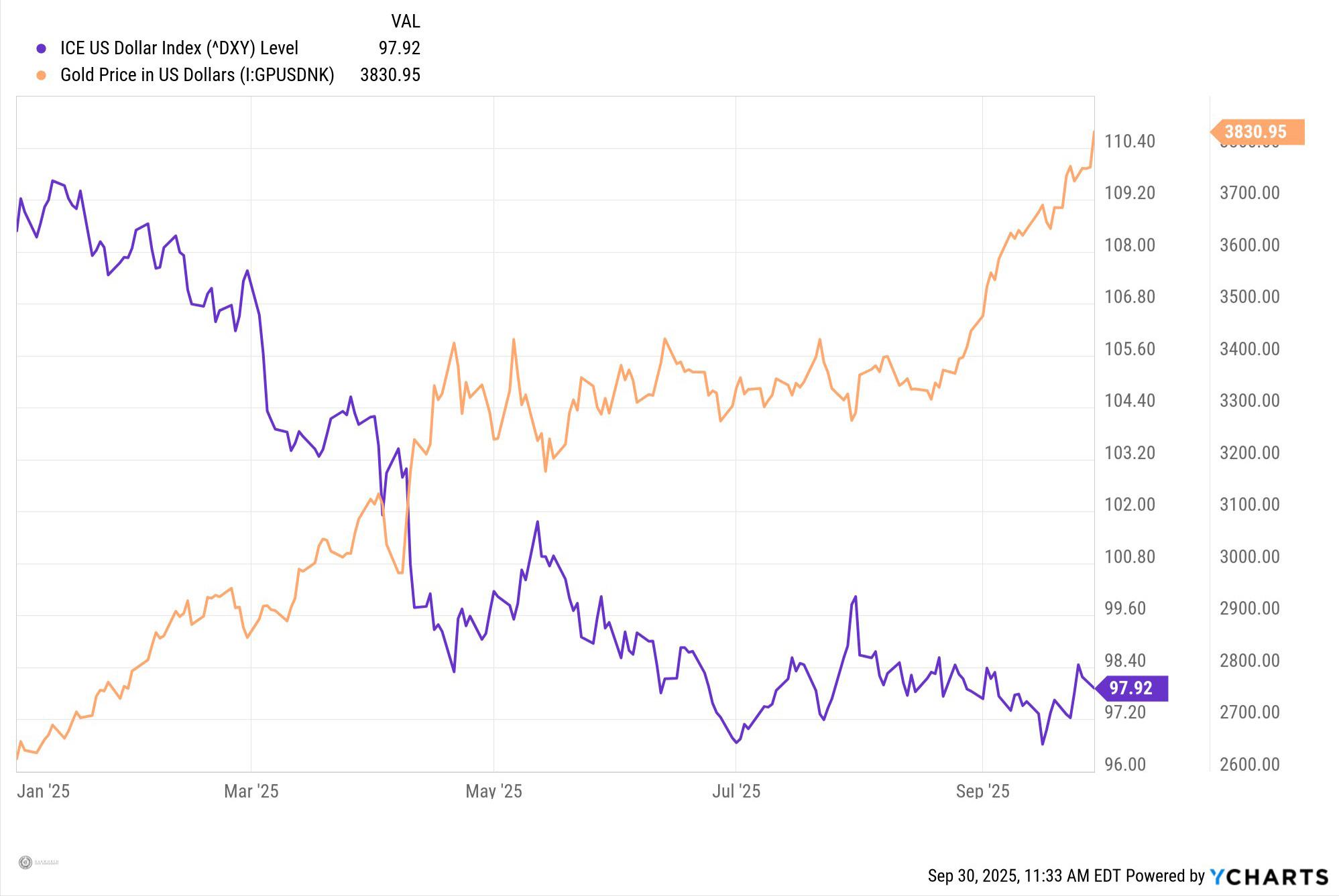

• As of Sept. 30, 2025, gold is valued at $3,898 per ounce1

In less than three years, gold has more than doubled in value – a notable move for any commodity. With sustained demand, not only from speculators, but more importantly from institutional players such as central banks, large money managers and sovereign reserve administrators, it is our opinion that gold’s rise does not appear to be a short-term tactical trade. In the first quarter of 2025, for example, the National Bank of Poland increased its holdings significantly, and China resumed steady reported purchases. 2 At a broader level, global central bank gold reserves, according to the World Gold Council, have reached record levels – pushing upward of 36,700 tonnes, surpassing levels not seen since the post-Bretton Woods era, the modern era of fiat currencies. 3

We see the drivers clearly: mounting fiscal debt burdens, questions over monetary policy credibility, fears of inflation, continued increase of money supplies and a growing desire among many nations to lessen dollar dependence – or at least limit exposure to U.S. Treasuries. Gold is no longer a relic held in mom and pop’s safe. It is reaserting itself as a cornerstone of strategic reserve policy.

GOLD AND GREEN –METALS AND THE DOLLAR

When gold climbs, it tends to cast a shadow on the U.S. dollar. Gold is priced in dollars, so if the dollar weakens, a rising gold price is easier to absorb. But more than that, the

upward trend in gold may reflect investors’ declining confidence in fiat currencies – especially the dollar’s role as the world’s reserve currency. History suggests a negative correlation, especially over tail events, between gold and USD exchange rates. In times of stress or uncertainty, gold exhibits safe haven behavior in its relationship to currencies. 4 In more normal periods, gold can act as a hedge or diversifier in currency portfolios. One common rule of thumb is that a sharp gold rally – say, +10% over a given period – often correlates with a 2–3% weakening of the dollar, as measured by the ICE U.S. Dollar Index (DXY).5 Essentially, when investors are reallocating out of dollar-based assets and into gold, downward pressure is exerted on the dollar.

$3,898 ( as of 9/30/2025)

AS CONFIDENCE IN THE DOLLAR WEAKENS, GOLD PRICES RISE

The dollar’s strength or weakness is shaped not only by gold but also by interest rate differentials, macro data, central bank policies and geopolitical confidence. For example, when the Federal Reserve cuts the overnight lending target, real yields may fall, making the dollar less attractive and giving gold more room to advance. We’ve seen hints of this recently with U.S. inflation data coming in softer than expected, labor markets weakening and futures markets increasingly pricing in more additional rate cuts for 2025 and into 2026. 6

Gold’s upward momentum feeds directly back into the psychology of currency markets. A persistent rally can encourage currency traders to reprice future USD weakness, prompting capital to shift from dollar-dominated liabilities into assets such as gold or nonUSD reserve assets. In this way, gold becomes more of an active market signal rather than just a passive recipient of dollar moves.5

Gold and the greenback often move in a feedback loop: dollar weakness leads to gold strengthening, which in turn leads to greater doubts about the dollar, reinforcing the cycle until interrupted by some pivot or external shock.

CURRENCY MOVEMENTS, GLOBAL MARKETS AND ECONOMIC CONSEQUENCES

When gold exerts downward pressure on the dollar, multiple effects ripple across global currencies.

First, non-U.S. currencies relative to the dollar tend to appreciate. The euro, yen, pound and others often benefit as capital flows out of the dollar. We have seen this dynamic play out clearly this year. Stronger foreign currencies can tighten trade balances, as imports become cheaper for non-USD

buyers, but it can also create headwinds for export competitiveness. If domestic demand is soft, this can add deflationary pressure.

Second, “commodity currencies,” such as the Australian dollar, Canadian dollar, South African rand, etc., often benefit from higher gold and commodity prices. These nations are direct producers of precious metals, so rising metal prices boost export revenues, strengthen trade balances and support currency appreciation. The currency of a goldproducing country tends to pick up a tailwind as gold revenue inflows rise. Conversely, when gold weakens, pressure returns.5

Third, emerging market currencies can feel the squeeze in a gold-driven dollar decline, as many emerging markets issue debt in U.S. dollars. If the dollar weakens, their debt-servicing burden loosens somewhat in terms of local currency; but if capital pulls back in anticipation of United States or developedmarket volatility, their currencies may still come under downward pressure anyway. Simply put, a gold rally can prompt

WHEN SHINY TURNS SERIOUS

Precious metals, especially gold and silver, have been signaling loudly from the rooftops for the past three years as evidenced by the price appreciation. Even alongside an appreciating U.S. equity market, the “safe haven” assets have been sharing their own stories of deep undercurrents in global macroeconomics, reserve management and currency strategy. Their climb exerts pressure on the U.S. dollar, reshapes exchange rate dynamics and recalibrates capital flows, trade balances and financial portfolios worldwide. For investors, the impact is seen in

SOURCES

1. YCharts – “Gold Price in U.S. Dollars”

2. World Gold Council – “Central Bank Gold Buying Slowed in April” (June 2025)

3. World Gold Council – “Gold Demand Trends Full Year 2023”

4. Cornell University – “The Generalisation of the DMCA Coefficient to Serve Distinguishing Between Hedge and

investors to rebalance capital away from riskier markets, punishing their currencies unless they are perceived as safe.

Fourth, these currency shifts feed through into global trade patterns and capital flows. A stronger non-USD currency gives those countries more strength to import, spend, invest and accumulate reserves. In turn, countries consider reserve diversification strategies — including gold, euro, yuan, etc. The rising interest in “de-dollarization” is no longer just small talk, according to CNBC – it is being established in reserve shifts and trade arrangements outside dollar transactions. 7

Lastly, the cumulative effect of currency and capital flows tends to amplify global divergence. Countries with structural strengths such as low debt, commodity endowments and credible monetary policy tend to benefit while risks such as twin deficits and foreign liabilities are exposed. In such cases, precious metals may act like a seismograph, signaling stress points in the global system.

inflation expectations, borrowing costs — and arguably most importantly — investment returns.

Our opinion is we are witnessing a renaissance for precious metals – not as nostalgic relics, but as active mediators in 21st-century monetary dynamics. Following the aftermath of COVID-induced monetary and fiscal policies, the relationship between gold and fiat currencies has entered a new phase, one in which precious metals carry meaning far beyond their shine.

Safe Haven Capabilities of the Gold” (arXiv, 2019)

5. Finance Markets Today – “The Relationship Between Gold Prices and Currency Strength” (March 2025)

6. Reuters – “Gold Hits Record High on Rate-Cut Bets, U.S. Government Shutdown Fears” (Sept. 29, 2025)

7. CNBC – “Dollar Divorce? Asia’s Shift Away From the U.S. Dollar is Picking Up Pace” (June 2025)

ASSET ALLOCATION

We don’t try and time the market. But we do try and stay flexible so that we can adapt to change.

Sam Clement

The third quarter of 2025 unfolded with an unusual quietness in the markets, especially in comparison to the turbulence of the second quarter. Volatility remained muted and stock indexes drifted steadily higher. In contrast to the prior quarter’s tariff uncertainty, inflation surprises and geopolitical tension, the third quarter was defined by a sense of calm, at least in the markets. While this may not have made for dramatic headlines, it did allow us to enjoy the continued rebound from April’s lows and even make new highs.1 With volatility so low, however, a continued question of our investment committee has been: “What will change this low-volatility environment?” After all, we believe volatility tends to normalize.

MARKET VOLATILITY

Both realized and implied volatility remained near the lower end of historical ranges this quarter, with measures like the CBOE Volatility Index (VIX) signaling complacency rather than concern. 2 Despite occasional spikes around earnings seasons or major data releases, volatility failed to sustain any momentum — except down. These brief spikes were quickly absorbed by the market, which resumed its slow grind higher, giving the impression of investor indifference to just about anything.

MARKET VOLATILITY OVER THE PAST 12 MONTHS

EQUITY MARKETS

Leadership rotated slightly, with more cyclical and rate-sensitive sectors, including small- and mid-cap stocks and real estate, participating more than they had earlier in the year. Market breadth, however, remained somewhat narrow, with the largest gains still concentrated in the tech and tech-adjacent areas. The tech heaviness of the market cannot be ignored as the artificial intelligence (AI) revolution continues to be the talk of the market, not necessarily due to irrational exuberance, but from the unbelievable levels of capital expenditure and commitment to leading the charge in AI.

In this context, we have maintained a neutral asset allocation stance both in terms of equities to fixed income and growthto-value within equities. The last few years have proved more difficult to find areas of the market that appear undervalued.

However, as tech-heavy sectors continue to drift higher, opportunities are emerging in the seemingly forgotten sectors of the market.

This sentiment, where entire sectors fall out of the spotlight, is not new, but in our view it creates opportunities. This is not a doom-and-gloom situation for growth but rather an opportunity, in our opinion, to better balance risk and reward. Put differently, the bar is raised for growth areas to continue to beat expectations while the margins for error have narrowed.

We also remain of the opinion that volatility tends to mean revert…in other words, periods of low volatility are followed by a return to higher levels, and vice versa. Markets do not stay calm forever. The timing, however, is impossible to predict, and we believe it is prudent to begin preparing for it rather than wait for it to arrive.

Our approach is grounded in a couple of key beliefs:

1. The current risk and reward dynamic in equities appears balanced rather than overly compelling. That balance largely comes from the fact that some areas of the market are a bit more richly valued.

2. We recognize that flexibility is essential in a market like this. Remaining neutral means that we’re not overcommitted to any one outcome, which allows us to respond thoughtfully and have the dry powder ready as occasions arise.

Our neutral positioning gives us the flexibility to react decisively, either by increasing risk if opportunities emerge or by getting defensive if more storm clouds arrive.

FIXED INCOME

Fixed income continues to be a ballast for our portfolios, a source of stability rather than an area where we want to swing for the fences. Our duration, or interest rate sensitivity, remains low as the long end of the curve continues to digest the push and pull between inflation and a softening economy and labor market. It is our opinion that credit spreads are incredibly tight, which to us suggests it doesn’t make sense to take on significant risk in an area that we believe is primarily used to smooth out returns over time.

Importantly, this process is not about making a binary call on market direction. Rather, it’s about acknowledging that market trends change, and that a prudent investor prepares for multiple outcomes.

We are not trying to time the market; instead, we are looking to manage risk in a way that preserves the ability to participate in the upside while protecting portfolios from unforeseen headwinds.

SOURCES:

1. Federal Reserve Bank of St. Louis – S&P 500

2. Federal Reserve Bank of St. Louis – CBOE Volatility Index (VIX)

LOOKING AHEAD

Looking forward, we expect the fourth quarter to offer more clarity on whether the low-volatility trend can persist. Key events, including two more Fed FOMC meetings, upcoming inflation and labor market data, and the fourth-quarter earnings season, will provide insight into the continued health of the consumer and how well companies are performing. 3

In summary, the third quarter was a quarter characterized not by explosivity but by a calm and steady climb. This environment rewarded patience and penalized overreaction. We maintained a neutral asset allocation and, while welcoming the market’s recent resilience, we remain mindful that periods of low volatility rarely last indefinitely. With that, we continue to look for opportunities to balance risk and reward in a thoughtful and deliberate manner. As always, we will remain flexible and open to changes as they may come with whatever the future holds.

3. Federal Reserve, FOMC Meeting Calendar 2025 (Board of Governors of the Federal Reserve System).

VIX -The VIX is a theoretical, uninvestable benchmark that measures the market’s expectation of future volatility. You cannot purchase the VIX itself like a stock. Instead, you must buy derivatives that track VIX futures, and their value may not perfectly align with the VIX index.

The views expressed are those of the author and Oakworth Asset Management as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance, and you may not get back the amount invested.

2025 YEAR-END PREDICTIONS

From disruptive politics and rising beef prices to AI upheaval, bond market volatility and other proverbial canaries in the coal mine — these are our Investment Committee’s top predictions through the end of 2025.

• Last quarter, we predicted that excess levels of debt, bloated central bank balance sheets and declining investor confidence in public institutions could support continued strength in precious metals. This quarter, we get to add another factor from the September Federal Open Market Committee: the Federal Reserve has finally begun cutting interest rates. In short, the case for gold and other shiny stuff is arguably still there.

• Unless something dramatic happens in October, Zohran Mamdani, in our opinion, is well-positioned to win the New York mayoral election in November. If and when that happens, the country — and perhaps the world — will anxiously wait to see if he can enact his aggressive progressive economic agenda. It could set the tone for discussions in the national midterms in 2026.

• If China were wise, it would quietly, and as surreptitiously as possible, build up its military and let the West tear itself apart at the seams. As Chinese general Sun Tzu wrote in The Art of War: “… the opportunity of defeating the enemy is provided by the enemy himself.”

• No matter what the Fed does with the target overnight lending rate between now and the end of 2025, the cost of domestic beef isn’t coming down significantly. According to the American Farm Bureau, the supply of beef cattle simply cannot grow that fast that soon. So, Americans will just have to grin and bear it at their tailgates and barbecues for a while longer.

• Unless a new “must-have” technology or product magically appears in a short period of time, the 2025 holiday shopping season will likely disappoint. U.S. consumers are still worried about inflation and aren’t as secure in their jobs as they once were. Adding to this, as reported by PwC, younger generations seem to favor “experiences” over things.

• A permanent conclusion to the wars in either Gaza or Ukraine by the end of 2025 is highly unlikely. With the so-called global “court of public opinion” largely on their side, the Palestinians and Ukrainians will continue to fight as long as possible. For their part, neither the Israeli nor Russian governments can run the political risk of compromising while they have the military advantage. It is our opinion that this is a real problem.

• By year-end, the run-up to the May 2026 local elections in the United Kingdom (U.K.) will already have reached a fever pitch. Ultimately, it will serve as a referendum between Labour and Reform U.K. By next spring, many will view these elections as potentially the most important in the history of the United Kingdom.

• The September collapse of subprime auto lender Tricolor could be a proverbial canary in the coal mine for the sector as a whole. This collapse comes as the entire industry struggles with tariffs and declining profitability. At best, the sector will likely close 2025 with less confidence about the future than it would like.

16

• Unless something unforeseen happens, the Federal Reserve would like to reduce the target overnight lending rate to 3.0% to 3.5% by the end of 2026 (as projected in the FOMC’s dot plot)—assuming U.S. inflation allows it to do so. The problem with forecasting inflation is the uncertainty of tariffs on consumer prices, and the fact that U.S. producers aren’t as in control of their inputs and supply chains as they once were.

• If predicting inflation has gotten difficult, so too has forecasting longer-term interest rates. Typically, long-term rates reflect future inflation expectations. The question then remains: Will the bond markets be able to handle the continuous surge in new Treasury supply without pushing rates higher? Time will tell.

• Questions about AI will continue to build, most of them negative. What is the true industrial demand for AI? How much is circular? How many jobs will AI kill? How will this impact the U.S. economy? Will this economic slowdown cause the Federal budget deficit to explode? While these are legitimate and potentially painful short-term concerns, AI is here to stay, and the long-term innovations will be awesome.

• Holiday box office hopes are falling on “Avatar: Fire and Ash,” “Zootopia 2,” “The SpongeBob Movie: Search for SquarePants” and “Five Nights at Freddy’s 2.” Obviously, all of these are sequels or spinoffs. Hollywood is betting on repeats. And who says creativity is dead?

• Finally, on December 31, the year 2025 will mercifully end.

Central Alabama Office

850 Shades Creek Parkway Birmingham, Alabama 35209

Phone: (205) 263-4700

South Alabama Office

1 St. Louis Street, Suite 3200 Mobile, Alabama 36602

Phone: (251) 375-7800

Central Carolinas Office

6000 Fairview Road, Suite 125

Charlotte, North Carolina 28210

Phone: (704) 901-7250

Middle Tennessee Office

5511 Virginia Way, Suite 110

Brentwood, TN 37027

Phone: (615) 760-1000

Advisory Services, including investment management and financial planning, are offered through Oakworth Asset Management LLC a registered investment advisor and is owned by Oakworth Capital Bank, Member FDIC. Investment products and services offered via Oakworth Asset Management LLC are independent of the products and services offered by Oakworth Capital Bank, and are not FDIC insured, may lose value, have no bank guarantee, and are not insured by any federal or state government agency. Because of the ownership relationship and involvement by Oakworth Asset Management LLC associates with Oakworth Capital Bank, there exists a conflict of interest to the extent that either party recommends the services of the other. Oakworth Asset Management LLC does not provide tax or legal advice. You should consult your tax advisor, accountant, and/or attorney before making any decisions with tax or legal implications. For additional information about Oakworth Asset Management LLC, including its services and fees, send for the firm’s disclosure brochure using the contact information contained herein or visit advisorinfo.sec.gov

This communication contains general information that is not suitable for everyone and was prepared for informational purposes only. Nothing contained herein should be construed as a solicitation to buy or sell any security or as an offer to provide investment advice. The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect any one client situation. This communication contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ. As such, there is no guarantee that any views and opinions expressed herein will come to pass. Investing involves risk of loss including loss of principal. Past investment performance is not a guarantee or predictor of future investment performance.

Any reference to a market index is included for illustrative purposes only as it is not possible to directly invest in an index. The figures for each index reflect the reinvestment of dividends, as applicable, but do not reflect the deduction of any fees or expenses, the incurrence of which would reduce returns. It should not be assumed that your account performance or the volatility of any securities held in your account will correspond directly to any comparative benchmark index. This communication contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to their accuracy or completeness.

All opinions and/or views reflect the judgment of the authors as of the publication date and are subject to change without notice.